Fastly (NYSE:FSLY) took the investing world by storm earlier this year. After bottoming at $10.63 on March 16, FSLY stock went on a blistering run to the upside, gaining 1,008% at its pre-earnings high.

That high came on the day Fastly reported earnings on Aug 5. To its credit, the company beat on earnings and revenue expectations and topped guidance estimates.

Still, it wasn’t enough to justify a 1,000% rally. When you say it out loud, it sounds utterly ridiculous. Of course FSLY could not justify that type of rally in just 99 trading sessions. How could anyone?

That doesn’t mean the business is bad, turning south or lacking catalysts. In fact, the reality is just the opposite. So while the stock is still 28.5% off its pre-earnings high, I think the narrative here remains quite bullish.

Can Fastly Get to $100?

On Aug 24, Raymond James analysts upgraded Fastly to outperform from market perform. In doing so, the analysts also assigned a $100 price target.

FSLY stock isn’t cheap, according to Robert Majek, the analyst who upgraded the stock. That being said, the market is underestimating just how long Fastly’s growth can continue.

I agree with Majek. To me it seems that investors are looking at Fastly’s growth spurt as a one-time event due to the novel coronavirus. In reality, Covid-19 helped pull forward its growth, but edge computing is here to say – and so is Fastly’s business.

Breaking Down Fastly

Look at the robust growth at Amazon (NASDAQ:AMZN), where last quarter’s revenue of $88.9 billion obliterated estimates by $7.5 billion. Pinterest (NYSE:PINS) beat on earnings and revenue and had better-than-expected user numbers too.

Why does this matter? Because Amazon and Pinterest are among Fastly’s customers. So is Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) via Google Cloud, SoftBank and Microsoft (NASDAQ:MSFT) via Azure.

As these companies grow, so too should Fastly. But there’s a fly in the ointment when it comes to the company’s customers too. That’s as TikTok is the company’s largest customer, generating 12% of its first-half revenue. That’s a problem as TikTok faces being banned in the United States.

Perhaps that problem gets resolved and everything will be fine for Fastly. Perhaps it will be banned and revenue will see an impact. Either way, the market is viewing that revenue as a liability rather than an asset at this time.

I’ll be honest, I don’t like that risk either. However, it’s not unusual for young companies to be more heavily reliant on a few of its larger customers. As long as Fastly continues to grow – which there’s no reason it shouldn’t – then that revenue will begin to diversify.

It’s similar to the bearish narrative shorts pushed on Twilio (NYSE:TWLO) years ago. That being its over-reliance on Uber (NYSE:UBER) generating 12% of its revenue. At the time, that was a scary realization for investors, just like it is now for Fastly. However, two years later, Twilio’s 10 largest customers account for just 15% of revenue.

So while TikTok (and the narrative) might be a short-term risk, long-term bulls shouldn’t sweat this fear.

Here’s another reason why.

During the company’s most recent conference call, CEO Joshua Bixby said that, “Our enterprise customer count grew to 304, up from 297 last quarter.”

That’s good. But it’s nowhere near the end of the road. He later said in the Q&A portion of the call:

“To put our 300 enterprise customers into perspective, some of our largest competitors in the space have 6,000 – 7,000 of these. So, this is – we are in the early days of this market from our perspective… So if you sort of captures wider to some of these other companies that have 30,000 or 100,000 enterprise customers that’s certainly where we’re looking at.”

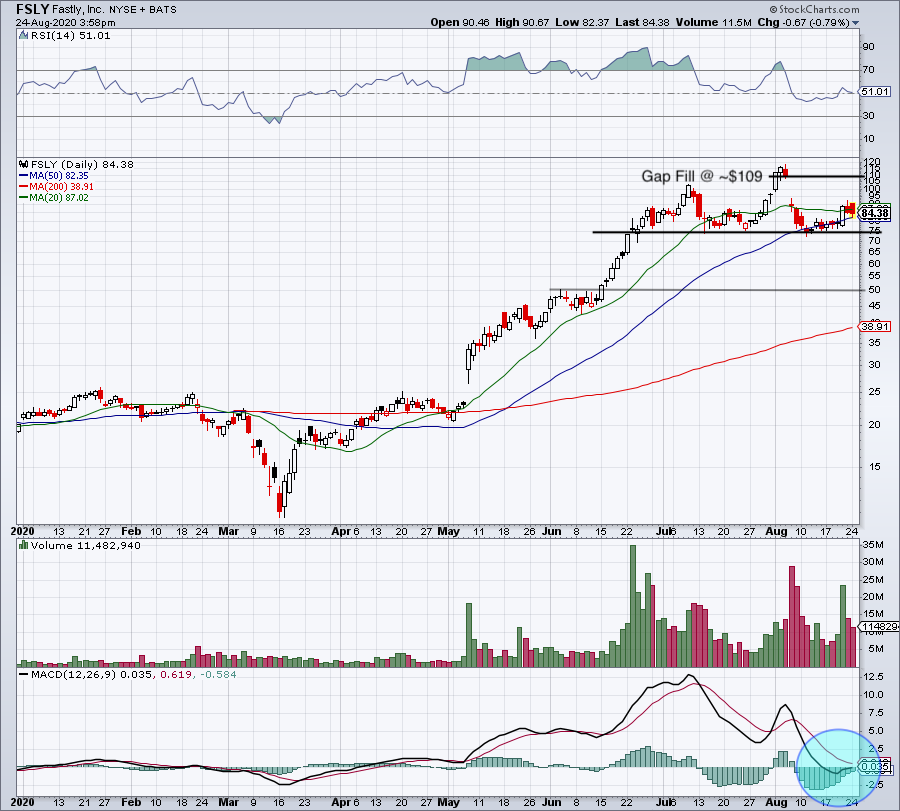

Trading FSLY Stock

Click to Enlarge

The $75-ish area continues to act as decent support for FSLY stock, while it’s hugged the 50-day moving average for much of this month. Last week, shares popped higher but they keep getting rejected by $90 and the 20-day moving average.

A close below the 50-day likely puts $72 to $75 back in play. Over last week’s high at $92.19 puts the post-earnings high of $94 in play, followed by $100. From there, investors will be looking for a gap-fill up toward $109.

A close below $70 could put $50 in play, particularly if it’s in conjunction with a larger market decline. To be honest, that would be a very attractive long opportunity in my mind.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long FSLY, PINS and GOOGL.