I found seven low price-to-earnings (P/E) value stocks that are poised to rebound significantly this year. They are:

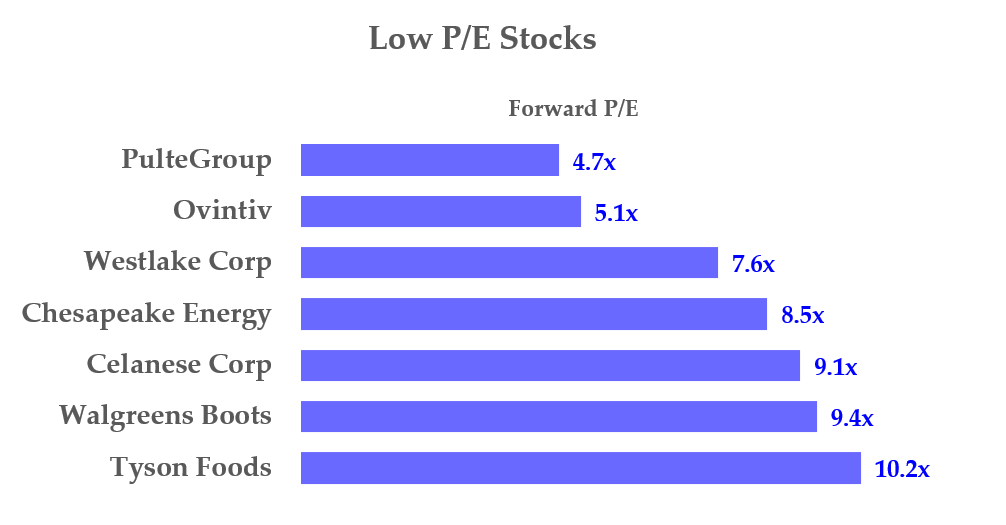

- Pulte Group (NYSE:PHM) — Homebuilder with a 4.7x forward P/E, 1.2% dividend yield, and strong earnings

- Ovintiv (NYSE:OVV) — Permian Basin oil and gas producer — 5.1x forward P/E, 1.6% yield, strong earnings growth

- Westlake Corp (NYSE:WLK) — Upstream petrochemical producer – 7.6x forward P/E, 1% yield, strong cash flow

- Chesapeake Energy Corp (NASDAQ:CHK) — Oil and gas developer — 8.1x forward P/E, 3.7% yield, earnings growth

- Celanese Corp (NYSE:CE) — a global plastics maker with a 9.1x forward P/E, a 1.9% dividend, and huge cash flow

- Walgreens Boots Alliance (NYSE:WBA) — Global retailer with a forward P/E below 10x and a 4.0% yield

- Tyson Foods (NYSE:TSN) — Chicken, pork, and prepared foods maker — 10x forward P/E, 2.1% yield, inflation play

These seven stocks have traditional value characteristics, including having forward P/Es at 10x or lower, paying a dividend, and having positive earnings forecasts. Moreover, the investor in these value stocks can expect that they have good potential upside since they are so cheap.

The theory behind this is, as J.P. Morgan Chase’s (NYSE:JPM) Wealth Management says, a low P/E stock generally indicates that it may be undervalued. Moreover, by using a “forward” earnings estimate in the P/E calculation we are using an “educated guess” of future earnings. This is as opposed to using trailing earnings in the calculation.

For example, these seven stocks are ranked from lowest forward P/E to highest, are all U.S. companies, as can be seen in the chart on the right.

Click to Enlarge

In addition, all these stocks pay a dividend and have expected earnings growth or high free cash flow (FCF). Moreover, a number of these companies have large share buyback programs, which I will indicate. These can act as catalysts for these value stocks to rise to higher valuations.

There are many other companies we could have put on this list, so we arbitrarily limited it to value stocks with a forward P/E of 10x or less, plus all the other criteria. It should be noted that we used Refinitiv analyst survey data as seen in Yahoo! Finance Statistics page tabs.

Let’s dive in and look at these value stocks further.

| PHM | Pulte Group | $48.43 |

| OVV | Ovintiv | $47.98 |

| WLK | Westlake Corp | $123.93 |

| CHK | Chesapeake Energy Corp | $78.51 |

| CE | Celanese Corp | $142.85 |

| WBA | Walgreens Boots Alliance | $47.36 |

| TSN | Tyson Foods | $87.14 |

PulteGroup (PHM)

Market Capitalization: 12.0 billion

Forward P/E: 4.7x

PulteGroup is the third-largest homebuilder in the U.S. with operations in 23 states and 42 major markets. Its leading home brands are Centex, Pulte, Del Webb, DiVosta, John Wieland Homes and Neighborhoods, and American West.

