When Amazon.com (NASDAQ:AMZN) reported on its ever-increasing free cash flow growth last quarter, the stock fell regardless. At 12% below its $2,000 July peak and after trading recently at $1,805.60, should investors accumulate AMZN stock?

Amazon.com reported second quarter 2019 free cash flow of $25.02 billion, up 140% year-over-year. Its long-term goal is to optimize free cash flows and it certainly looks like the job’s getting done. It will achieve that in a way every other fast-growing firm does so: by growing sales. Net sales were $63.4 billion, up 20% Y/Y. North America accounted for 61% of the online retailer’s net sales in the period. International was 27%, while AWS was 12% of sales.

In North America, operating income fell 15% to $1.56 billion. Its guidance is for the next quarter is lower than analyst expectations. The focus on one-day shipping is driving higher shipments but higher costs come with it. The associated costs of additional transportation and getting capacity in place will continue to hurt operating income.

The short-term underperformance might explain why the stock fell by almost 10% in the last month. Though the stock is still trading in an uptrend, conservative investors might want to wait for operating cost growth to slow.

One-Day Shipping Lures Customers

Shipment unit volumes increased in the second quarter, driven by the one-day shipping offering. The lower ASP is a setback because it puts pressure on profit margins. Still, offering faster shipping times differentiates the online retailer from competitors like Target (NYSE:TGT) or Walmart (NYSE:WMT). So long as Amazon balances price convenience and selection, customers will gravitate back to the site. The faster shipping option will drive revenue growth for the long term. Plus, attracting more third-party merchants will give customers a wider range of product choices on the site.

Amazon continues to invest in its fast-growing AWS cloud business. It is also investing in devices, video, and the global expansion of much of its Prime Benefits. Development of grocery delivery, through Whole Foods, Prime Now, and AmazonFresh units will weigh on income for a while longer. In Q1, the firm did not face much of these costs. These efforts picked up in Q2 and will continue through the remainder of the year, at the very least.

Ads and Alexa’s Allure

Video ad revenue is a potential business opportunity. But to grow its viewership, the company will first expand its video and over-the-top offerings. It is developing live sports offerings and IMDb TV. Looking ahead, Amazon Publisher may benefit from service integrations. As more and more consumers buy a Fire TV device, Amazon.com could easily compete with

Roku (NASDAQ:ROKU) in growing its subscriber base.

Video advertising opportunities are greatest in North America. International markets have the potential to draw video ads, too, but Amazon must first improve on delivering more relevant ads that match viewers within international geographies.

With hundreds of third-party devices building in Alexa, Amazon becomes a touch point for even more consumers. Good partnerships and arrangements with companies like BMW and its Mini increase the frequency of consumers interacting with Alexa. As the software gets better and smarter, consumers may enjoy the benefit of the enhanced experienced the home assistant has to offer.

Valuation Shows Upside

Some 31 analysts who cover AMZN stock have an average price target of $2,284. Per TipRanks, that represents an upside of 26.5%. Conversely, investors may build a 5-year Growth Exit model that assumes a perpetuity growth rate of 3.5% – 4.5%. In this more conservative forecast, the stock’s fair value is $1,961, 8% above its recent $1,806 price.

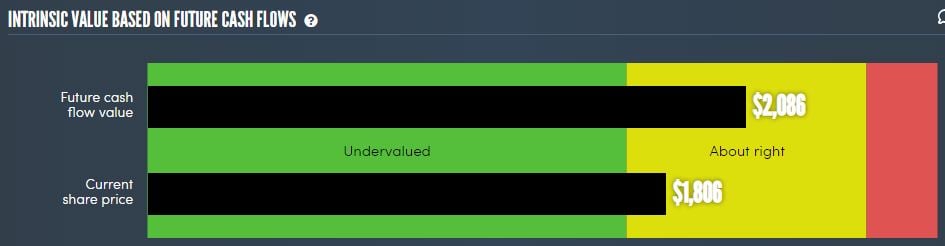

Simplywall.st thinks the stock is worth $2,086, based on future cash flow:

Source: https://simplywall.st/

Your Takeaway on Amazon Stock

This is a conglomerate with a wide range of businesses that will shield it from any downturn. The Amazon.com stock valuation is relatively lower than that of Roku or Netflix (NASDAQ:NFLX) stock. Yet investors get an online retailer, a supplier of music and video, a grocery, and a consumer devices maker, just to name a few segments. The share price is holding steady at the $1,800 level and could bounce higher as investors decide to buy the dip.

Disclosure: As of this writing, the author did not hold a position in any of the aforementioned securities.