If you’re looking for the best growth stocks to buy and hold through 2030, you should look into the many solid businesses other than the top tech mega-caps. I believe expanding your core growth holdings into some of these quality businesses is a good idea, as they have sticky revenues and solid growth over the coming years.

Growth stocks have been driving the market recently, and that is unlikely to change anytime soon. These companies have solid growth that should allow them to beat the market over the long run. That said, profitability will make or break companies, and the ones I will be discussing today have plenty, or at least are expected to, in the near future.

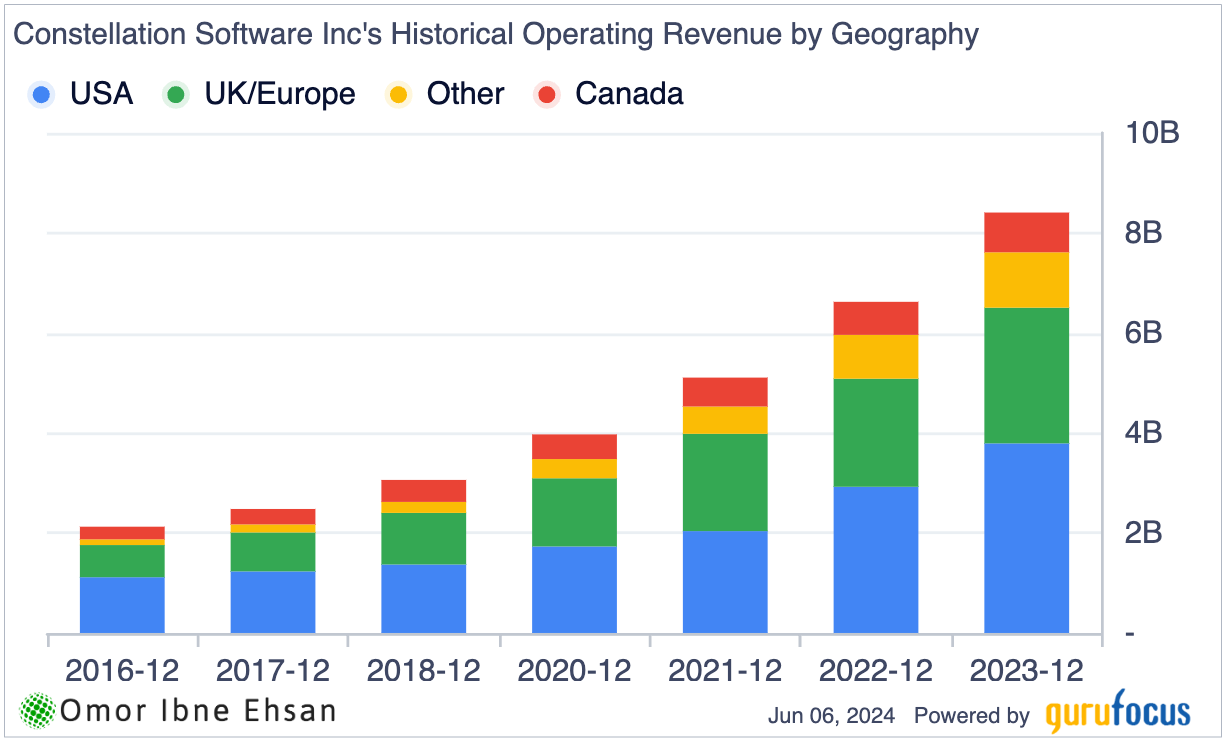

Constellation Software (CNSWF)

Constellation Software (OTCMKTS:CNSWF) provides software and services to select public and private sector markets. This Canadian software powerhouse has been a compounding machine for years, making it one of the most reliable and influential stocks in the nation’s tech sector. I believe this stock is poised to rapidly rebound from any dip given its rock-solid fundamentals. This company is also far more geographically diversified than you’d think.

Click to Enlarge

In Q4, revenue surged 26% year-over-year to $2.35 billion. For the full year, sales skyrocketed 27% to $8.41 billion. Analysts expect this momentum to persist, with revenue projected to double within the next four years at a roughly 20% annual growth clip.

