Predicting the future is a fool’s errand. If you had asked me just five years ago what 2024 would look like, I would have gotten it laughably wrong. The world has changed at a dizzying pace over the last two decades, with the rise of smartphones, social media, artificial intelligence, and so much more. Paradigm-shifting events like the COVID-19 pandemic have humbled our collective prognosticating abilities.

So, looking out 50 years to 2074 seems downright quixotic. Will we have flying cars and robot butlers as 1950s futurists imagined? Probably not. But I believe we can still make some informed, if speculative, bets on which industries and companies could deliver hypergrowth if things break their way. Artificial intelligence, genomic medicine, and clean energy look poised to revolutionize the economy and our lives in the coming decades.

Of course, any 50-year prediction will likely prove off the mark. But, I’m willing to take some risks on high-upside growth stories. Because if the stars do align, the rewards could be astronomical. With that in mind, here are seven hypergrowth stocks to buy and hold until 2074:

Joby Aviation (JOBY)

Joby Aviation (NYSE:JOBY) is well-positioned to ride the megatrend of urban air mobility in the coming decades.

It recently completed a 523-mile flight with its hydrogen-electric aircraft. The company also continues to make steady progress on the regulatory front, becoming the first eVTOL maker to have its final airworthiness criteria published by the FAA.

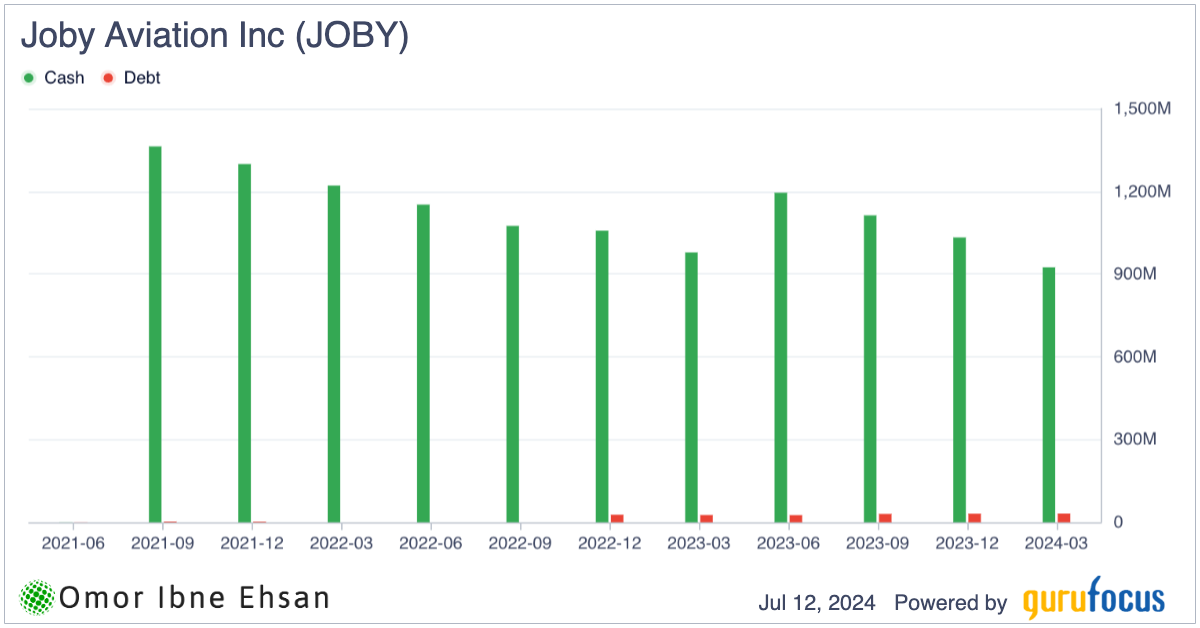

Financially, Joby remains on solid footing with $924 million in cash and short-term investments as of Q1 2024. This cash should provide ample runway as the company ramps up manufacturing and prepares for commercial operations targeted for 2025.

Click to Enlarge

Analysts are generally bullish on JOBY stock. The consensus rating is a “moderate buy” with a 12-month average price target of $9, implying nearly 45% upside from current levels. Raymond James recently initiated coverage with an “outperform” rating, while Canaccord Genuity reiterated its “buy” rating.

Sure, Joby is still in the pre-revenue stage and faces risks as it navigates uncharted skies. However, with strong partnerships like Toyota (NYSE:TM), Delta (NYSE:DAL), and the U.S. Air Force, I believe Joby has the right ingredients for long-term success. As the $1 trillion urban air mobility market takes flight in the coming years, Joby looks poised to be a prime beneficiary.

