If there was any doubt to the power of Shopify (NYSE:SHOP) and its e-commerce business, SHOP stock removed it all. At a time when we have so many questions about the viability of the domestic and global economies, SHOP represents the bright beacon of hope. Since the start of the year, shares have jumped an astonishing 146%.

Even more remarkable, Shopify stock had slowed down noticeably last year. Once the dust settled on a volatile end to 2018, shares of the upstart e-commerce firm were only up 36%. That gave ammunition to the bears — including yours truly — to criticize the company’s business model. At the time, it also seemed like the bubble was bursting, given that SHOP stock skyrocketed 133% in 2017.

Of course, I was dead wrong about Shopify stock. Part of the reason why shares have done so remarkably well in 2019 was due to the fundamentals, the very thing that bears have criticized. For example, in the company’s most recent second-quarter earnings report, management knocked it out of the park.

In terms of per-share profitability, SHOP delivered earnings of 14 cents per share. That figure easily surpassed analysts’ consensus call for earnings-per-share of 2 cents. On the revenue front, Shopify rang up $362 million, besting consensus estimates for $350 million. Not surprisingly, SHOP stock flew substantially higher on the news.

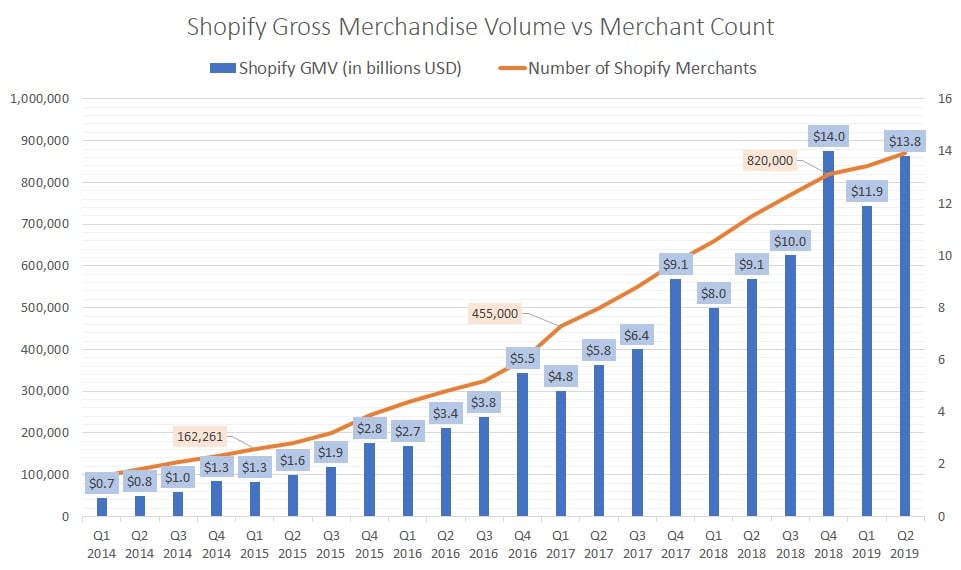

Additionally, the granularity was also very positive in Q2. For instance, gross merchandise volume (GMV) hit $13.8 billion, shooting Merchant Solutions revenue up 56% year-over-year to $153 million. Also, the number of merchants is over 800,000 (although Shopify didn’t specify in their Q2 summary).

All in all, that’s tremendous news for Shopify stock, right? Not so fast.

SHOP Stock Is a Deceptively Attractive Investment

On the surface, it seems you can’t lose with Shopify stock. For one thing, it’s levered to the broader e-commerce revolution that drove up names like Amazon (NASDAQ:AMZN). More importantly, they’re demonstrating that more merchants are boarding the Shopify train.

For the bulls, the below chart represents one of many reasons why they’re excited about SHOP stock. Whether you’re talking about the price of shares or corporate revenue or GMV and merchant count, several metrics are exercising the positive end of the vertical scale.

Click to Enlarge

But while it’s crucial to have the right numbers moving higher, the reality is that context matters. And this is where some of the optimistic narrative for SHOP stock dies down for me.