Yet astoundingly, CSU trades at a mere six times sales. For a software juggernaut of this caliber, that’s an absolute steal.

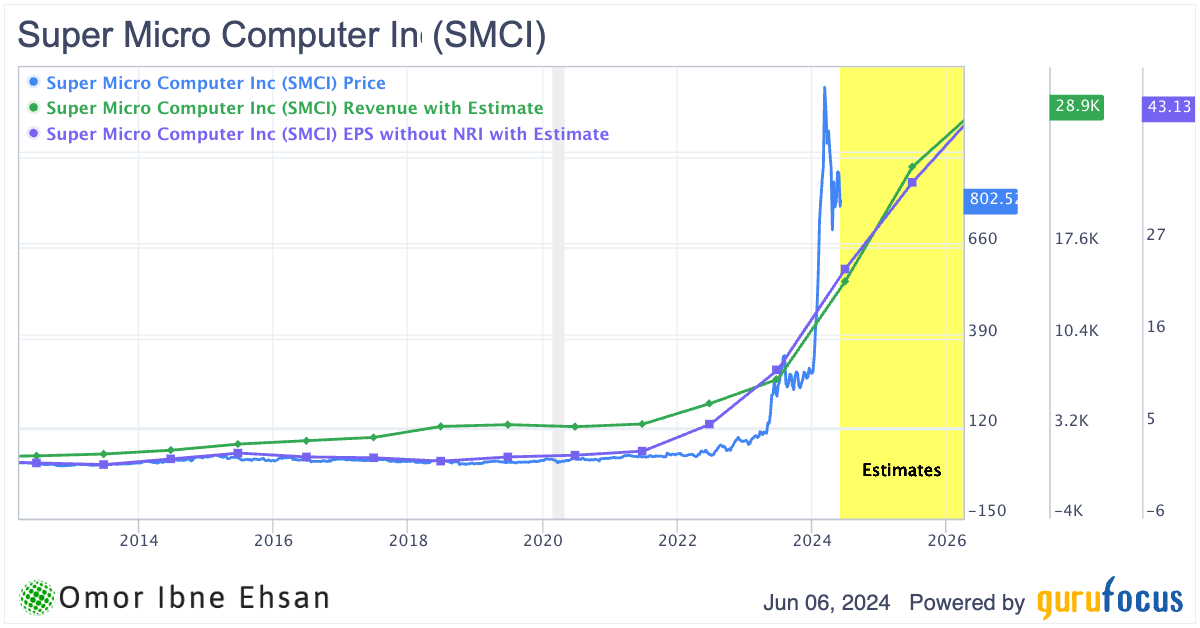

Super Micro Computer (SMCI)

Super Micro Computer (NASDAQ:SMCI) provides high-performance server and storage solutions. The company is riding high on the AI revolution, delivering record-breaking results in Q3, with revenue surging 200% YOY to $3.85 billion and non-GAAP EPS skyrocketing 308% to $6.65.

I believe the debate around an AI bubble is valid, but SMCI’s fundamentals suggest it’s a compelling buy in the space. The company is investing significantly in production, operations and liquid cooling technology to meet the soaring demand for its rack-scale AI solutions. Despite the stock’s meteoric rise, SMCI trades at just 34 times forward earnings and three times sales, a bargain compared to many frothier AI plays.

Click to Enlarge

I expect SMCI to handily double its sales and EPS over the next two years as it capitalizes on the AI megatrend. With a pristine balance sheet bolstered by a recent $3.28 billion capital raise, SMCI has the firepower to scale aggressively. For growth investors, I recommend accumulating shares on any dips, as this AI juggernaut is just getting started.

The Trade Desk (TTD)

The Trade Desk (NASDAQ:TTD) operates a leading demand-side platform for digital advertising. I believe this is one of the highest-quality growth stocks you can buy and hold until 2030.

In Q1, revenue surged 28% YOY to $491 million, highlighting the rapid adoption of programmatic advertising. CEO Jeff Green noted that over 90% of the top 200 global advertisers have run campaigns on their platform in the last 12 months.

CTV continues to be their fastest-growing channel as industry giants like Disney (NYSE:DIS), NBCU, and Roku (NASDAQ:ROKU) double down on streaming. The open internet is being replumbed and revalued, especially compared to walled gardens. Trade Desk’s Kokai platform helps clients fully leverage data-driven buying to fuel their growth in this environment.