Credo Technology (CRDO)

Credo Technology (NASDAQ:CRDO) is riding high on the AI and data center megatrends. I believe the company’s focus on high-speed connectivity solutions positions it well to capitalize on the explosive growth in data and AI infrastructure.

In Q4 2024, Credo’s revenue surged an impressive 89.4% year-over-year to $60.8 million, driven by strong demand from hyperscale customers deploying AI. Analysts are bullish, with a consensus “Strong Buy” rating and an average price target of $29, although insiders have been selling shares recently. Credo’s management expects AI-related revenue to double by the end of fiscal 2025.

With gross margins over 65% and a cash-rich balance sheet, I think Credo has the financial strength to keep investing in innovation. As long as the data boom persists, I believe Credo’s growth story has legs. The stock has been volatile but rewarded investors with a 5% return over the past month. Of course, competition from giants like Nvidia (NASDAQ:NVDA) is a risk to watch. I’m optimistic about Credo’s prospects if the coming decades are driven by data.

Atlassian (TEAM)

Atlassian (NASDAQ:TEAM) is a leading provider of team collaboration and productivity software. I believe the company is well-positioned to benefit from several megatrends that should act as tailwinds for growth in the coming years. The rise of AI is a key one – Atlassian is already using AI to boost team productivity through features like predictive smart search and AI-powered writing assistance. The ongoing migration to the cloud is another massive opportunity, with Atlassian now a “cloud-majority” company with over 300,000 cloud customers.

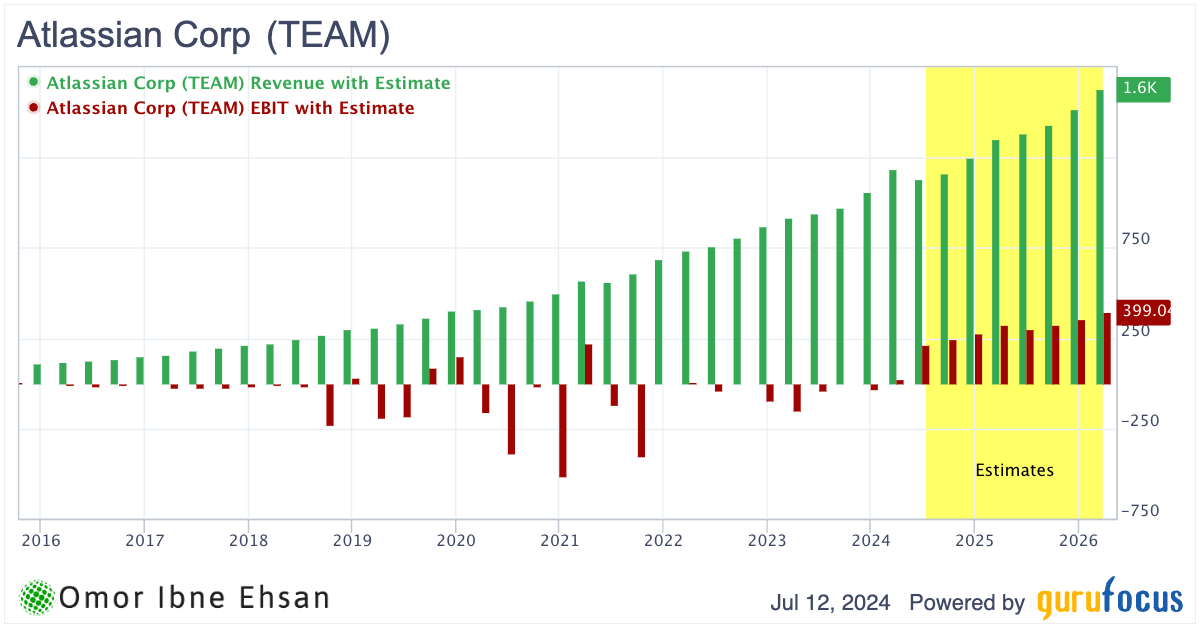

Enterprise service management is yet another area in which Atlassian has strong momentum. Its Jira Service Management product hit $600 million in annual revenue as large organizations increasingly standardize on Atlassian. Financially, the most recent quarter impressed, with $1.19 billion in revenue (up 30% YOY), 82% gross margins, and positive operating income. Atlassian also provided bullish medium-term guidance, targeting 20%+ revenue CAGR through FY27 while maintaining operating margins above 25%. The growth ahead is too good to ignore.

Click to Enlarge

The stock has pulled back significantly from its highs and is basically flat in the past year, but I suspect it may have bottomed out here. I see significant upside if the growth continues.

