Can Merck (NYSE:MRK) rally almost 30% to $105? If you ask the folks at Goldman Sachs, they’ll say it’s possible. The firm recently upgraded the stock to a buy rating and assigned MRK stock with a — you guessed it — $105 price target.

Among other things, the analysts are bullish on Merck’s pipeline and balance sheet. The upgrade comes after the company reported earnings on July 31.

In that report, Merck reported earnings of $1.37 per share, easily beating estimates by 32 cents. Revenue of $10.87 billion coasted past estimates by $350 million, despite sales slipping more than 10% year-over-year.

More importantly, the company provided better-than-expected full-year guidance. Management now expects sales in the range of $47.2 to $48.7 billion vs. a prior outlook of $46.1 to $48.1 billion. Consensus estimates were at the low end of the new range, at $47.33 billion.

On the earnings front, management now expects profit of $5.63 to $5.78 per share, up from a prior range of $5.17 to $5.37 per share. Analysts were looking for $5.31 per share, which was below the low end of the new range.

All of That’s Great, But…

Hey, we’re not here to hate on a good quarter. Merck turned in a good result — a top- and bottom-line beat — and raised guidance. MRK stock pays out a dividend yield close to 3%, which is slightly more than the S&P 500 and well above the 10-year Treasury yield of 0.53%.

Based on the midpoint of the company’s most recent outlook, Merck’s stock isn’t even that expensive. Shares trade at just 14.5 times the midpoint of this year’s estimate. So what’s the problem?

To an extent, there isn’t one. But we can’t own every stock out there. Given Merck’s market capitalization of $200 billion and its somewhat sluggish growth, I would simply prefer to look elsewhere.

Consensus expectations call for just 1.8% revenue growth this year and for 8% growth in 2021. Earnings estimates are a bit better, with expectations calling for 6% and 13.8% growth this year and next, respectively.

But when I’m looking for biotech stocks, I want explosive growth and robust pipelines. While Goldman Sachs likes the pipeline here, I want more. The growth needs to be better and if Merck were to make an acquisition or two that really built on that upside potential, then it would certainly be worth another look.

As it stands, this is a great quality company, but it’s one without a whole lot of growth. In other words, it’s a mature biotech stock, not unlike an Oracle (NYSE:ORCL) in the tech world. I’m sorry, but I would rather own a faster horse.

Some could consider that horse to be Regeneron (NASDAQ:REGN). Despite its flat growth and $72 billion market cap, 2021 should be a stronger year. Or even a name like Invitae (NYSE:NVTA), although that’s a bit more speculative.

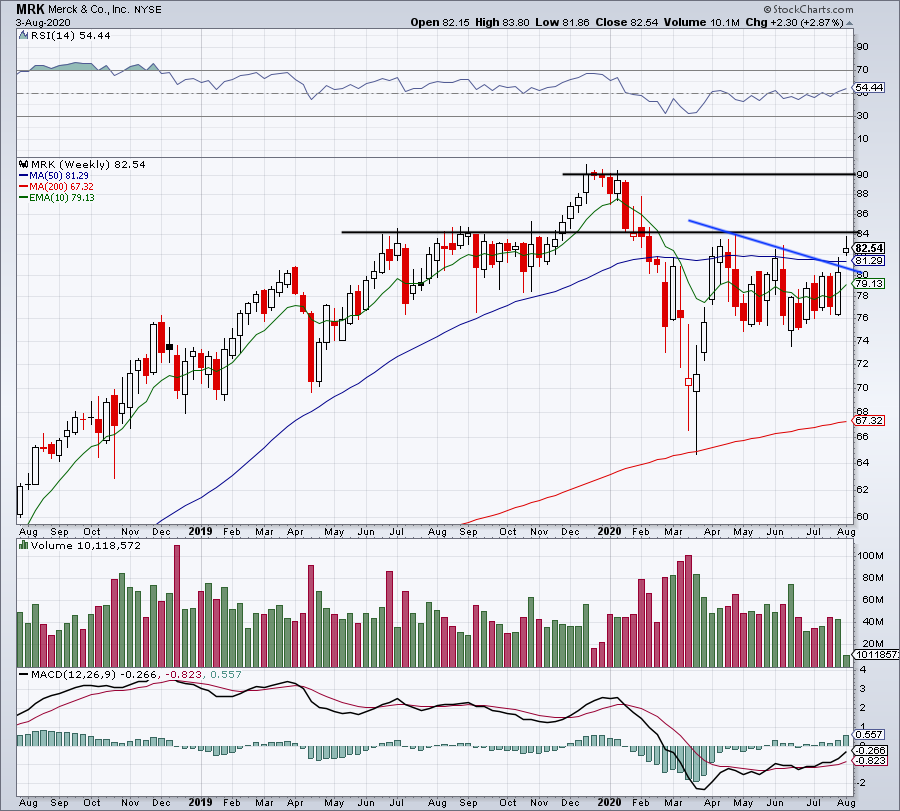

Sizing Up MRK Stock

Click to Enlarge

After reporting earnings last week, MRK stock tested up into the 50-week moving average and downtrend resistance (blue line). However, the stock was rejected from both levels, ultimately closing the week near $80.

Merck didn’t waste any time on Monday, gapping up over both of these marks. It’s good to see shares on the right side of the 50-week moving average, which has been notable support and resistance over the years. For bulls to really remain in control, this mark needs to act as support going forward.

On the upside, we need to see MRK stock clear $84, a notable level of resistance from 2019. Above $84 puts $90 in play, which was resistance in Q4 2019 and in the first few weeks of 2020. Over that and the calls for $100 will grow louder.

Like I said, I’m not bearish on Merck or biotech in general. There are simply other stocks that I’d prefer to be in.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now. As of this writing, Matt did not hold a position in any of the aforementioned securities.