With the shift to digital advertising accelerating and the $1 trillion TAM up for grabs, I’m incredibly bullish on Trade Desk’s ability to outperform over the long run. The future looks very bright here, too.

If you’re looking for a high-conviction growth stock, Trade Desk absolutely belongs in your portfolio.

Pinduoduo Holdings (PDD)

Pinduoduo Holdings (NASDAQ:PDD) operates a leading e-commerce platform in China. I believe PDD is one of the most compelling growth stocks to buy and hold until 2030. In Q1, PDD’s revenue surged an astounding 131% YOY to $11.99 billion, blowing away estimates by $1.41 billion.

This momentum is undeniable. PDD is a rare Chinese company that successfully brought its model to the U.S. through its Temu app, which has consistently ranked as the most downloaded shopping app. Temu is rapidly popularizing Chinese-style bargain e-commerce stateside.

While most Chinese stocks have been shattered, PDD’s international expansion gives it a major edge to keep compounding. Management’s focus on supporting high-quality consumption, broadening supply, and promoting a robust ecosystem positions PDD for sustainable growth.

Yes, near-term challenges may arise as PDD invests heavily in the future. But I’m confident its long-term orientation will handsomely reward patient investors. PDD’s unique domestic dominance and international momentum mix make it a top pick. Analysts think it can cross $200 within the next 12 months.

Click to Enlarge

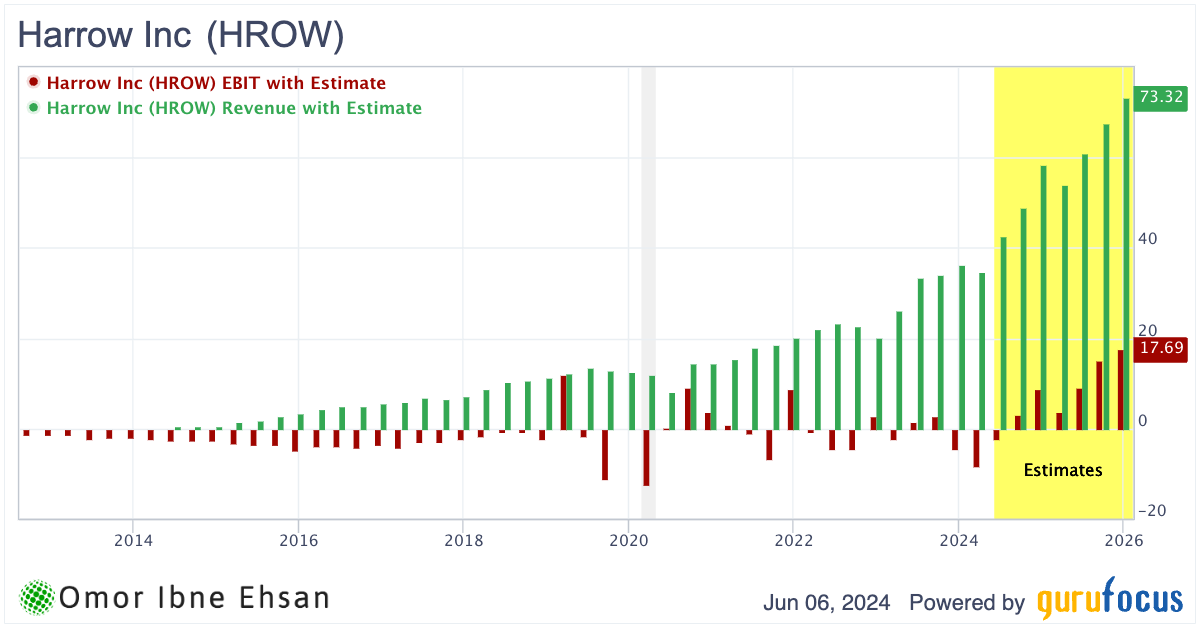

Harrow (HROW)

Harrow (NASDAQ:HROW) is a pharmaceutical company focused on developing ophthalmic drugs and technologies. The stock is a riskier bet than other growth stocks, with higher volatility. However, I believe Harrow’s long-term prospects are compelling, supported by the increasing prevalence of eye problems in today’s screen-obsessed world. Kids are growing up with screens glued to their hands, and while there’s a lot of debate around why so many people have eye problems today, I think everyone can agree that screens are involved in some form. HROW stock seems like a solid way to benefit from this.

