The stock market is soaring and investors are giddy about potential interest rate cuts from the Federal Reserve. But I’m not popping the champagne just yet. History shows that interest rate cuts have often preceeded recessions.

Sure, the labor market looks strong, and trends like re-industrialization bode well for the economy. However, if GDP underperforms as it did in Q1, there’s always the possibility we could tip into a recession. European investors are already skeptical that this rally will last.

I’m not saying a crash is imminent, but it pays to prepare for the worst while hoping for the best. Some stocks hold up well in a recession, while others are more likely to get hammered. I’ll highlight two stocks I believe are well-positioned to weather a downturn and two that could be in for a rough ride if the economy sours. Let’s dive in.

Stocks to Buy When the Market Crashes: ThredUp (TDUP)

ThredUp (NASDAQ:TDUP) is an online resale platform for apparel, shoes, and accessories. Indeed, this is a company that has been weathering a challenging economic environment. The stock has been trading sideways for a long time, but I believe a recovery could be on the horizon if consumers increasingly turn to secondhand goods in the face of financial pressures. ThredUp reported first-quarter revenue of $79.6 million, up 5% year-over-year, and gross margins expanded to 69.5%. The company is rapidly narrowing its losses, with adjusted EBITDA loss shrinking to just $0.7 million.

Resale is a major consumer trend, expected to more than double its market share and reach $350 billion globally by 2028. ThredUp’s peer RealReal (NASDAQ:REAL) has led to a significant recovery in TDUP stock. If ThredUp can surprise to the upside on top-line growth, the stock should follow suit. With active buyers reaching 1.7 million and orders growing 9%, ThredUp looks well positioned to capitalize on the secular shift toward secondhand goods. The company’s investments in AI and expanding its Resale-as-a-Service program with major retailers could further fuel growth in the quarters ahead.

McDonalds (MCD)

McDonald’s (NYSE:MCD) operates and franchises restaurants worldwide under the McDonald’s brand. The fast-food giant recently launched a new $5 meal deal amidst a growing price war in the industry. I believe this affordable combo will prove very popular with budget-conscious consumers.

That said, McDonald’s stock has taken a beating lately. It is down over 13% year-to-date as of July. This pullback seems overdone to me, as McDonald’s hasn’t historically performed this poorly outside of major recessions. I think the company’s current valuation provides downside protection going forward.

Importantly, McDonald’s has proven it can thrive during economic downturns. The company delivered impressive sales growth and restaurant expansion during the 2008 recession as cash-strapped consumers traded down to cheaper dining options. With its unmatched scale, modernized restaurants, and everyday value focus, I expect McDonald’s to once again outperform if a recession unfolds.

Stocks to Avoid When the Market Crashes: Coinbase (COIN)

Coinbase (NASDAQ:COIN) is the leading U.S. cryptocurrency exchange. Notably, COIN stock has skyrocketed 181% over the past year as Bitcoin (BTC-USD) hit new highs, spurring a market recovery. That said, I believe now is not the time to join the Coinbase bandwagon. The crypto market is notoriously cyclical, and Coinbase may be peaking. Most altcoins have already been crushed, with Bitcoin being the only crypto somewhat holding up. Even without a recession, I think Coinbase could take a beating in the coming months.

Coinbase reported blowout Q1 revenue of $1.64 billion, beating expectations of $1.34 billion. Net income was $1.18 billion, or $4.40 per share, compared to a year-ago loss. However, trading volumes on Coinbase’s platform have decreased significantly since early March.

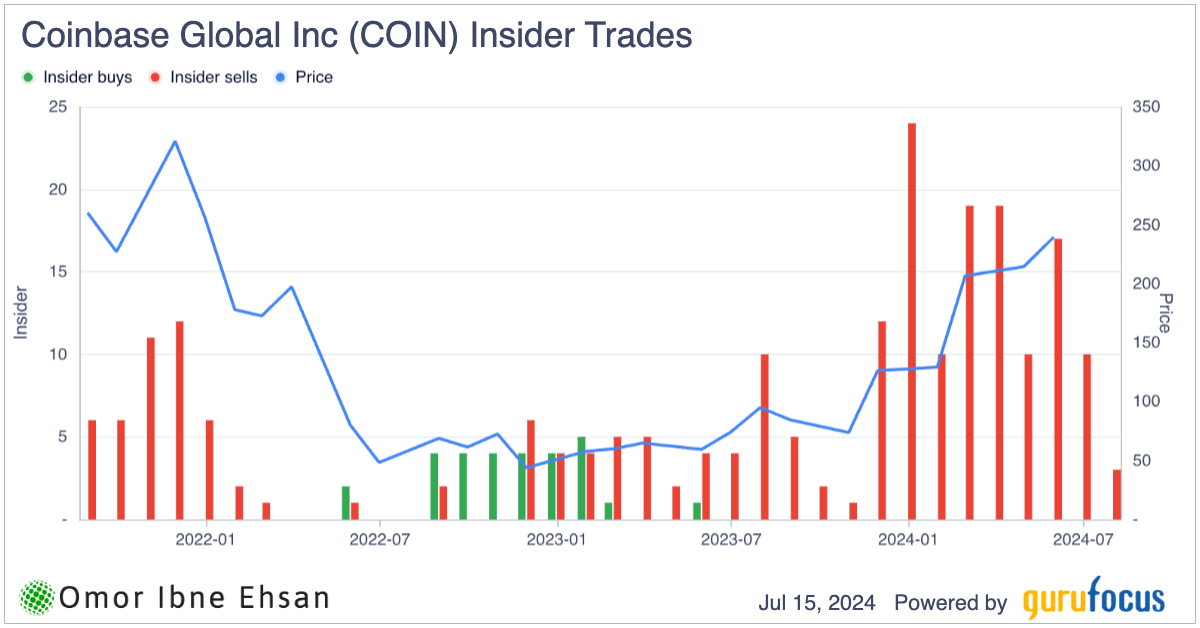

Moreover, Coinbase insiders sold a collective $383 million worth of shares in Q1. That’s more than double the amount sold in Q4 2023. Co-founder Fred Ehrsam alone netted $129 million from his share sales alone.

Click to Enlarge

Coinbase also faces ongoing legal challenges from the SEC. A judge ruled in March that the SEC’s claim that Coinbase engaged in unregistered securities sales will proceed to trial. New competition from Crypto.com is regaining market share as well.

With all that in mind, I’d steer clear of this crypto stock for now.

Robinhood Markets (HOOD)

Robinhood (NASDAQ:HOOD) operates an online brokerage platform that aims to democratize investing for the masses. I believe the company’s recent explosive growth is largely relying on the frenzied stock market rally that has surpassed even the euphoria of 2021 in some respects, along with the ballooning crypto market. While Robinhood reported record revenues of $618 million in Q1 2024, up 40% year-over-year, and turned a profit with net income of $157 million, I’m skeptical about the sustainability of this performance moving forward.

The company still faces significant headwinds and flaws in its business model. Robinhood’s tendency to gamify trading encourages novice investors to trade riskily frequently. The company also relies heavily on payment for order flow for revenue, a controversial practice that may result in customers getting worse execution prices.

Moreover, Robinhood is currently under investigation by the SEC, having received a Wells notice regarding its crypto business. Regulatory risks remain high. Additionally, I think Robinhood is far too exposed to the whims of the stock and crypto markets. Thus, if a recession drags down the market, Robinhood could be one of the worst hit companies out there.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.