Today, pharmacy stocks are stuck in the middle of a tug-of-war in the markets. Intricately linked to the broader healthcare industry, pharmacies have seen their equity valuations decline with benchmark exchange-traded funds like Health Care SPDR (ETF) (XLV).

On the other hand, pharmacies are considered staples. They’ve benefited from consistent, secular demand that industries with specialized services usually don’t have.

However, there are signs that pharmacies can no longer afford to hide under the radar.

In the middle of last month, retail giant Wal-Mart Stores, Inc. (WMT) announced a partnership with McKesson Corp. (MCK), the largest distributor of pharmaceuticals in the U.S. The deal — which involves leveraging the size of both companies to reduce drug costs — is a win for both companies. For McKesson, the new contract replaces ones that recently expired. For Walmart, this adds another weapon in its battle against declining traffic.

From an outside perspective, the deal speaks more of necessity than a shrewd business strategy. More and more pharmacies, along with other entities involved in the distribution of medication, are either working out their own arrangements or are simply merging together. This may result in lower consumer prices, but it also underscores just how tight the competition among pharmacies has become.

Here are three pharmacy stocks that have weakened under a tough industry.

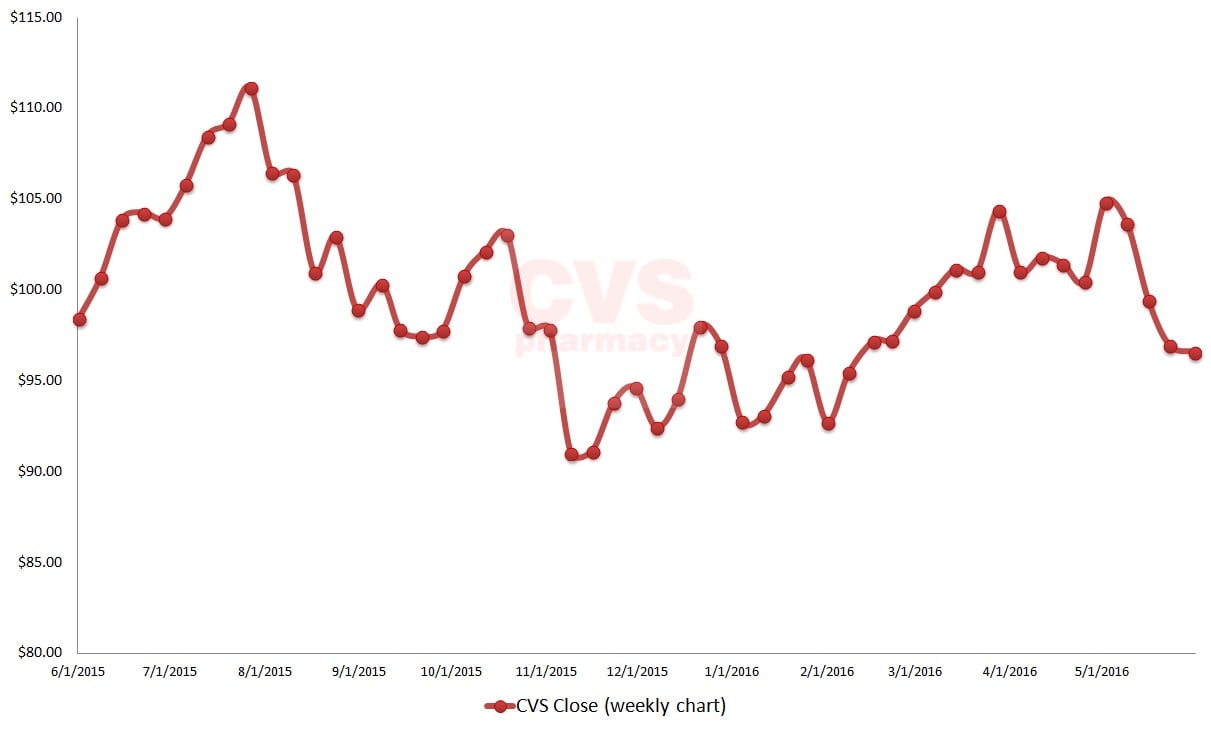

Pharmacies That Look Sickly: CVS Health Corp. (CVS)

Currently the biggest name by market capitalization among the featured pharmacies, CVS Health Corp. (CVS) took a big risk on its self-imposed cigarette sales ban.

More than two years ago, the pharmacy giant announced its decision, citing overall health concerns. Though the move was praised by anti-smoking activists, Wall Street was rightfully concerned regarding the impact towards CVS stock. However, top-line sales continued to grow, in part due to a cultural shift against “Big Tobacco” companies.

Unfortunately, no good deed goes unpunished, which aptly describes CVS stock.

