Many investors may be seeking answers on where to invest during the current market climate. After all, some of the stocks that have provided us with such joy for most of 2021 are getting battered and bruised. Meme stocks are running out of steam. Healthcare stocks that got a pandemic boost are, in some cases, starting to falter.

Where should a careful investor look now?

It’s times like these that we need to remember a few basic principles of investing, and one of the best principles I know of is putting the defense on the field when there’s a risk-off attitude. Right now, the market’s worried about economic variables such as inflation, higher interest rates in 2022, and the impact of China’s hard-line economic policies.

It’s the perfect time to look at a defensive rotation, and I’m focusing specifically on healthcare stocks today. The energy sector has lead the way over the past few weeks, but I firmly believe that the healthcare sector is next up to the plate.

Here are my top picks for October.

- UnitedHealth Corporation (NYSE:UNH)

- Anthem (NYSE:ANTM)

- CVS Health (NYSE:CVS)

- Pfizer (NYSE:PFE)

- Medtronic (NYSE:MDT)

- Catalent (NYSE:CTLT)

- Teladoc (NYSE:TDOC)

Healthcare Stocks: UnitedHealth Corporation (UNH)

UnitedHealth is a diversified healthcare company in the United States with a significant foothold in the medical insurance space. The company beat its second-quarter guidance in July by posting revenue worth $71.3 billion, a gain of 14.8% year-over-year, and an earnings-per-share of $4.46.

Based on its price ratios, United Health trades at a discount to the broader sector with its price-earnings and price-sales trading at benchmark discounts of 21.9% and 82%, respectively.

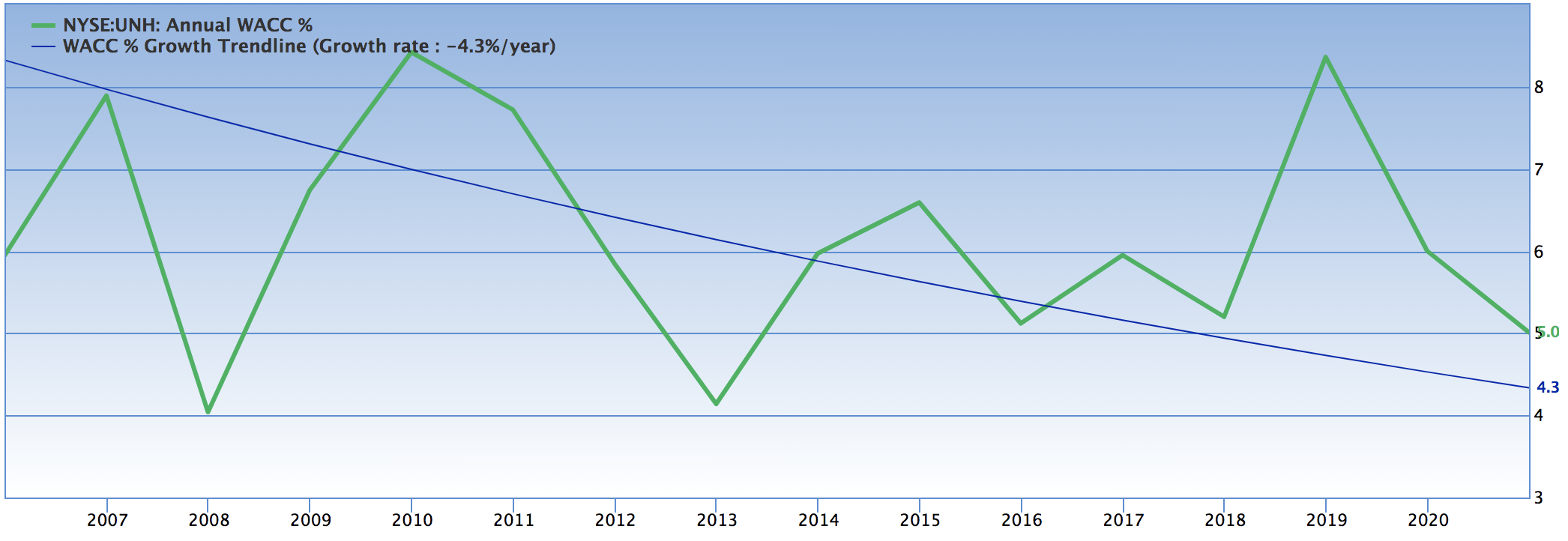

Looking at the firm’s pricing metrics in isolation suggests the stock could reach significant heights. United Health has managed to decrease its cost of capital significantly while providing a surplus return on invested capital of 8.72%.

Source: Gurufocus

The recent improvements in the firm’s WACC (weighted average cost of capital) coupled with a five-year net income constant annual growth rate of 18.62% means that investors’ residual has improved significantly.

Ricky Goldwasser of Morgan Stanley recently reiterated her appreciation of UnitedHealth stock and placed a $488 price target.

Anthem (ANTM)

Anthem is part of the same peer group as UnitedHealth, but it’s a higher-Beta (1.01) stock. This essentially just means that it’s a more speculative bet, but it could pose superior returns to both the S&P 500 and UnitedHealth.

