Editor’s Note: This article was updated on Sept. 22, 2020, to correct the wording around Intel’s P/E ratio.

Intel (NASDAQ:INTC) is well-known among the investment community. One of the largest chip makers out there, the name has been around for decades. But Intel stock isn’t what it used to be. Or should I say, doesn’t enjoy the same dominance it once did.

For that, the company can thank Advanced Micro Devices (NASDAQ:AMD) and Nvidia (NASDAQ:NVDA). Intel may have formed 52 years ago in 1968 and went public 49 years ago. Despite its long-time standing in the semiconductor industry, others have caught up.

Simply put, AMD is taking market share, while Nvidia goes gangbusters. Delays to products and stifled growth has left Intel as the odd one out. While it won’t be going out of business, it lacks the agility and innovation of its peers. It lacks the oomph behind the hottest tech stocks I identify with Investment Opportunities.

Intel Just Doesn’t Have What It Takes

Intel is forecast to grow revenue just 4.4% this year, while consensus estimates call for a 40 basis point decline in year-over-year earnings growth. Although there’s still time for a rebound, the numbers for 2021 are even worse. Analysts expect sales to slip just over 2% and for earnings to fall 3%.

Some investors will argue that Intel stock is cheap. While they are right, shares are cheap for a reason.

Intel stock trades at about 10 times earnings — much cheaper than Nvidia and AMD. However, these companies have explosive growth forecasts for this year and next year. Of course they have a higher valuation, because investors are willing to pay a premium for them.

In other words, Intel is a value trap. Unassuming investors look at a simple measure like the price-to-earnings ratio, see a below-market multiple and assume they are getting a good deal. In contrast, inexperienced investors may look at the P/E ratio for NVDA and AMD and conclude that they are far too high.

Admittedly both stocks have been on an eye-popping run. But the elevated valuations say one thing to me, which is that demand for the stock is through the roof — and it should be.

In its latest blow, Intel reported disappointing earnings in late July. Shares fell more than 16% in the first post-earnings trading session and more than 20% in the five sessions following earnings.

But it wasn’t just the quarterly report that stoked the selling. The company said its 7nm chips would be delayed until 2022. That opens the door for AMD, (which rocketed higher on the news). It was just one more misstep showing how Intel’s competitors are simply out-executing the industry stalwart.

Fortunately, for those looking to be far ahead of the curve with their tech-based investments, I’ve curated the best plays behind multiple technological revolutions. Investment Opportunities is one way to help you make huge profits while dodging deceptive duds like Intel.

Intel Stock Lacks Catalysts

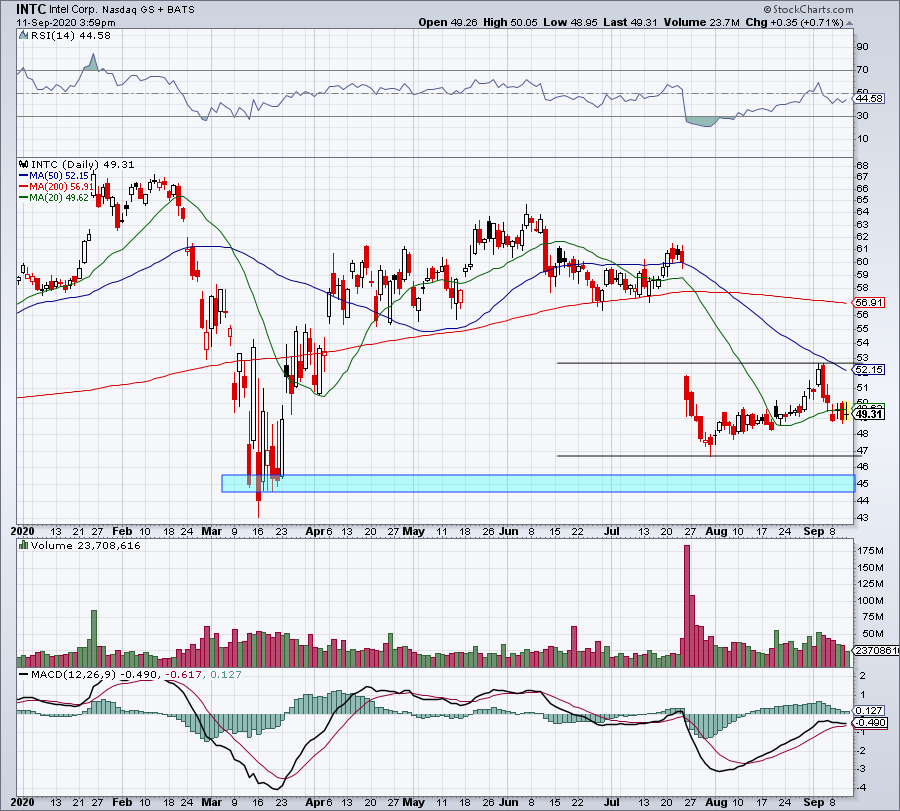

Click to Enlarge

A low valuation has its merits, but not at a time where tech stocks are doing so well. On the plus side, Intel stock pays out a 2.7% dividend yield, which is nothing to scoff at given that the 10-year Treasury yield stands at less than 70 basis points.

Still, we’re not snooping around the semiconductor space looking for yield and low valuations. Those merits have a place in one’s portfolio, but not when looking for stocks that should be enjoying the tailwinds of secular growth.

Beyond those marks though, there’s simply no urgency to buy Intel stock. There’s little to no growth when its competitors have robust growth. That’s all we really need to say. Cash flows are fine, the balance sheet is OK, but is that enough? Not really, no.

Current assets of $31.3 billion outweigh current liabilities of $22.3 billion. But long-term debt stands at $25.3 billion, while current debt rests at $3.7 billion. Intel isn’t facing a liquidity scare, but compare that to the bolt-on and accretive acquisitions that Nvidia has made and the pristine balance sheets of other mega-tech stocks and it leaves Intel investors wanting more.

On top of all that, the stock’s performance underscores the lack of demand for Intel stock. Shares are up just 14.5% from the March lows. That compares to the 108% rally in AMD and the 169% burst in Nvidia. It badly lags the Nasdaq too, which is still up 63.5% from its March low, despite the recent pullback.

Maybe it retests the August low near $46.60. Perhaps not. It doesn’t matter. I’m not interested in Intel because it doesn’t have the catalysts that its peers have. That makes it a stock to avoid.

Intel stock is no longer shinning, but not all tech plays are duds. Nvidia and AMD are strong players with notable catalysts. However, while these tech names hold promise, there’s another stock that you need on your radar. It’s bound for long-term success that’s perhaps even more impressive, only the space it focuses on is mobile communication.

While several tech titans helped lay the foundation for our hyper-connected society, this company stands to lead a technological revolution that will forever change communication on a global scale.

As InvestorPlace’s chief technology analyst, I’ve worked feverishly with our veteran research team to identify the best stocks to buy in my Investment Opportunities. Over the years, our research has helped millions get ahead of the curve. Our subscribers have enjoyed massive gains in tech titans long before they were kings.

Now, I’m ready to share with you the stock behind the next big development in communication. The company has already inked deals with key mobile phone partners. But it’s bound to become its own king with an approach to mobile interaction that we’ve never seen before … and it’s only a taste of the unique strategies and research you can expect from Investment Opportunities.

On the date of publication, Matt McCall did not have (either directly or indirectly) any positions in the securities mentioned in this article.

The InvestorPlace Research Staff member primarily responsible for this article had long position in NVDA.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now. As of this writing, Matt did not hold a position in any of the aforementioned securities.