Speculation about Alibaba (NYSE:BABA) stock has been making headlines since the scrutiny on Chinese ADR listings and data acquisitions started. And retail opinions on the stock market have increased immensely over the past year during a period when the S&P 500 hasn’t suffered a pullback of more than 5%.

As a result of minor pullbacks, many traders have benefitted from buying the dips. But the dangers of doing need to be fully conveyed to many others. Just because Alibaba’s stock price has decreased significantly doesn’t mean it will return to previous heights.

Let me outline the key reasons why this topic isn’t a matter of basic intuition.

Systemic Clarity for BABA Stock

Let’s start off with the primary topic of debate, which is the new policies proposed by China and the United States.

When you embark on pricing an asset, you need to choose at least two systemic factors and analyze the asset’s sensitivity to each. China’s economic growth can’t be questioned, so I decided to factor in geopolitical risk and regulation. The stock’s sensitivity to these factors has been there for all to see; Alibaba stock has decreased by more than 20% in the past three months alone.

Both political and regulatory issues stem from data concerns.

The predominant manner in which mature-stage technology companies add value is through data and intangible asset acquisitions. Data acquisitions allow for better consumer information, subsequently resulting in a more efficient business.

Asset acquisitions refer to acquisitions of scalable, innovative solutions created by earlier stage companies that can provide the acquirer with a more rapid expansion (rather than internal development), subsequently fending off the competition of rivals.

Let’s dissect the two factors.

- Politics: The United States has long seen China as a threat to national security and has clearly become uncomfortable with Chinese companies gaining access to U.S. consumer data and capital. On the other side of the playing field is the Chinese Communist Party. They are not comfortable with big technology firms gaining the power that Facebook (NASDAQ:FB), Alphabet’s (NASDAQ:GOOG, NASDAQ:GOOGL) Google, and Amazon (NASDAQ:AMZN) have in the United States. This double-ended effort to curb the power of these companies has caused restrictions on future access to capital and hypergrowth expansion for Alibaba, which has been amplified by regulatory body interventions.

- Regulation: As if the political headwind isn’t enough. The Securities and Exchange Commission has also started demanding transparency from Alibaba regarding its reporting. Alibaba Group Holdings ADR (American Depositary Receipt) is a shell company, and the financial transparency of the underlying business has been questioned. Furthermore, both the Chinese Government and the Federal Trade Committee are cracking down on big-tech acquisitions. There have been concerns that anticompetitive behavior arises from securities fraud; this is because many big tech companies complete acquisitions at premiums to simply overpower their competition.

Why should this matter so much to BABA stock?

As mentioned, a significant part of a tech company’s growth is due to data and asset acquisitions. Alibaba has made more than 170 investments and acquisitions; if it can’t resume this rapid investment rate, it will lose ground on rising competitors, and its enterprise value growth may come to a standstill. It’s for this reason that these policies will affect Alibaba more than most.

Fundamental Factors

Now, let’s set that aside for the moment. Let’s imagine a world where systemic matters didn’t play a role, and fundamentals were all we cared about. Most categorize Alibaba as a hybrid between growth, defensive value and cyclical value.

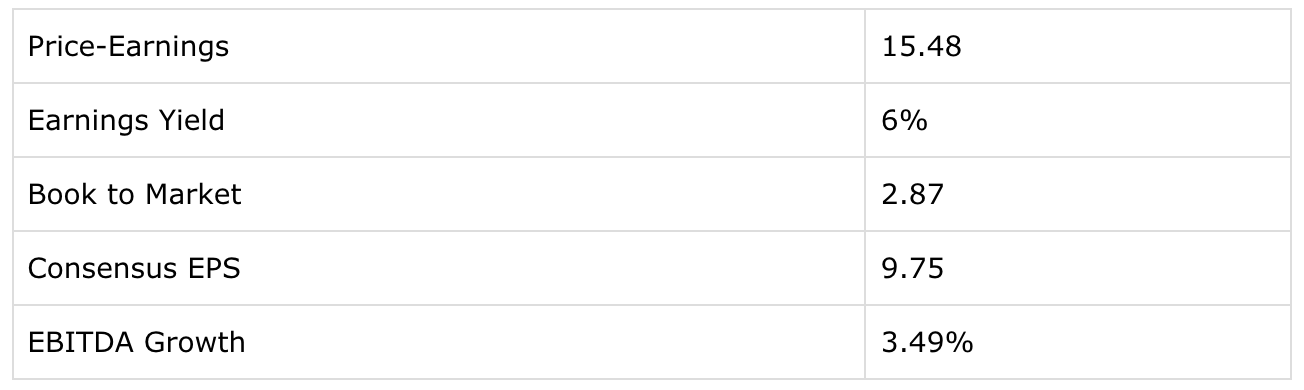

For this reason, we need to look at the following ratios:

- Earnings Yield and Price-Earnings (Defensive Value)

- Book to Market (Cyclical Value)

- Consensus Earnings and Earnings Growth (Growth)

Source: Author via Seeking Alpha

Based on the outlined multiples at the time of writing, Alibaba is an average stock, which could experience little to no upside in a non-systemically influenced market. Its P/E ratio was 5.02% higher than the sector median, while its expected EPS for March 2022 is anticipated to shrink by 3.47%.