While Wall Street toasted Shopify stock for the underlying company producing another strong earnings report, I was left wondering what they were talking about. Principally, I don’t see the same sustainable growth story that has tickled the suits covering the e-commerce firm.

Let’s break down what we actually have here. Over the trailing year since Q2 2019, Shopify merchants have generated GMV of $49.7 billion. Although I don’t have the actual merchant figure, I’m going to conservatively estimate that they have 870,000 stores. That gives me an average annual GMV per merchant of $57,126.

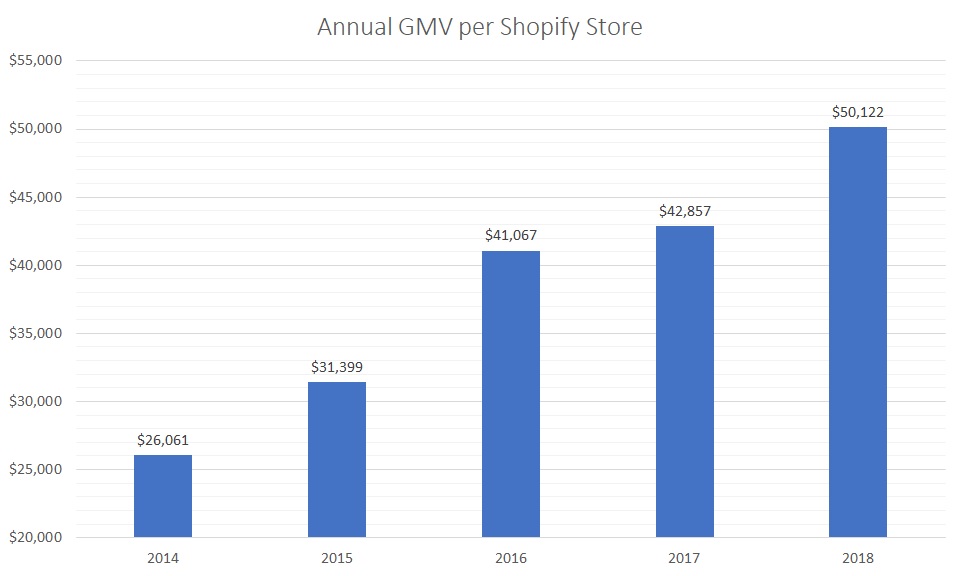

That’s probably a bit on the high end. For instance, in 2014, annual GMV per merchant was $26,061. A year later, this metric increased to $31,399. Between 2016 and 2017, GMV per merchant averaged just under $42,000. Last year, the stat registered $50,122.

Click to Enlarge

My question is, what business can survive on gross sales of $50,000 a year? In the U.S., the

median household income is $56,516.

You’re better off working for a living, which means the rally in SHOP stock is probably not sustainable.

Follow the Logic

Of course, calculating averages is merely an arithmetic exercise. In reality, we know that merchants can’t live off of $50,000 a year. Just off the top of my head, I can think of overhead expenses and inventory outlays. These and other costs and expenses can really start eating into profits in a hurry.

Logically, then, we know that Shopify gets the bulk of its GMVs from its top-tier, high-level merchants. We’re talking about the names that management always brags about in their quarterly summaries, such as Unilever (NYSE:UL), Kylie Cosmetics, Allbirds, and MVMT.

What about the other 869,996 merchants? Well, most of them will fail because they have to. Mathematically, if the lion’s share of GMVs are produced by a handful of elite organizations, that leaves very little for everybody else. And that means, revenue sources like Merchant Solutions are threatened because they could drop off as the merchants do.

Plus, if we have a recession, it’s game over. There’s no way that merchants making far less than $50,000 a year can compete with the scale of big-box retailers like Walmart (NYSE:WMT) or Target (NYSE:TGT).

Don’t get me wrong: SHOP stock can get interesting at a lower valuation. But right now, it has simply gotten well ahead of itself.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.