Although the company scored an earnings beat in the first quarter of fiscal year 2016, the growth rate was the smallest since Q4 FY2013. This also placed a caveat on a 19% increase in revenue, which was primarily driven by asset acquisitions. CVS bought out Omnicare last year, and it also procured pharmacies that were under the Target Corp. (TGT) brand.

The expansion efforts are great, but they also came at a steep price.

Click to Enlarge

Add to this the fact that since the company no longer benefits from cigarette sales — a very tangible source of income — and there’s reason to fear that CVS stock is stretched.

CVS stock isn’t going to collapse. At the same time, it’s evident that there are enough worries that are keeping investors on the sidelines.

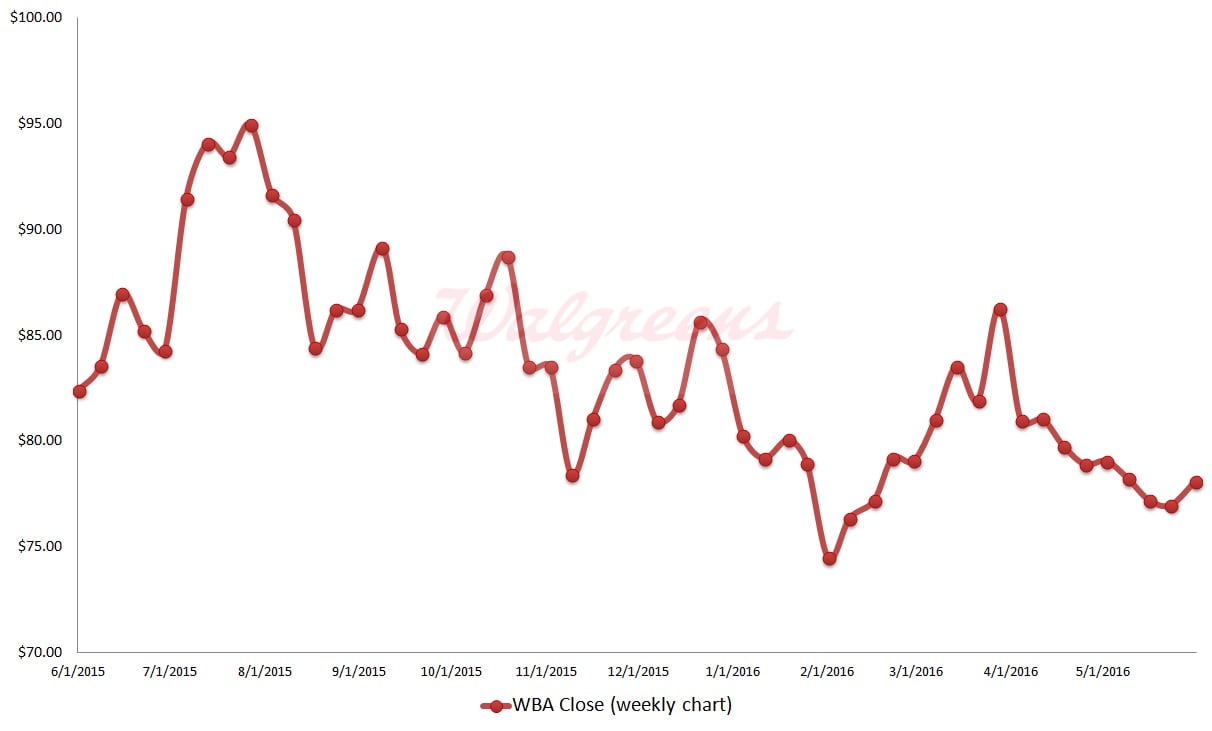

Pharmacies That Look Sickly: Walgreens Boots Alliance, Inc. (WBA)

A few days before Halloween last year, Walgreens Boots Alliance, Inc. (WBA) announced that it would buy out rival competitor Rite Aid Corp. (RAD).

At the agreed-upon price of $9 per share, the buyout amounted to a 48% premium against RAD stock’s closing price just prior to the announcement. Not surprisingly, shares of embattled Rite Aid soared.

Sadly, the same could not be said about WBA stock. After a brief spike up, Walgreens slipped into a bearish trend channel. Since the buyout disclosure, WBA stock is down 17%.

As if that wasn’t bad enough, there’s a little matter called Theranos. The blood testing startup company was a Wall Street darling and provided a constant stream of corporate, cheerleading articles — namely because of Theranos’ young, beautiful, billionaire CEO, Elizabeth Holmes.

The only problem? A mountain of accusations and an army of federal regulators suggest that the whole thing was fake.

Ironically, Theranos entered into a partnership with Walgreens’ because it was a respected brand among pharmacies. That now raises questions about the company’s quality control measures, as well as the health of WBA stock.

