When a stock has become a big-time winner, many investors bet against it simply because it’s rallied so much. Stocks do get exhausted, but that’s a poor thesis to bet on a stock’s demise — particularly when it comes to a name like Salesforce.com, inc. (NYSE:CRM). Salesforce stock has been a beast this year, up 23%. Can it continue?

While the PowerShares QQQ Trust, Series 1 (ETF) (NASDAQ:QQQ) is up a very respectable 8%, CRM is crushing that performance. However, given the trends in its business and its long-term growth profile, I see little reason to let go of a long position now.

Salesforce Growth and Valuation

Admittedly, CRM stock is not cheap. But let’s put it this way: No one bought Salesforce, watched it rally and has now decided it’s become too expensive to own. CRM stock has always been expensive, not unlike Amazon.com, Inc. (NASDAQ:AMZN).

Also like Amazon, Salesforce has continued to meet the lofty growth goals expected of the company. CEO Marc Benioff still expects Salesforce to hit $20 billion in sales by 2022. Keep in mind that for this year, consensus expectations “only” call for $12.7 billion in sales.

To get to $20 billion by 2022, CRM will need to grow sales by more than 20% annually over the next few years. Consensus expectations call for $18.5 billion in sales in 2021, roughly $1.5 billion short of management’s goal. Worth noting is that consensus expectations have CRM generating almost $22 billion in sales in fiscal 2022.

In February, Salesforce beat on earnings and revenue expectations and raised its full-year outlook. From Benioff: “It was our best quarter we’ve had in a long time. It’s an amazing quarter … I think that because of this incredible quarter, you’re going to see us really have a huge dream of getting to $20 billion faster than any other software company ever.”

I don’t expect that momentum to be a one-quarter phenomenon. On the earnings front, estimates call for 67% growth this year to $2.26 per share, followed by 20% growth next year. In other words, CRM trades at about 55 times earnings.

I told you it wasn’t cheap.

For better or for worse, CRM isn’t about earnings growth — at least not yet. Again like Amazon, CRM is still in “go, go, go!” mode. While it’s growing bottom-line results and cash flow, it’s more focused on fueling the top line at the moment.

The Cloud

The cloud has never been a slow-growth industry. But for a while, it looked like the industry was becoming commoditized and growth was slipping. In the second half of 2017 though, that mindset changed. We saw the industry become re-energized and begin to churn out even stronger growth.

It now feels like the cloud is in the early innings rather than the mid to late innings. That’s based on the results from Amazon, Microsoft Corporation (NASDAQ:

MSFT) and Alphabet Inc (NASDAQ:GOOG, NASDAQ:GOOGL). It’s also based on how well smaller companies like Twilio Inc (NYSE:TWLO) and Box Inc (NYSE:BOX) are doing.

Even as terms like artificial intelligence and machine learning make their way to the water coolers and family outings, the cloud industry still has plenty of growth to go. Those that integrate AI/machine learning into the cloud have even more runway. That’s why I think CRM stock still has a long ways to go before slowing down.

Trading Salesforce Stock

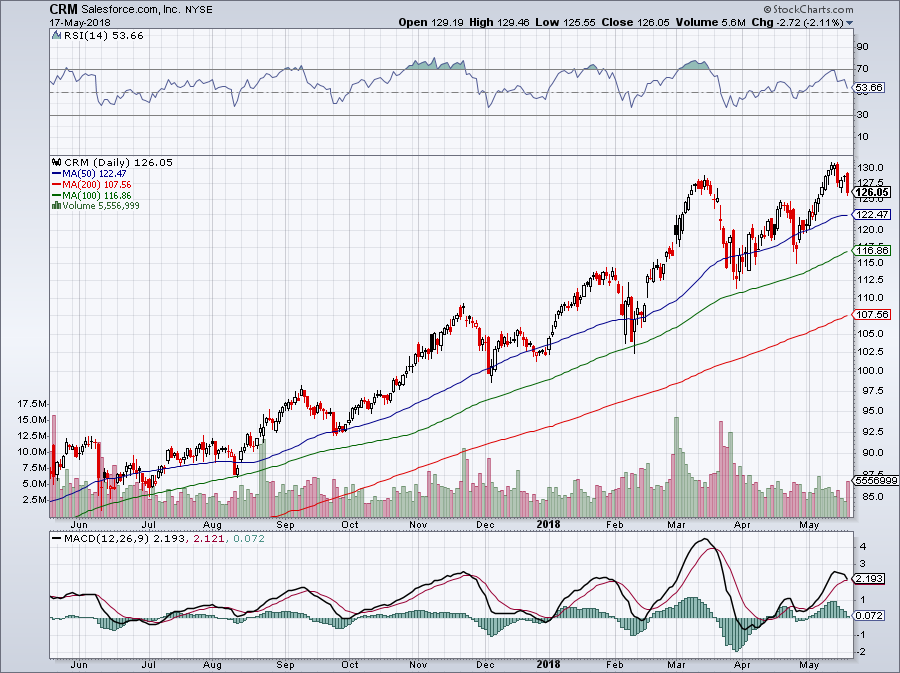

Click to Enlarge

Not many marks have to be drawn on the chart for Salesforce stock.

Over the past year, the trend has been pretty clear as CRM stock moves from the lower left to the upper right. If I were looking to buy a new position, starting one near $120 wouldn’t be the worst idea. For reference, the 100-day moving average has been a great buying opportunity over the last 12 months.

As for upside, the average analyst price target sits near $138, implying about 10% upside from current levels. There are plenty of estimates over $140 though and even one all the way up at $160. Should it get there, that’s 27% upside from current levels.

It would be great if it did, but I don’t know that Salesforce stock can eclipse $160 this year. To be clear, I think $160 is definitely in the cards. I just don’t know that it will be in the next 6.5 months. However, if CRM stock can close the year above $140, investors should be happy. Let’s see what management says when it reports earnings on May 29.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell was long CRM and BOX.