The company posted strong revenue growth of 33% YOY, reaching $34.6 million in Q1 2024. While Harrow missed EPS estimates by $0.17 with a loss of 38 cents, the launch of VEVYE, its flagship dry eye treatment, is showing promising early results. New prescriptions are ramping up month-over-month, and the company is now seeing its fifth refill cycle, which is where the true value lies for stockholders.

Harrow is expected to turn profitable next year and significantly grow its profits, with the stock trading at just six times 2027 EPS estimates.

Click to Enlarge

Revenue is projected to grow nearly 40% this year and double over the next six years. The stock has already recovered 50% year-to-date, and I believe it has further room to run.

Taiwan Semiconductor (TSM)

Taiwan Semiconductor Manufacturing Company (NYSE:TSM) is the world’s largest dedicated semiconductor foundry. Despite its impressive rise over the past few years, I believe TSM’s valuation still doesn’t fully reflect its critical role in the global semiconductor supply chain. In Q1 2024, TSM reported revenue of $18.23 billion, up 9.7% YOY, and EPS of $1.38, beating estimates by 6 cents. Advanced technologies (7nm and below) accounted for a whopping 65% of wafer revenue.

While geopolitical risks surrounding Taiwan persist, I think the market overestimates their potential impact on TSM. Even if tensions escalate, TSM’s global customer base and expanding U.S. presence provide a buffer. Plus, any disruption would likely hurt fabless chipmakers more than TSM itself. Nvidia (NASDAQ:NVDA) alone has nearly 4x the market cap of TSM right now, and this company won’t function without Taiwan Semiconductor. I also expect Nvidia’s pricing power to start extending into TSMC.

Chipmakers will also be able to source from TSM right in the U.S. once its factory in Arizona comes online.