Click to Enlarge

Then there’s the second irony of sticking firmly with the buyout of Rite Aid — which some view as a financial liability — while keeping as much distance from Theranos, a reputational burden.

The ultimate impact to WBA stock is still unclear. However, investors typically don’t like drama, especially if it was preventable.

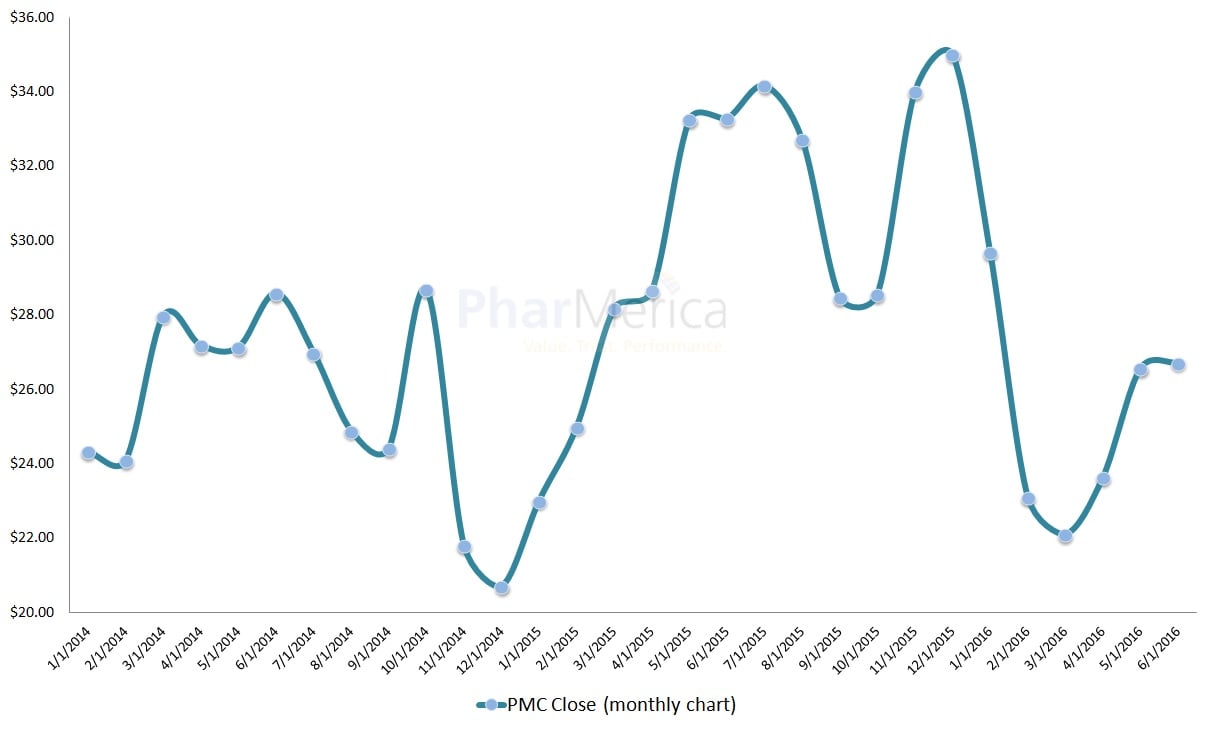

Pharmacies That Look Sickly: PharMerica Corporation (PMC)

Among publicly traded pharmacies, one could make the argument that PharMerica Corporation (PMC) has one of the strongest bullish arguments.

Unlike typical brick-and-mortar pharmacies, PMC stock is supported by a diverse business structure. This includes pharmacy services to healthcare institutions, outpatient services, and specialized oncology care.

Of these divisions, the vast majority of sales comes from the company’s institutional pharmacies. With several patented medications about to expire, PMC stock could see a boost in both revenue and earnings thanks to the possible sales increase of generic knockoffs.

However, there’s a big difference between theory and reality. While PMC stock has seen a sharp rise in market value over the past two months, we haven’t seen much stability. Year-to-date, PharMerica shares are down 24%, and it wouldn’t be that much of a stretch to say that investors are losing patience.

In the past six years, top-line sales have been shaky, ranging from steep declines to double-digit growth. And while PMC stock did beat earnings expectations in Q1, the result was more than 6% under the year-ago performance.

Click to Enlarge

We saw a similar pattern in PMC stock during the second half of 2014. This may embolden contrarian traders to time the reactionary spike move up. But the length of bearishness this time around makes such a move particularly risky. The weaknesses among other pharmacies casts further doubt.

Like its bigger rivals, PMC stock is a solid company facing troubling headwinds. However, there may still be some turbulence left in the journey.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.