While we are still far from a resolution with the novel coronavirus pandemic, many segments of society are steadily returning to normal. Perhaps most conspicuous for everyday Americans is the resumption of collegiate and professional sports. With this bounce back of sentiment, it’s natural that people are considering traveling again. On the surface, this bodes well for Delta Air Lines (NYSE:DAL) and DAL stock.

Of course, there are two ways for industry competitors to recover from the devastation of the coronavirus. First and most obvious is to offer steep discounts to would-be travelers, grabbing as much market share as possible. Later, the companies adopting this tactic can worry about profitability. The second approach is to focus on customer needs, essentially eschewing market share for return business.

Clearly, Delta is going with the latter approach. In an announcement last month, management signaled its commitment to blocking the middle seat and limiting the number of customers per flight through at least Jan. 6, 2021. That’s a major departure from rivals like American Airlines (NASDAQ:AAL), which stated that it will stop social distancing on its flights beginning July 1. From a PR perspective, DAL stock is a standout winner.

Unfortunately, Delta’s feel-good story doesn’t seem to have translated into its financials. According to a CNBC report, the company “is raising $9 billion in a massive debt sale backed by its frequent flyer program.” Further, “The amount is nearly 40% more than the $6.5 billion Delta said earlier this week it intended to raise.”

This move follows American and United Airlines (NASDAQ:UAL), which are also dipping into their frequent flyer programs. Thus, a great story alone won’t save DAL stock.

Economic Concerns Present Major Challenges for DAL Stock

Initially, it appeared that Delta’s executive leadership made the right call regarding the seat blockage. Since the pandemic already gutted air passenger volumes to ridiculously low levels, no one was going to win on absolute terms. Therefore, you might as well win over customer trust for the long haul.

But even against load factors, the company’s strategy may not pan out for DAL stock. As I mentioned in my story for JetBlue Airways

(NASDAQ:JBLU), the load factor for U.S. carriers went from tight margins across the board to highly discrepant. While some of the obvious winners in load factor were ultra-discount specialists like Spirit Airlines (NYSE:SAVE), everybody else, including Delta, had to fight for scraps.

According to the Bureau of Transportation Statistics, in June of this year, Delta’s load factor was 48.76%, a far cry from the 84% it recorded in February. For a bullish argument in DAL stock to be credible, demand must return quickly and substantively.

Click to Enlarge

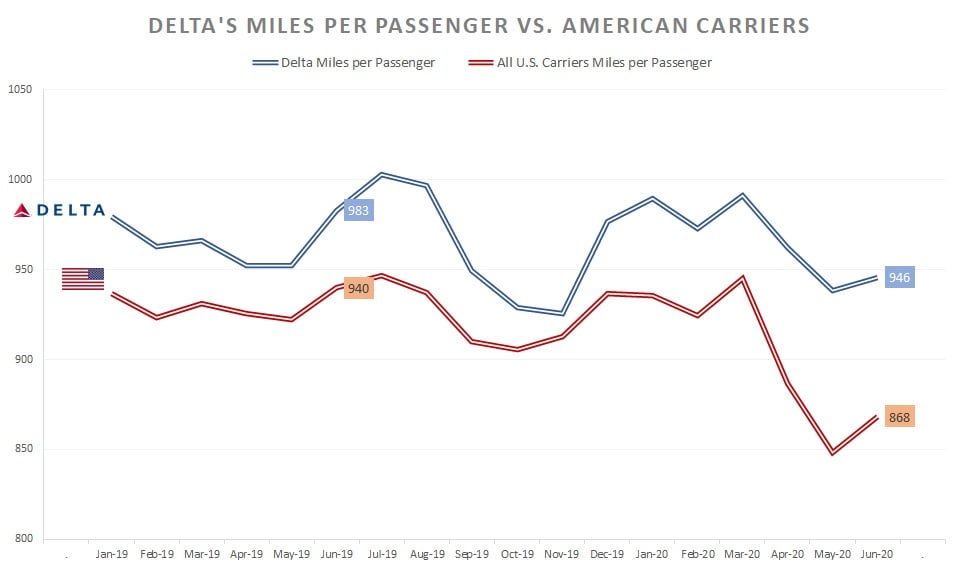

However, I’m not holding my breath. According to the same federal agency, the average miles flown per passenger for U.S. carriers on domestic flights has dipped significantly since the pandemic struck. For instance, in June, U.S. carrier passengers flew an average of 868 miles, down nearly 8% from 940 miles in the year-ago period.

To be fair, Delta looks much better in comparison. During the same period, the company’s average miles per passenger “only” dipped to 946 miles from 983 miles. This was a loss of nearly 4%.

For now, Delta’s passengers appear to be demonstrating loyalty. But how long will this last? As we see from all U.S. carriers, the dip in average miles flown indicates that passengers are flying for trips of necessity, not for business or leisure.

A Second Wave Could Sink Delta

Honestly, if neither commerce nor the travel industry opens, DAL stock is in trouble and it’s not the only one. Obviously, airliners make substantial profit off its business-class passengers. And without the incentive for longer-distance travel, the advantage of flying with Delta versus flying a discount airliner diminishes.

Still, we’re not mentioning the giant gorilla in the room: a second wave of the coronavirus. From what we’re seeing in Europe, loosening restrictions have allowed Covid-19 to infect a new batch of unsuspecting people. Worryingly, BBC.com is reporting a second wave hitting the U.K.

It seems like we never learn. Based on what we experienced this summer, it appears like we’re going to suffer the same fate.

If so, you’d best stay away from DAL stock. Look, it’s no longer about the middle seat and in-flight social distancing. For all the bravado that people display on social media, most folks just aren’t flying. That leaves many airliners trying to subsist on portions of emergency rations. I just don’t see how this is going to work.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.