With novel coronavirus cases still wreaking havoc across the U.S., the gut reaction is to avoid cruise liner investments like Carnival (NYSE:CCL). Early in this pandemic, the cruise ship industry was the poster child of vacations gone awry. It also didn’t help matters for CCL stock that the vessel that sparked the negative PR was the Diamond Princess, a ship under the vast Carnival umbrella.

At the same time, it’s fair to wonder how long the dark cloud will hang over the company. While immediacy bias dictates that we view current events through a sharply pessimistic lens, the reality is that sooner or later, this pandemic will fade. Further, vaccines from Pfizer (NYSE:PFE), Moderna (NASDAQ:MRNA), AstraZeneca (NASDAQ:AZN) and others bode well for CCL stock.

Better yet, pent-up demand indicates that the industry can bounce back once our circumstances normalize. Last month, a report from USA Today indicated that cruise liner bookings were strong for late 2021. Additionally, the Cruise Lines International Association “found that 73% of cruisers say they are ‘likely to cruise’ in the next few years, and 50% say they will cruise within the year.”

Further confirmation came from Carnival’s rivals, such as Norwegian Cruise Line (NYSE:NCLH) and

Royal Caribbean Cruises (NYSE:RCL). Both reported modest upticks in demand for the first half of this year, while the back half demonstrated a robust increase. As well, many of the bookings are from new customers as opposed to those redeeming credits for future journeys.

On the economic front, CCL stock can also bank on encouraging developments. True, the December jobs report wasn’t pleasant, with the economy losing 140,000 jobs. But according to Morgan Stanley, if you exclude losses from the hospitality and leisure sector, the economy really added 403,000 jobs.

Put another way, it’s time to turn that frown upside down for CCL stock. But before you go too deeply contrarian, you may want to consider the possible lingering impact the Covid-19 crisis will have on consumer sentiment.

Can Demand for CCL Stock Sustain Longer Term?

From a technical point-of-view, investors may be encouraged to take a swing for the fences with Carnival. After all, over the trailing six months, CCL stock is up nearly 32%. As well, you have similar enthusiasm for its publicly traded rivals over the same period. Actually, Carnival is the laggard in this trio.

Still, there’s an argument to be made that the pent-up demand narrative is overplayed. Though travel overall improved from the March and April doldrums, we’re talking about comparisons against small numbers. Naturally, the percentage increase will be large. However, overall traffic and movement of people is down against historical norms.

As the pandemic ripples throughout the world, and with SARS-CoV-2 mutating into new strains, that pent-up demand could deflate in a hurry. I’m not saying that it will. Nevertheless, I’m not sure anyone can declare with absolute confidence that extended cabin fever alone can spark a recovery in the broader travel industry.

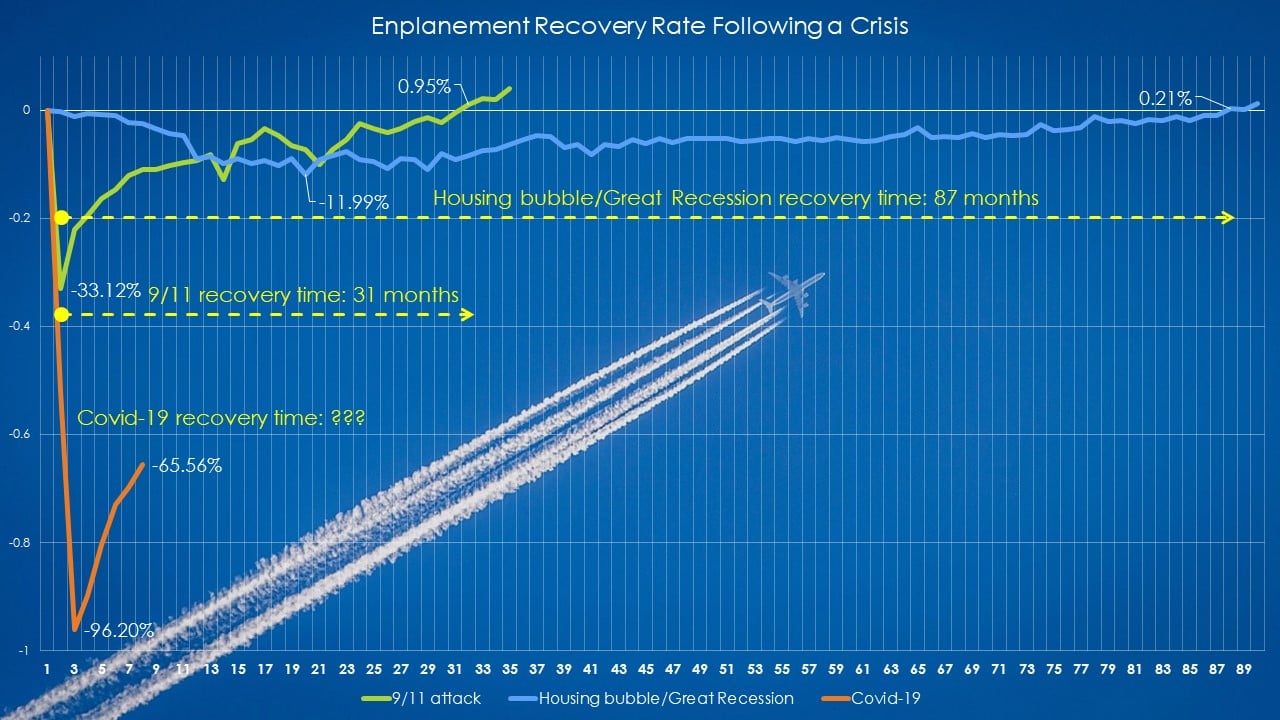

More importantly, we have evidence that, in terms of air travel, demand has been impacted by various crisis events. While flights don’t necessarily correlate with CCL stock, we’re still dealing with a similar platform: a legion of strangers sharing an isolated/enclosed public space.

Click to Enlarge

First, the Sept. 11 terror attack had an immediate impact on air travel demand, just like it did for Covid-19. Not insignificantly, the U.S. Bureau of Transportation Statistics reported a conspicuous dip in vehicle miles driven in September 2001. This suggests that consumer sentiment was wounded across all transportation methods.

Following the hemorrhaging of demand, it took 31 months for air travel to recover to pre-9/11 norms.

Second, the housing bubble, stock market crash and the Great Recession of the late 2000s gradually deflated enplanements. It took more than seven years for demand to normalize to pre-recession levels.

Be Careful with Carnival and Any Cruise Ship Investment

Though I can’t say for sure how long investments like CCL stock will be negatively affected, I’d say that around three years of softness is a reasonable forecast.

First, consumers already knew well before Covid-19 that cruise ships were floating Petri dishes. If you’ve got the stomach for it or won’t go cruising for a while, check out the unpleasantries that apparently occur on board. While I’m sure standards will improve in the post-Covid era, I’m also sure that many won’t trust such promises.

And that brings me to my second point. According to academic research, the 1918 influenza pandemic eroded social trust in many impacted nations. You can point to any random outbursts this past trailing year to find clues that not much has changed.

Third and finally, the pandemic is as much a health crisis as it is an economic one. Here, countering data refutes Morgan Stanley’s optimistic time. For instance, Axios points out that while professional and business services jobs saw the biggest nominal growth, “over 40% of the gains were in temporary help services, limited gigs that may or may not turn into longer-term work.”

Therefore, the combination of pandemic and financial woes in my view indicates that a three-year window of softness is not out of the question. If you’re going to gamble on CCL stock, you should do so with this margin in mind.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.