Shares of Alibaba Holding Group Ltd (NYSE:BABA) have been on a tear in 2017, up a whopping 90% so far. It’s a name many wish they’d bought, but never pulled the trigger on. With BABA stock pulling back 6% as September winds down, is that enough to get wanna-be investors on board?

Before you answer that, consider this question: Why should investors be interested in Alibaba in the first place?

We typically look at FANG stocks for a combination of growth and brand power. After all, who hasn’t heard of or used Google, now Alphabet Inc (NASDAQ:GOOGL)? Or, who hasn’t checked out Amazon.com, Inc. (NASDAQ:AMZN)? Though BABA stock is U.S. listed, many Americans aren’t too familiar with the Chinese tech giant. Certainly not as familiar as they are with the FANGs.

FANGs Versus BABA Stock

While Facebook Inc (NASDAQ:FB), Amazon and Alphabet all sport larger market caps, many casual investors may be unaware that BABA has a $430 billion valuation. It’s really just a good day of trading away from matching AMZN’s $450 billion market cap, although still $50 billion shy of FB’s $480 billion.

What’s unique about Alibaba? How about its level of growth? BABA is forecast to grow revenue 49% this year and 34% next year. That trumps every one of the FANG stocks. The closest is Facebook, with 42% and 30% sales growth expected in 2017 and 2018, respectively. Does anyone realize how massive ~50% sales growth is for a $430 billion company?

Then there’s the bottom line. Take out

Netflix, Inc. (NASDAQ:NFLX) and AMZN for a minute, because neither are focusing on profits right now. FB and GOOGL are zoned in on profits, though, and so is BABA. Sure, Facebook and Alphabet crush Alibaba on total net income, but not so much on the valuation side of things.

True, BABA stock trades at a price-to-earning (P/E) ratio of 57 vs. about 35 for both FB and GOOGL. But it’s different on a forward basis. Analysts expect Alibaba to grow earnings by 41% in 2017 and 32% in 2018 — topping both FB and GOOGL. Because of Alibaba’s superior earnings growth, its forward P/E ratio is more reasonable, at just 34. While not small, that’s not too far off the 31 for FB and 30 for GOOGL. In fact, one could argue that BABA deserves the premium, given its superior growth rates.

The point is, Alibaba is growing earnings and sales at a remarkable pace and is trumping its FANG competition in almost every way in this regard.

What Makes BABA Stock a Buy?

Some investors will still have a problem paying more than 30x forward earnings estimates. But with such impressive sales and earnings growth, bulls can make a reasonable case that BABA stock is not highly overvalued. Admittedly though, they would’ve had an easier time proving that case nine months and 90% ago.

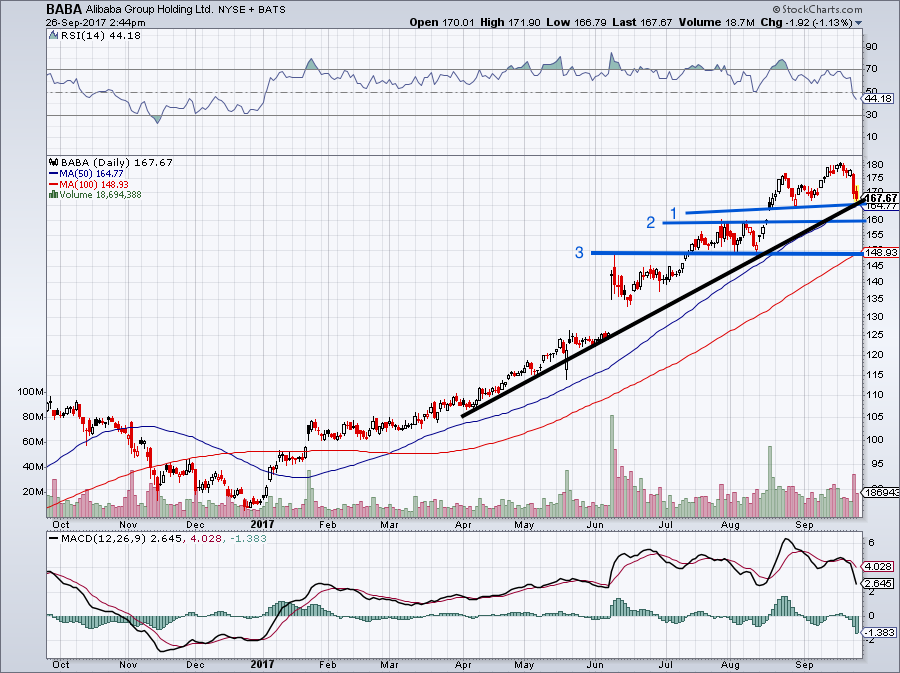

Click to Enlarge

From a fundamental perspective, business continues to hum along for Alibaba. There’s been a little margin pressure and, yes, the valuation is getting up there. One can easily make a case for staying long, but what about buying in now? That gets a little trickier. In investing, it all comes down to risk vs. reward. We could buy BABA stock today near $167 and it could fall down to $100. After all, that’s where it was trading in February and while unlikely, it could happen.

So here’s what investors can do. Looking at the chart (above), we see the 50-day moving average has been decent support, near $165. Then there’s support at blue line No. 1, 2 and 3. Also, the 100-day moving average is near $148. In other words, BABA stock has numerous layers of support. Below these levels and we could hit some serious turbulence. So, $135 and $125 would be downside targets, but the hope is that BABA stock doesn’t fall that far.

Investors can buy near current levels, and add at $160 and $148. Assuming equal purchase sizes, we’ll have a cost basis near $157.50. A stop-loss below $145 can be used. Should that trigger, we would wash our hands with an 8% total loss.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.