Drugstore chain Rite Aid (NYSE:RAD) is fighting for its life, if the recent and not-so-recent performance of Rite Aid stock is any indication.

That’s a tough truth for shareholders to hear, but that doesn’t make it not true. Remember, this is the same company that in 2015 was willing to sell itself, in its entirety, to rival Walgreens Boots Alliance (NASDAQ:WBA). It was a lifeline more so than a strategic decision, in retrospect.

The pharmacy chain business is also just a tough one to thrive in anymore, as evidenced by the recent decision from Fred’s to begin Chapter 11 bankruptcy proceedings. The smaller player isn’t even going to bother trying to team-up with a bigger and better-established player like Walgreens or CVS Health (NYSE:CVS). It’s simply looking to liquidate its assets.

There’s one last ace in the hole Rite Aid could play, however, to light a fresh fire under a deteriorating RAD stock price. That’s new CEO Heyward Donigan. Just know that the turnaround effort she’ll have to lead is a monumental task, and the odds aren’t in her favor.

A New CEO and Rite Aid Stock

There’s little doubt 58-year-old Heyward Donigan’s got the chops.

Prior to taking the helm for Rite Aid, she was chief executive of Sapphire Digital … a company that leveraged an effective use of data to lower the total cost of buying and offering health care; you may know the company better by its old moniker, Vitals.

Before that, Donigan led a similar outfit called Value Options, and before that, she was a Senior Vice President of Operations for health insurer Cigna

(NYSE:CI). Donigan is also a board member for Kindred Healthcare and Eastern Virginia Medical School.

In short, she knows the healthcare business.

Knowing the ins and outs of an industry and being able to keep a third pharmacy chain afloat in an environment that may only need two, however, aren’t the same thing. Donigan may well have inherited a project that’s simply too far gone to be salvaged.

Scaling Is a Real Problem for Rite Aid Stock

Ask ten different people what’s ultimately ailing Rite Aid, and you’ll likely get at least seven different answers. All of those answers, however, would point in the same general direction: Rite Aid lacks the scale and reach necessary to hold up in an environment where every aspect of the nation’s healthcare apparatus is under fire.

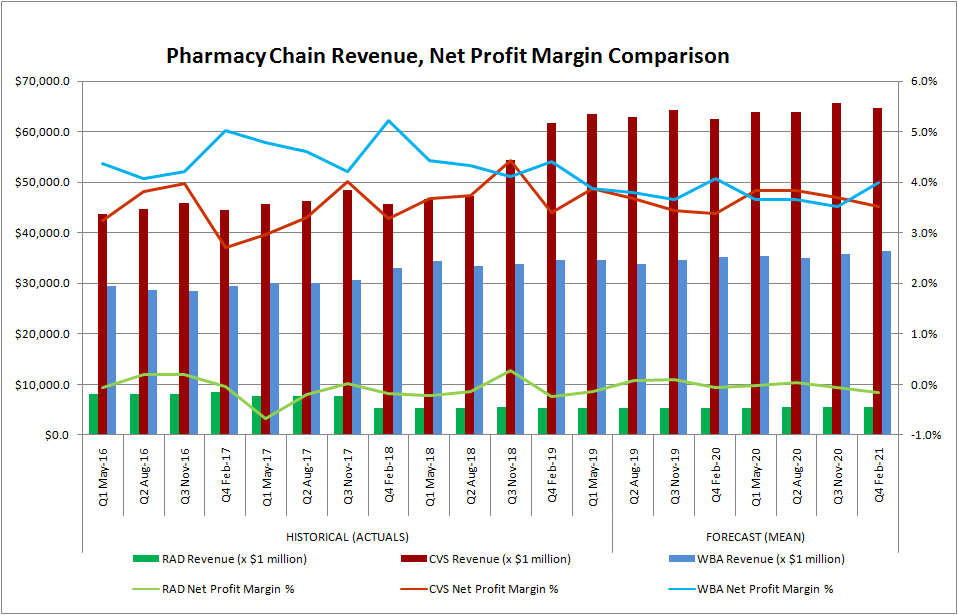

The simplest of numbers tell the tale. Over the course of its past four quarters, Walgreens has done $136 billion worth of business. CVS Health has done a whopping $226 billion in sales. Rite Aid, meanwhile, has struggled to produce a twelve-month top line of $21.6 billion.

That exceedingly small size makes it tough to cover its fixed costs its bigger rivals can more readily absorb. Specifically, Rite Aid pays out a disproportionately higher amount of its revenue to cover selling, general and administrative costs, and its $3.5 billion worth of long-term debt is forcing the organization to pay roughly twice as much, relatively speaking, as Walgreens to service its debt load. The end result is alarmingly thin profit margins.

Click to Enlarge

A lack of scale also establishes another (albeit related) hurdle. That is, Rite Aid doesn’t have the same sort of buying power its rivals enjoy.

Undoubtedly Rite Aid has secured some price breaks due to its capacity to sell in volume, from behind its pharmacy counters as well as from its stores’ general shopping areas. But, at roughly one-tenth the size of both CVS Health and Walgreens, its suppliers simply can’t prioritize discounting the way they can for the company’s bigger rivals.

Finally, its small size prevents Rite Aid from entering agreements that would help buoy its business, such as the union of CVS and health insurer Aetna. Would-be partners want scale as well, particularly if a relationship is going to be an exclusive one.

Looking Ahead for Rite Aid Stock

Ergo, Donigan’s primary task ahead is also the toughest thing Rite Aid could be asked to do at this time … grow the company.

Never say never. Anything’s possible. Perhaps she has a plan to do what John Standley couldn’t between 2010 and August of this year.

Somehow though, that endzone seems out of reach. Indeed, the company is seemingly moving in the wrong direction, handing over 1932 of its stores to Walgreens, sacrificing scale in an effort to pay down debt, and giving a competitor even more scale in the process.

Throw in the fact that a digitally dominant Amazon.com (NASDAQ:AMZN) now manages online pharmacy Pillpack and at the same time is looking for ways to completely circumvent the traditional means of delivering healthcare, and a recovery seems pretty close to impossible.

Donigan will need to pull off a miracle if RAD stock is ever going to be worth owning again. Don’t hold your breath.

As of this writing, James Brumley had no position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.