DroneShield (DRSHF)

DroneShield (OTCMKTS:DRSHF) provides drone detection and countermeasure solutions to militaries and other security-focused organizations worldwide. I believe the company is poised for significant growth as the proliferation of drones in warfare and other domains is driving exponential demand for effective counter-drone technologies.

DroneShield’s financial performance has been nothing short of impressive. In Q1 FY2024, the company reported a staggering 900% year-over-year increase in revenues, reaching 16.4 million AUD. This growth was fueled by major contract wins, including a 5.7 million AUD repeat order from a U.S. government customer and a landmark counter-drone procurement agreement with NATO.

Analysts are bullish on DroneShield’s prospects. Bell Potter rates the stock a buy with a forecast of 97 million AUD in sales and 24.4 million AUD in earnings for FY2024. CEO Oleg Vornik’s recent comments suggest even greater ambitions, hinting at the potential for annual revenues to reach 500 million AUD.

I believe DroneShield is well-positioned to capitalize on these megatrends and deliver substantial returns for investors. While the stock has already seen impressive gains (up 767.65% in the past year), I think there’s still plenty of room for growth.

Samsara (IOT)

Samsara (NYSE:IOT) provides software and insights for physical operations through its Connected Operations Cloud. The company is riding several megatrends that I believe position it well for continued hypergrowth. First, the increasing digitization of physical operations across industries like transportation and manufacturing is driving strong demand for Samsara’s platform. Second, the transition to electric vehicles (EVs) could accelerate in the coming years as interest rates come down.

Samsara delivered 37% revenue growth to $281 million in Q1 while also achieving record gross margins of 77%. Large enterprise customers grew 43% as Samsara became a strategic partner for digitizing complex operations. Analysts remain bullish, with RBC Capital reiterating an Outperform rating and $47 price target. The stock has surged 23% in the past month alone.

While Samsara’s platform extends well beyond EVs, I’m optimistic the company will benefit as high-growth tech stocks roar back. With a massive $20 billion market cap already, Samsara still has a long runway ahead in my view. The company’s ability to deliver fast ROI and billions in customer savings makes it a compelling investment for the years and even decades to come. Of course, competition is fierce, and execution is key, but I believe the stars are aligning for Samsara.

Cloudflare (NET)

Cloudflare (NYSE:NET) is a leading content delivery network and cloud security company that helps power and protect a huge portion of the internet. I’d bet that most of the websites I visit on a daily basis rely on Cloudflare’s services in some way, even if it’s not obvious. This company has quietly become the backbone of the modern web.

In Q1 2024, Cloudflare posted strong results, with revenue growing 30% year-over-year to $378.6 million. Large customer growth was particularly impressive, as Cloudflare added a record number of customers spending over $100,000, $500,000, and $1 million annually. Operating margins also expanded.

Cloudflare is riding several powerful tailwinds that should continue propelling its growth. The ongoing shift to the cloud, the rise of edge computing, and the ever-increasing importance of cybersecurity are all megatrends playing right into Cloudflare’s strengths. As more companies digitize their operations and more data moves online, the demand for Cloudflare’s web performance and security solutions will only increase.

CEO Matthew Prince recently unloaded over $12.9 million worth of stock. However, this is likely for personal financial reasons and doesn’t change the company’s fundamental story. With Cloudflare powering 80.6% of websites in some form, its market dominance is unquestionable. As long as the internet keeps growing, Cloudflare should keep winning.

Semrush Holdings (SEMR)

Semrush Holdings (NYSE:SEMR) provides an online visibility management SaaS platform used by marketers for SEO, PPC, content, social media, and competitive research. I believe Semrush is well-positioned to capitalize on the rapid growth of the digital marketing software market, which is expected to reach $264 billion by 2030. As businesses increasingly rely on search engine traffic to drive revenue, tools like Semrush that optimize online visibility are becoming mission-critical.

Semrush delivered impressive results in Q1 2024, with revenue up 21% year-over-year to $85.8 million. The company is firing on all cylinders – paying customers increased to nearly 112,000, while its free active user base surpassed 1 million for the first time. Importantly, Semrush achieved strong profitability, reporting income from operations of $1.5 million and generating a free cash flow of $12 million.

Looking ahead, I’m very bullish on Semrush’s growth prospects. The company is making smart investments in AI-powered tools like Content Shake and expanding upmarket with its new enterprise SEO product. This should drive further ARPU expansion, as enterprise contracts carry 10-15x higher values than Semrush’s current average. With secular tailwinds at its back and a large market opportunity ahead, analysts are overwhelmingly positive on the stock, with a consensus price target of $15.90 implying nearly 18% upside.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.