Salesforce (NYSE:CRM) stock moved modestly higher on Thursday, trading on word that it had closed its acquisition of Tableau Software. Given the visual analytics capabilities and the massive growth forecasted while Tableau traded on a separate ticker, it will likely become a valuable acquisition for CRM stock.

CRM continues to make other deals as well. A recently announced partnership with Alibaba (NYSE:BABA) should also increase its reach into the world’s second-largest economy. This could help Salesforce achieve one of its goals of doubling sales by fiscal 2023.

However, despite these moves, CRM stock has seen falling multiples and little price action since the beginning of the year. This calls into question what it will take to boost CRM. Until investors get an answer to that question, I see little reason to own Salesforce stock.

Tableau, Alibaba Should Boost Salesforce Revenues

Few question the premise that Tableau will add significantly to Salesforce’s growth. When Tableau traded as a separate company under the DATA ticker, analysts predicted 680% profit growth this year and 31% the next. Given that rate of increase, CRM probably made a wise purchase despite paying more than 12-times sales for the company.

Further, partnering with Alibaba gives CRM a foothold into China. The deal makes Salesforce the only enterprise customer relationship management (CRM) software that Alibaba will sell on its platform.

Salesforce Stock Could Still Struggle

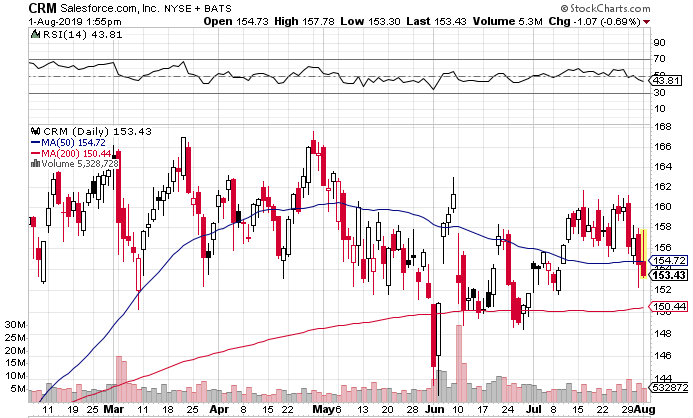

However, I think traders want to know whether these deals will reinvigorate CRM stock. The company recovered quickly from the market slump back in December. Still, it has seen little movement in the price since February.

Many also wonder if valuations will recover to previous levels. The forward price-earnings (P/E) ratio stands at about 60. That may appear high by S&P 500 standards. However, that multiple has fallen far from its average five-year P/E ratio of about 274. Moreover, this year, analysts expect an earnings increase of only 5.1%.

Admittedly, I would treat this lower growth as an anomaly since Wall Street also projects average annual profit increases of 29.58% per year over the next five years. Still, that comes in below the 47.2% average for the previous five years.

We have also begun to see indications of a downtrend in the charts. As InvestorPlace

feature writer James Brumley mentions, CRM stock has struggled to stay above its 200-day moving average. In June and July, bulls rescued the Salesforce.com stock price. Still, with no significant price action since February, repeated tests of this level should cause concern.

CRM Saw a Huge Run-Up Over the Last 10 Years

Over the past 10-plus years, CRM stock has seen an incredible run. In November 2008, the Salesforce.com stock price fell as low as $5.21 per share. Today’s price of almost $155 per share represents an increase of nearly thirty-fold!

Salesforce’s Software as a Service (SaaS) has become a disruptor across the tech industry. Although companies such as Microsoft (NASDAQ:MSFT), Oracle (NASDAQ:ORCL) and SAP (NYSE:SAP) offer competing products, they have not threatened Salesforce’s leadership in CRM software.

Still, stock prices depend on the future. Salesforce should remain a leader in its industry. However, recent deals have not stopped the multiple compression in CRM. Unless the company can find a larger catalyst, investors may see little near-term profit in Salesforce stock.

Final Thoughts on CRM Stock

The Tableau and Alibaba deals help Salesforce.com, but they may not help to boost CRM stock. Salesforce stock has seen massive increases over the last 10-plus years. Its SaaS capabilities have transformed tech and buying Tableau should continue this market leadership.

However, it remains uncertain how much longer Salesforce stock can defy gravity. The forward P/E ratio has fallen back to double digits. As mentioned before, recent deals have done little to rescue the falling valuation.

CRM stock reports its earnings on Aug. 22 after the closing bell. From there, investors should have a better indication of what these deals do for this equity.

I do not see a massive downturn occurring in this stock. However, I also do not think the Tableau buyout or the Alibaba deal will stop this multiple compression. With high expectations and the lack of additional catalysts, I do not see what will.

As of this writing, Will Healy did not hold a position in any of the aforementioned stocks. You can follow Will on Twitter at @HealyWriting.