The bank stock earnings reports are the unofficial kickoff to earnings season. Citigroup Inc (NYSE:C) and JPMorgan Chase & Co. (NYSE:JPM) will get things started Thursday. Bank of America Corp (NYSE:BAC) will join Wells Fargo & Co (NYSE:WFC) on Friday before the bell. So what can we expect of BAC stock?

Analysts expect earnings of 46 cents per share on $21.94 billion in revenue. While this would represent sales growth of just 0.4%, it would mean more than 12% earnings per share growth. For the year, analysts expect 5.5% sales growth and a whopping 20% earnings growth.

Aside From BAC Earnings

Earnings will obviously be the big driver for BAC stock over the next few days. But there is another catalyst to note. On Wednesday, the Fed released its minutes statement. As it stands, the Fed seems likely to raise interest rates for the third time in a year this December. Investors’ hopes have dwindled over the months about whether the Fed would raise rates again. Those concerns linger for 2018, but as it stands, a December hike is likely.

Companies like Bank of America depend on higher interest rates because higher interest rates essentially translate to risk-free income, as BAC can make money on customers’ deposits. While the interest is small, it adds up quickly when the asset base is in the billions.

Bank of America’s Specifics

BAC stock has been on an absolute tear, ripping more than 60% over the past 12 months. Part of that has been because of higher rates, but largely, it’s on the back of a stronger economy and better earnings. While a strong economy translates to gains for cyclical stocks like Ford Motor Company (NYSE:

F), General Motors Company (NYSE:GM), Boeing Co (NYSE:BA) and others, banks are a winner too.

Corporate lending, consumer borrowing and more money flow all translate to profits for the banks. Additionally, a stronger economy tends to be accompanied by higher rates, and it’s no surprise to see BAC, JPM, Goldman Sachs Group Inc (NYSE:GS) and others moving higher as a result.

Despite such a large rally over the past year, one could argue that BAC stock isn’t overvalued. In fact, one could argue that it’s actually cheap!

For years, most of the bank stocks traded with a sub-1 price-to-book (P/B) ratio. In theory, a P/B ratio of 0.5 meant that if the company were to liquidate today, its stock price should double (to equal a P/B of 1). Because of the financial fallout and the carnage associated with the Great Recession though, these banks traded with a P/B ratio below 1.

BAC stock now trades with a P/B ratio of 1.04. While that may remove the asset-value catalyst, its price-to-earnings (P/E) ratio sure is attractive. Trading with a trailing P/E ratio of just 15.3 and a forward P/E ratio of 12, BAC stock isn’t all that expensive. That’s especially true for a company expected to grow earnings 20% this year and another 19.4% next year.

Buy, Sell or Hold BAC Stock?

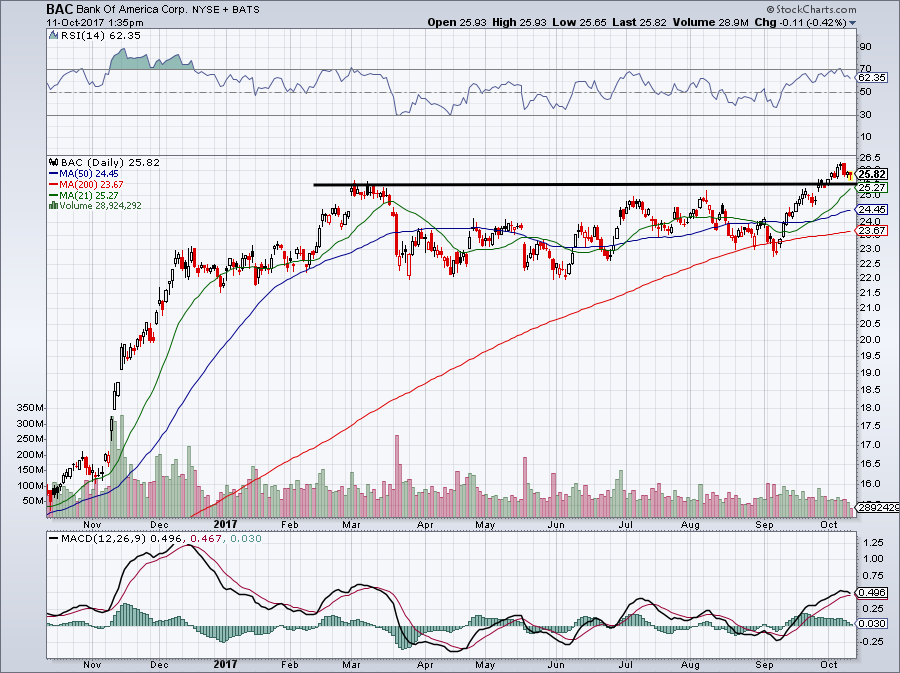

Click to Enlarge

First, investors must determine if they are investing in Bank of America or trading it. As a trader, I would not take a new position ahead of earnings. Even as an investor, one must be aware of these earnings dates.

With that said, should BAC earn what analysts expect this year ($1.80 per share) and should it maintain its trailing P/E ratio of 15.3, one could make a case that BAC stock will hit $27.50, up about 8% from current levels. Should that valuation stick through fiscal 2018 and Bank of America earn $2.15 as analysts expect, one could argue shares will be worth almost $33.

That’s all assuming BAC stock maintains its current valuation. Admittedly, it could wind up with a lower valuation. But in an era where the economy is improving and sales and earnings are growing, I don’t expect much contraction on the valuation front. If anything, one could argue for a higher valuation, given its near 20% earnings growth. On that note, BAC stock should trade for more than 12 times forward earnings.

And don’t forget about its near-2% dividend yield.

On the charts, we’re looking at $25 to $25.50 as a big level of support. The only problem? Earnings. If the report is ill-received, using a stop-loss at this level may be all for naught, as BAC stock could gap right below this level. In any regard, see if BAC stock can hold this level on a closing basis post-earnings.

If BAC stock falls, it’s one to buy on the pullback, depending on where it lands.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.