Last year Pulte’s revenue rose over 26% to $13.57 billion and fourth quarter sales were up 38% to $4.2 billion. Its Q4 adj. net income rose 64% to $2.51 per share. The company said it now has a unit backlog of 18,003, down slightly from the prior quarter, and prior year. However, analysts now look for earnings to rise 39.8% to $10.25 per share, up from $7.33 last year.

That gives PHM stock a forward P/E of just 4.7x. Along with its 15 cents quarterly dividend ($0.60 annually), its annual dividend yield on the March 18 price of $48.43 is 1.2%. This makes it clearly one of the best low P/E value stocks out there. Moreover, PulteGroup spent $897 million repurchasing 17.1 million shares last year, or a 6% total reduction of shares outstanding. That is the same as a 6% buyback yield for shareholders, as it lifts earnings per share (EPS) and eventually allows higher dividends per share.

As a result, combined with its 1.2% dividend yield, PHM stock has an attractive 7.2% total yield. This gives the stock significant upside potential. For example, the average analyst target price surveyed by TipRanks is $67.33, an upside of 39%.

Ovintiv (OVV)

Market Cap: $12.3 billion

Forward P/E: 5.1x

Ovintiv is a Denver-based oil and natural gas producer, marketer. Its principal assets are in the Texas Permian Basin as well as in Anadarko in west-central Oklahoma, and Montney in northeast British Columbia and northwest Alberta.

The company expects to produce significantly larger amounts of oil and gas this year. Analysts expect earnings will rise to $9.45 per share, up from $5.32 last year. At $47.98 on March 18, that puts OVV stock on a forward P/E of 5.1x.

Moreover, Ovintiv recently increased its quarterly dividend rate by 43% to 20 cents, putting the annual dividend yield at 1.67%. This shows its extreme optimism about the company’s cash flow prospects going forward.

In addition, it has been paying down debt and repurchasing shares. In fact, it plans on buying back shares equal to one-quarter of its free cash flow after paying dividends, or $71 million. From the end of Q4 2021, it has bought back 4.3 million shares to date since the beginning of Q4 2021, including 3.1 million during Q4.

That represents about 1.67% of its 258 million shares outstanding, implying an annual buyback yield of 3x times amount or 5.0%. So combined with its 1.67% dividend yield, this gives OVV stock a total yield of 6.67% for shareholders. It will act as a major catalyst pushing OVV stock much higher.

Westlake (WLK)

Market Cap: $15.3 billion

Forward P/E: 7.6x

Westlake Corp, not to be confused with Westlake Chemical Partners LP (NYSE:

WLKP), supplies petrochemicals, polymers, and building products worldwide. In short, it controls companies that make PVC, the third-most widely produced synthetic type of plastic. PVC is used to make rigid pipes, doors, windows, plastic bottles, even credit/debit cards. It is made from fracked methane gas from shale and converted into ethylene. Westlake has three such ethylene plants.

Last year the company made $15.58 in EPS and this year analysts forecast earnings of $16.23. Therefore, at $123.93 as of Friday, March 18, WLK stock has a forward P/E of 7.6x.

Westlake pays out a quarterly dividend of 29.75 cents or $1.19 annually. At today’s price, that gives it a dividend yield of almost 1% (o.96%). It is also likely to pay a higher dividend soon after the upcoming 4th consecutive quarterly payment at this rate. The company also purchases a small number of its shares but it does not amount to much.

This is a solid value stock with good earnings growth and the potential for a much higher P/E multiple and dividend.

Chesapeake Energy (CHK)

Market Cap: $10 billion

Forward P/E: 8.5x

Chesapeake Energy is an independent exploration & production (E&P) oil and gas company. Its main assets are in the Marcellus Shale in the northern Appalachian Basin in Pennsylvania and the Haynesville/Bossier Shales in northwestern Louisiana; and the liquids-rich resource play in the Eagle Ford Shale in South Texas.

Last year Chesapeake made $7.88 per share and this year 12 analysts forecast EPS of $9.2 per share. This puts CHK stock on a forward P/E of 8.5x at $78.51 per share on March 18.

In addition, Chesapeake has a very interesting dividend structure. It pays a base dividend of 43.75 cents per share quarterly, or $1.75 annually. That represents a base dividend yield of 2.23%. In addition, it pays out 50% of the quarterly free cash flow after the base dividend payment in a variable dividend. This past quarter that worked out to $1.33 per share, as can be seen on page two or its earnings report. The total dividend per share was $1.7675 for the quarter.