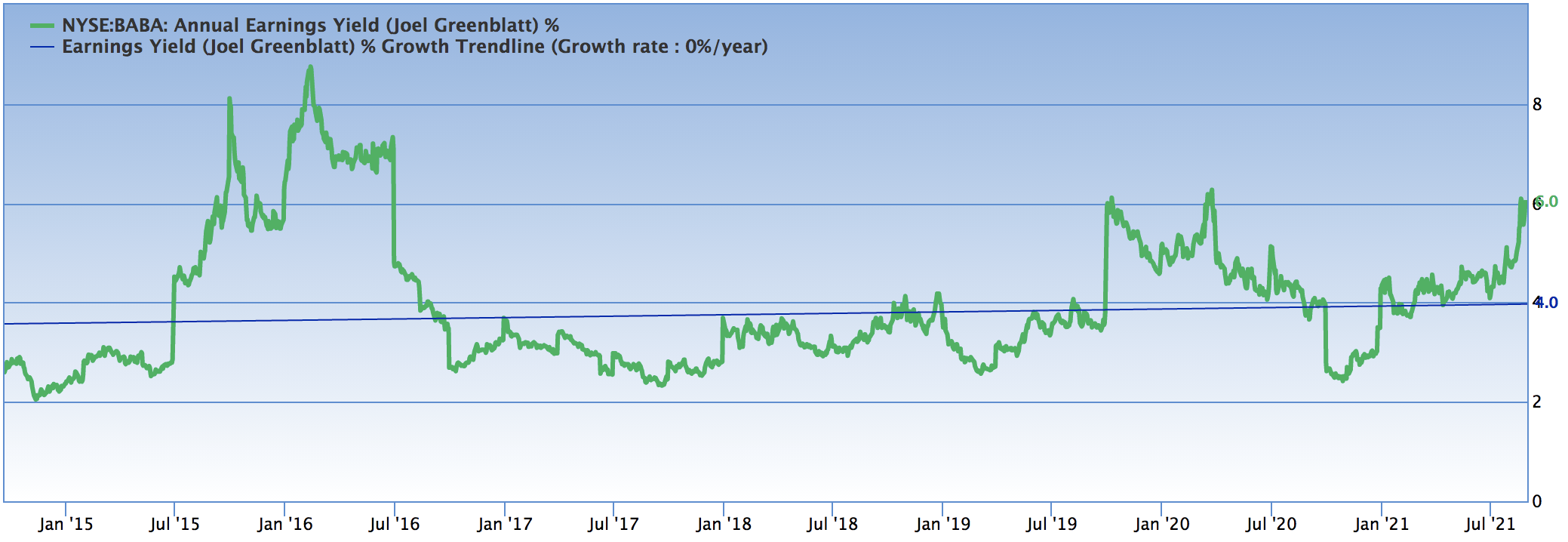

The company’s earnings growth paints a grim picture as its year-over-year EBITDA growth is 62.86% below the sector average, and its earnings yield has failed to breach the 7% level since 2017.

Source: Gurufocus

The only positive we can draw from the relative analysis is that Alibaba’s price to book multiple is marginally below the generally accepted benchmark (3.00).

There really is no way to justify a higher share price; many Wall Street analysts have assigned buy ratings to the stock over the past 12 months, but I believe that they’ve ignored basic theory and opted to price the stock based on subjective thoughts alone.

BABA stock is under severe pressure, so let me repeat the important info I mentioned in the opening paragraph — just because the stock has lost value doesn’t mean it’s a pullback buy!

On the date of publication, Steve Booyens did not hold any long or short positions in any of the securities mentioned. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Steve Booyens co-founded Pearl Gray Equity and Research in 2020 and has been responsible for equity research and PR ever since. Before founding the firm, Steve spent time working in various finance roles in London and South Africa, and his articles are published on various reputable web pages such as Seeking Alpha, Benzinga, Gurufocus, and Yahoo Finance. Steve’s content for InvestorPlace includes stock recommendations, with occasional articles on crowdfunding, cryptocurrency, and ESG.