The company beat its second-quarter earnings estimates and came in strong with operating revenue of $33.3 billion. Anthem’s success was driven by higher premium revenue — that segment rose by 13.7% year-over-year — and product revenue growth of 19.6% year-over-year.

I think the stock is in a good space, with an earnings yield of 3.6% during a period in which it’s also managed to decrease its cost of capital by a significant amount.

The stock’s price-earnings ratio of 22.1 is currently trading at a 33.5% discount to the sector, and its dividend is yielding 1.2% with a five-year growth rate of 11%. All aspects considered, Anthem is an excellent investment. Matt Borsch of BMO Capital seems to agree with me, having placed a $465 price target on the stock.

Healthcare Stocks: CVS Health (CVS)

This pharmaceutical powerhouse was a Michael Burry favorite earlier this year, when he bought a bunch of call options.

The optimism has faded, as few still include CVS in their investment idea conversations, but I’m still very optimistic about the stock. CVS is a dividend play in my opinion; its net income margin of 2.6% is at a five-year high, while its EPS guidance for the year was lifted by 10 cents after the company’s blockbuster second-quarter results, which saw it beat revenue estimates by more than $2 billion.

Switching focus to the stock’s value, CVS is trading at a 50% discount to the sector. George Hill of Deutsche Bank recently maintained his “buy” rating on the stock with a $101 price target.

Pfizer (PFE)

It might seem obvious to many that

Pfizer is a stock you’d want to own when it’s making the vaccines for a pandemic, but it’s always a question of cost outlay versus cash inflow. Plenty of capital went into research & development before Pfizer could roll out their vaccine.

Still, I believe the tradeoff ended up being positive, especially if you consider the boosters shots that are to follow.

Pfizer’s R&D expenses grew considerably in 2020 and an additional 68% year-to-date. However, the biotech giant has managed to match the cost with revenue and operating income; Pfizer’s year-over-year EBITDA growth is 1,783% higher than its five-year average, and its free cash flow margin is 148.45% higher than its 5-year average.

The stock’s earnings-per-share is anticipated to grow by an additional 153% in the final quarter of this year. If we use a price multiple such as price-earnings of 19.4 and multiply it by the estimated earnings-per-share for 2021, we find an implied price target of $78.96, worth roughly 88% in upside.

Some of this value will get diluted because of the stock’s high dividend payout ratio of 38.36%, but I think it’s safe to say that we’re looking at an undervalued asset.

Healthcare Stocks: Medtronic (MDT)

Medtronic is a producer and supplier of specialized medical devices. This stock is a reversal play, the relative strength index has a reading of around the middle 60s for the majority of this year before it suddenly plunged into the middle 30’s this month, which is near oversold territory (below 30).

The sporadic drawdown was probably an overreaction to the news that the company is tightening its full-year earnings guidance. I think it’s a brilliant opportunity to buy into the overreaction, with the stock trading at a sector price-sales discount of around 30% while also beating the sector average EBIT growth by an impressive 82.71%.

Wells Fargo recently upgraded its price target on the stock to $151 from $140, as it believes the delta variant’s effects on supply chains are transitory.

Catalent (CTLT)

Catalent is a drug research, design, and manufacturing firm with a strong foothold throughout the entire drug creation value chain.

Many retail traders have overlooked the stock but I added it to my portfolio last year September and have enjoyed the incredible 50%-plus ride ever since.

Catalent recently beat its fourth-quarter earnings estimates, producing a revenue beat of $50 million, and an earnings-per-share beat of 15 cents. The company provides full-year guidance and anticipates revenue growth of between 8%-13%. It also expects adjusted net income to be between $585 million and $650 million.

Catalent is currently trading above its 50-, 100- and 200-day moving averages with no sign of slowing down. Wall Street remains adamant that the stock will continue to succeed, with Bank of America being the last to reiterate a “buy” rating at a price target of $168.

Healthcare Stocks: Teladoc (TDOC)

Teladoc is one of the truest buy-the-dip opportunities in the healthcare stocks. TDOC has lost more than a third of its value year-to-date due to aggressive acquisitions in 2020, such as that of Livongo Health. Once investors start to fathom that this is a company that has grown its revenue by 127.42% over the past year and is expected to grow its free cash flow by 157.91% over the next year, we’ll see a snowball of capital flow into Teladoc’s stock.

Teladoc also holds a year-over-year CAPEX increase of 73.92% and an interest coverage ratio of 6.91, so there really is no reason to be concerned about a lack of liquidity after all its recent acquisitions.

The stock is oversold with an RSI figure in the low 30s; I don’t think it will be long before investors recognize Teladoc’s true potential. Sean Dodge of RBC capital believes Teladoc is a lucrative buying opportunity and has placed a $260 price target on the stock.

On the date of publication, Steve Booyens held long positions in UNH, CVS, CTLT. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Steve Booyens co-founded Pearl Gray Equity and Research in 2020 and has been responsible for equity research and PR ever since. Before founding the firm, Steve spent time working in various finance roles in London and South Africa, and his articles are published on various reputable web pages such as Seeking Alpha, Benzinga, Gurufocus, and Yahoo Finance. Steve’s content for InvestorPlace includes stock recommendations, with occasional articles on crowdfunding, cryptocurrency, and ESG.