We can estimate the FCF less the base dividends for the year. But for simplicity’s sake, let’s say that the FCF will be the same as the Q4 rate, less 20% to be conservative. That brings the quarterly variable dividend to $1.064, or $4.256 annually. After adding the $1.75 base dividend, the total potential dividend this year to $6.006, or let’s just say $6 annually.

Therefore, the annual yield is 7.64% (i.e., $6.00/$78.51). In addition, the company announced a $1 billion common stock and warrant repurchase program that will be executed by the end of 2023. That works out to about 10% of its $1 billion market cap, or a 5% annual buyback yield. This brings its total yield to roughly 17.64% annually. Expect good things to happen with CHK stock this year.

Celanese (CE)

Market Cap: $15.4 billion

Forward P/E: 9.1x

Celanese Corp makes high-performance engineered polymers (e.g. plastics). It is extremely profitable – last year the company generated $1.263 billion in free cash flow (FCF). Not only was that a high FCF margin (14.8% of $8.54 billion in sales), but it also represents 8.2% of its market value (8.2% FCF yield).

As a result, analysts are still bullish on the stock. The average EPS estimate of 23 analysts is $15.70 for 2022. That puts it on a forward P/E of 9.1x at the price on March 18 of $142.85.

Along with its annualized $2.72 dividend per share, which gives it a yield of 1.9%, this makes it one of the value stocks worth buying. Interestingly, the company has now paid out the same quarterly rate for 5 quarters, so it might be considering raising the dividend per share rate soon.

In addition, Celanese bought back $1 billion worth of its shares last year. That works out to a buyback yield of 6.49% of its $15.4 billion market capitalization. As a result, the total yield of CE stock is 8.39%. This makes it a very attractive investment opportunity for most value investors.

Walgreens Boot Alliance (WBA)

Market Cap: $41 billion

Forward P/E: 9.4x

Walgreens is a US and international pharmacy-led retail group. It operates under the Walgreens and Duane Reade brands in the U.S. along with five others and also is in the U.K., Thailand, Germany, Norway, Ireland, and other countries.

Last year ending Aug. 31, Walgreens earned $2.93 per share, and analysts forecast $5.03 per share this year. At $47.36 as of March 18, that puts WBA stock on a forward P/E of 9.4x.

Moreover, the company has paid out three quarterly payments of 47.75 cents per share in dividends, putting it at an annualized rate of $1.91. That gives WBA stock a dividend yield of 4%. After this upcoming fourth payment at this rate, expect that management will likely incrementally raise that dividend, which automatically raises the yield. In the past year, the company has not emphasized any buyback program it has.

Nevertheless, this is a growing retailer, with solid financials, a low P/E, and a high dividend yield. That makes it one of the traditional value stocks.

Tyson Foods (TSN)

Market Cap: $31.8 billion

Forward P/E: 10.2x

Tyson is one of the world’s largest food (protein) firms, making beef, pork, chicken, and prepared foods by processing cattle and hogs. Some of its familiar brand names are Tyson chicken, Ball Park Franks, Jimmy Dean sausage, Hillshire Farm, and State Fair.

Recently the company reported Adj. EPS up 48% for its fiscal first quarter ending Jan. 1, 2022. For the year ended Oct. 2, 2021, it made $8.34 per share, up 47.8% year-over-year. In addition, 13 analysts project sales this year of at least $8.53, putting it on a forward P/E of 10.2 at a price of $87.14 as of March 18. If earnings come through higher than expected as last year, expect to see an even lower P/E multiple.

The company talks at length about “logistics cost inflation”, “accelerated inflation”, and “persistent inflationary” pressures. But it has pricing power and has raised its own prices to consumers. Indeed, its latest quarterly report said that “Our record 2021 performance demonstrates the ability of our employees and business models to preserve our profitability amid inflation.”

In the past three calendar quarters, Tyson has paid out a quarterly dividend of 46 cents, putting it at an annualized rate of $1.84. After this next upcoming dividend payment Tyson is likely to hike the quarterly rate, which will act as a catalyst for TSN stock. Nevertheless, at today’s rate, the stock has a dividend yield of 2.1%, which is very attractive to value investors.

Moreover, Tyson bought back 4.2 million shares in its Q1 ending Jan. 2. That represents 1.1% of its diluted shares outstanding, putting it on a buyback yield of 4.4% annually. Therefore, the total yield to investors is about 6.5%.

In effect, this is an inflation play with earnings power, a low P/E, a good yield, and a nice buyback program. This makes it one of the best attractive low P/E value stocks.

On the date of publication, Mark Hake did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.