On Thursday, June 26, Nike (NYSE:NKE) reported its fiscal fourth-quarter earnings. As a result of its top- and bottom-line miss, shares are under pressure in after-hours trading. If there is more selling pressure, this could be a buying opportunity for Nike stock.

Why buy if the quarter was uninspiring? Simple. Because Nike is a very powerful brand with a loyal customer base. It’s one of the very few apparel and retail brands that will continue to do well — with or without the novel coronavirus — and will not see its business fall off the face of the earth.

Let’s look at the quarter before we go any further.

A Surprise Loss

Nike generated a loss of 51 cents per share in the quarter. That was a surprise loss to Wall Street, with consensus expectations calling for 3 cents per share in profit. That’s as revenue fell 38% year-over-year to $6.31 billion, missing estimates by $950 million.

Think about those headline numbers for a minute.

Within the apparel group, Nike stock is among one of the best-positioned names in the space. Earlier this month we heard from Lululemon (NASDAQ:LULU), which also has a loyal customer base. The company also missed on earnings and revenue estimates as the coronavirus weighs heavily on sales.

Both companies leaned on e-commerce to pick up the slack, but still, this was a difficult quarter. Now what are the rest of the companies in this space looking like — the lower quality companies? I’m afraid to ask.

In fiscal Q4, gross margins came in at 37.3%, well short of expectations at 43.3%. It’s as if years of careful, meticulous work has been undone in one quarter.

On the plus side, online sales soared 75% for Nike, as customers turned their attention to digital sales. That figure climbs to 79% on a currency-neutral basis and represented about 30% of total revenue.

From CEO John Donahoe: “In a highly dynamic environment, the NIKE Brand continues to resonate strongly with consumers

all over the world as our digital business accelerates in every market …We are continuing to invest in our biggest opportunities, including a more connected digital marketplace, to extend our leadership and fuel long-term growth.”

Then from CFO Matt Friend, “As physical retail re-opens, NIKE’s strong digital trends continue, a testament to the strength of our brand and the investments we’ve made to elevate digital consumer experiences.”

Valuing Nike Stock

I ended that last section with two quotes, because they are far more important than one or two quarter’s worth of numbers. I don’t mean to say that earnings are not important. But clearly we know this is a highly disrupted period due to Covid-19, and amid short-term chaos, investors need to focus on the long-term opportunities.

Clearly, those opportunities are presenting themselves in the digital space. Both the CEO and CFO mentioned such, and while I agree with that assessment, it’s not just because it’s what management said. It’s what we see from Shopify (NASDAQ:SHOP), Amazon (NASDAQ:AMZN) and virtually every other e-commerce platform.

Of course, it helps that sales are rebounding at store locations, too. Nike had this to say in the press release: “Retail traffic continues to improve week-over-week with higher conversion rates as compared to the prior year.”

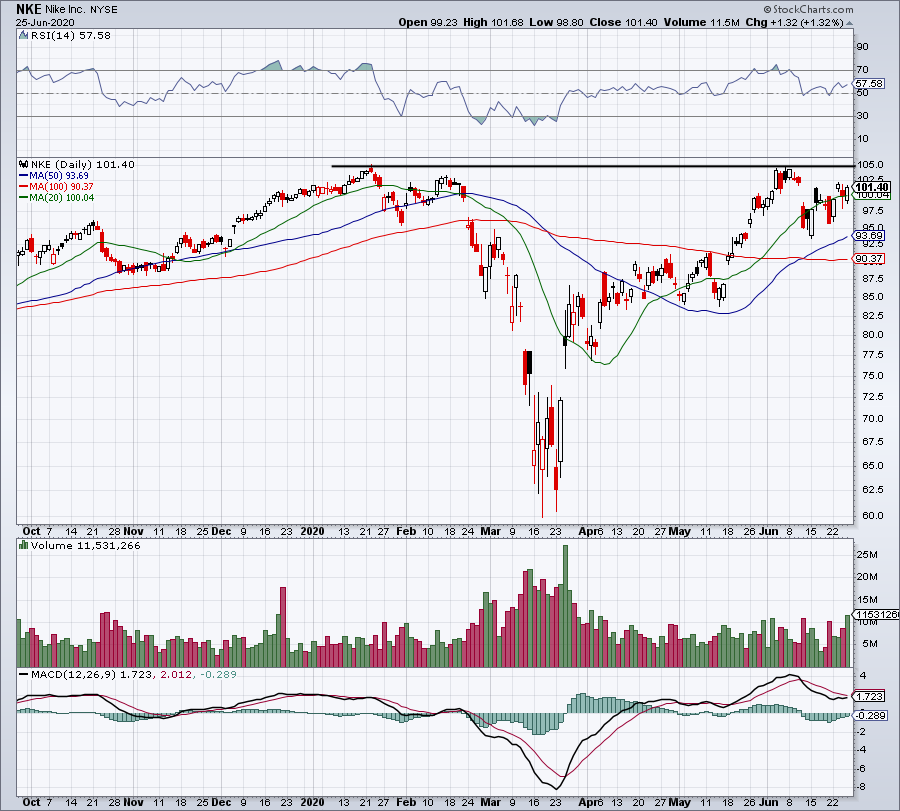

That bodes well for fiscal Q1 and potentially all of fiscal 2021. However, we have to understand that business is taking a hit and that maybe, just maybe, Nike stock doesn’t deserve to be trading 3.5% below its all-time high, as it was at the close of trading before earnings.

For fiscal 2021, analysts expect overall revenues to rebound by 7.7%, although that figure is sure to change after Q4 2020 sales missed estimates by nearly $1 billion. A surprise loss will also alter earnings expectations, which called for a 21% rebound in this fiscal year (before Q4 earnings were out).

The Bottom Line on Nike

Click to Enlarge

Covid-19 makes this environment difficult for two reasons. First, how can we justify Nike stock trading just below pre-coronavirus levels when the company is getting hammered right now?

That’s a tough case to make, even as much as I like Nike’s long-term potential.

Second, with so much uncertainty — rising unemployment numbers, a second wave, etc. — how can investors be too confident in Nike’s business recovering so quickly?

I love Nike, but let’s see if we can’t get a better price for this company. The long-term opportunities are obvious, but so are the short-term headwinds. Let’s start with a potential dip into the low-$90s, where Nike stock finds its 50-day and 200-day moving averages.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.