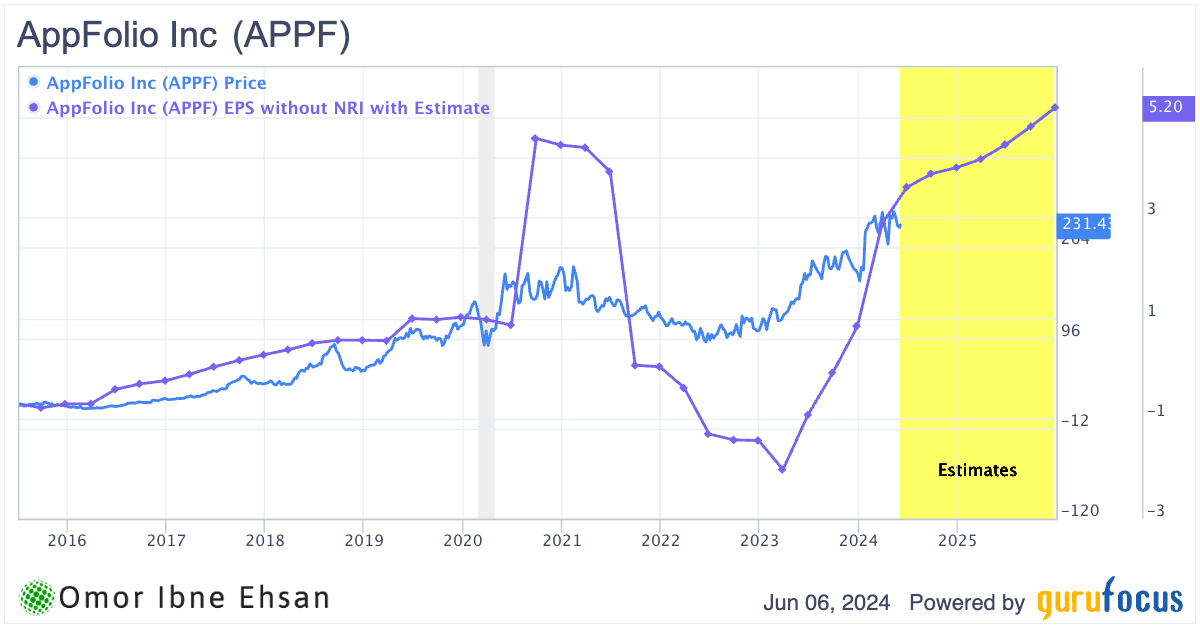

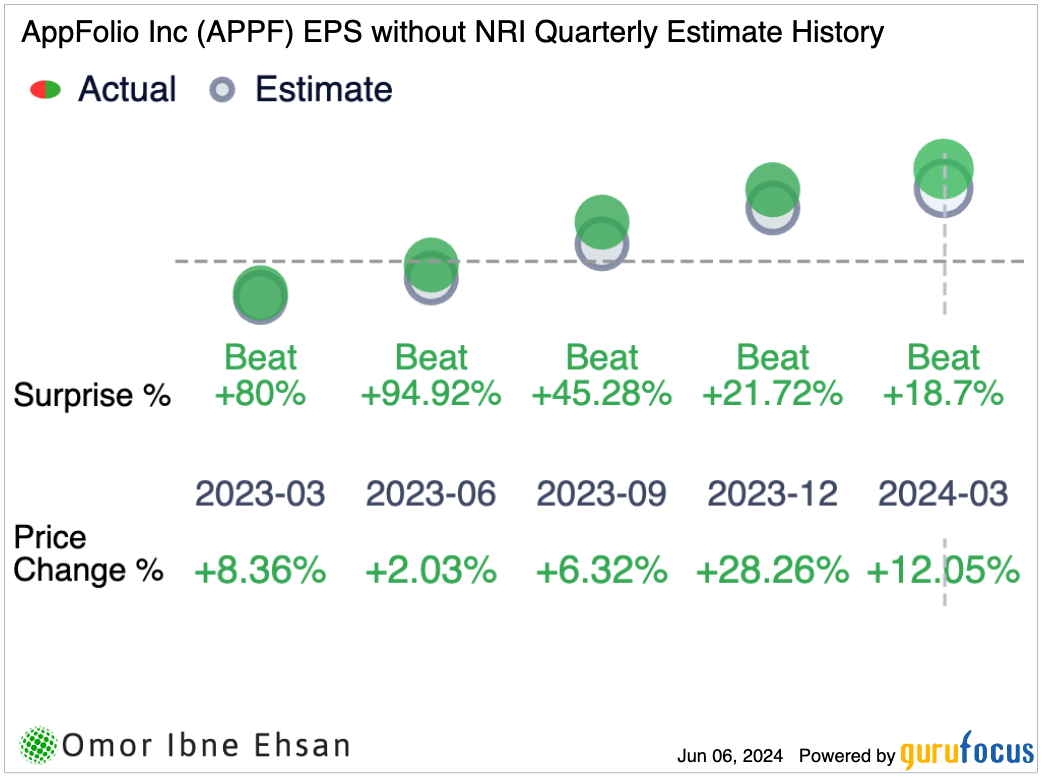

AppFolio (APPF)

AppFolio (NASDAQ:AAPF) provides cloud-based property management software solutions. Despite the waves of fear surrounding the real estate industry in recent years, I believe AppFolio is a great long-term investment with solid growth potential. In Q1 2024, AppFolio’s revenue surged 38% YOY to $187 million. The company also improved margins, with a non-GAAP operating margin of 26% and a free cash flow margin of 22%. Plus, rising EPS should lead to even more appreciation in the coming quarters.

Click to Enlarge

And don’t forget: AppFolio has been beating EPS estimates significantly.

Click to Enlarge

AppFolio’s differentiation lies in the company using AI to streamline processes like customer onboarding. This has resulted in customers completing data migrations 22% faster while maintaining a great experience. I believe the real estate industry is unlikely to face a massive crash due to limited housing supply and smaller family units. As interest rates eventually come down, demand for houses should accelerate. And I haven’t even talked about the additional demand from legal and illegal migration. Real estate will keep growing in the long run, and so will AppFolio. Definitely one of the growth stocks that could perform well through 2030.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.