It may be time to finally buy Alphabet Inc (NASDAQ:GOOGL, NASDAQ:GOOG). For those that have been absent on the GOOGL stock rally, it may be hard to jump in now. Particularly with shares trading north of $900. But this is such a high-quality company with a tremendous moat, it makes little sense not to own it.

If investors want to own GOOGL via a fund — like the Fidelity Nasdaq Comp. Index Trk Stk(ETF) (NASDAQ:ONEQ) or the PowerShares QQQ Trust, Series 1 (ETF) (NASDAQ:QQQ) — that’s fine, too.

While this type of ownership dilutes the benefits of owning GOOGL stock, it also helps protect investors from risk.

Getting to World Domination

For better or worse, Alphabet takes chances. It’s had some duds (Motorola, which it bought for $12 billion and sold for $3 billion), but it’s had some big winners, too.

The biggest win? Probably its purchase of YouTube for $1.65 billion in 2006. The property has become the second most popular website on the web — right behind Google. It gives Alphabet the No. 2 online properties, nudging out Facebook Inc (NASDAQ:FB) and Baidu Inc (ADR) (NASDAQ:BIDU).

This raises the question about whether Baidu — the “Chinese Google” — can nudge out any of these three properties. But if Facebook or Google were to suddenly gain Chinese approval, gold mines would suddenly open. Alas, I wouldn’t speculate on that happening any time soon, though.

Instead, despite the chaotic world of D.C., I would bet there’s a better chance we get a repatriation holiday. While it may not spark instant M&A, it should jump start some buying activity as many companies will now be flush with cash. Alphabet is no exception, having $94.7 billion in cash and short-term investments.

While it’s not as large as

Apple Inc. (NASDAQ:AAPL) and its $261 billion cash hoard, GOOGL’s dollars can still make an impact. I would look for the company to make acquisitions related to new businesses it’s already operating.

For instance, Waymo, it’s self-driving car business, has been valued at up to $70 billion by some analysts. Alphabet could surely put more resources behind this emerging new industry. GOOGL could also make acquisitions for businesses in the cloud and most certainly in artificial intelligence/machine learning. Alphabet has already shown it’s ready, snapping up DeepMind for an estimated $600 million to $650 million in 2014.

Several sub-$1 billion deals can help shape new businesses or improve existing ones as well.

Where Are We Going With All of This?

M&A means management is still focusing on growth and as a shareholder, that’s comforting. We want the company to continue growing. Acquisitions like Nest and Dropcam may be costing GOOGL money now, but so is Waymo.

But Waymo now commands a massive valuation. Who’s to say GOOGL stock won’t gain a premium valuation as perhaps Nest, Dropcam and other products start to form a “smart hub” around consumers’ homes? While that puts it in direct competition with Amazon.com, Inc. (NASDAQ:AMZN), Alphabet is no pushover.

That premium valuation may be closer than we think, though. Trading with a forward price-earnings ratio of 23.5, GOOGL stock isn’t necessarily cheap.

But with profit margins of almost 20% and estimates calling for 20% sales growth in 2017 and 17.2% growth in 2018, it may be worth it. Also consider that analysts are looking for almost 20% earnings growth annually for the next five years.

GOOGL stock is trading with a higher valuation than in years past, but there’s a good reason for it. Business is stronger than ever (and we recently took a deeper fundamental look).

CFO Ruth Porat, who’s been on board since May 2015, has tightened spending without suffocating growth. She’s also given the Street more transparency and, in that, investors have given trust. Believe it or not, that equals a higher valuation, too.

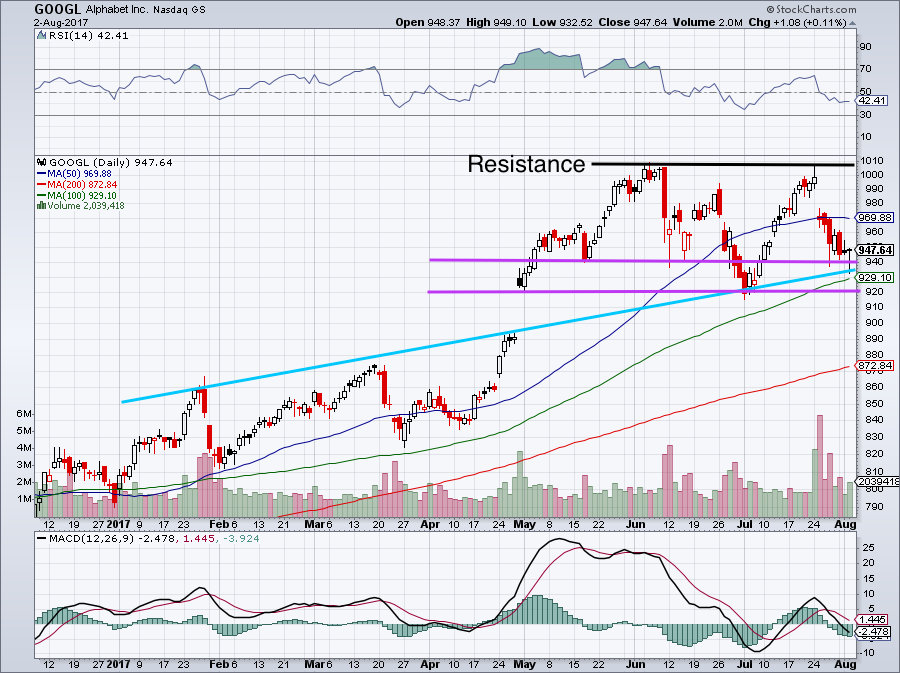

Trading GOOGL Stock

Click to Enlarge

There should be strong support between $920 and $940 per share. This support sits between the purple lines and the blue trend-line. Most recently, Alphabet stock found support at this blue line.

Will it hold up? At some point, especially after this big of a rally, most stocks will eventually break down. While it’s possible GOOGL stock bucks this trend, I would expect to see it lower at some point in time.

Should it not falter though, investors will kick themselves if they miss out — even with a small position.

This is a lights-out company and investors should feel comfortable owning a piece of the pie now and growing that stake over time. Absent a massive decline in the overall markets, GOOGL stock should be just fine. It’s a great long-term growth stock.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.