U.S. equities moved lower on Monday, a consolidation after the extreme moves seen in a handful of tech stocks on Friday following key earnings reports. Small-cap stocks were hit particularly hard — a reminder of the terrible market breadth that’s been in play lately — resulting in the worst one-day decline since August.

The catalyst fell in the form of the House’s five-year corporate tax-rate cut (down 3% per year, hitting 20% in 2022) plan, on concerns about the hit to revenues. Moreover, there is fear that fighting over individual deductions — like mortgage interest deduction — could torpedo the entire effort.

In the end, the Dow Jones Industrial Average lost 0.4%, the S&P 500 lost 0.3%, the Nasdaq Composite lost a fraction and the Russell 2000 gave back 1.2%. Treasury bonds were stronger, the dollar declined, gold gained 0.5% and crude oil gained 0.5%.

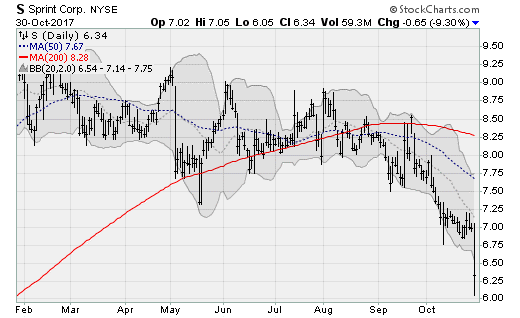

Click to EnlargeREITs led the way with a 0.6% gain with tech stocks up another 0.4%. Telecom underperformed on word M&A talks between T-Mobile US Inc (NASDAQ:TMUS) and Sprint Corp (NYSE:S) have broken down, losing 1.4%. Healthcare lost 1.1%.

Breadth was negative, with decliners outpacing advancers 1.6 to 1 with trading volume at 113% of the NYSE’s 30-day average. Diamond Offshore Drilling Inc (NYSE:DO) gained 9.5% after reporting better-than-expected quarterly results thanks to lower taxes and strength in the ultra-deepwater segment.

On the downside, Office Depot Inc (NASDAQ:ODP) lost 18.3% on a downgrade from JPMorgan citing headwinds from market share losses and office-products consumption in general. Sprint lost 9.3% while T-Mobile lost 5.4%. Chipmaker Advanced Micro Devices Inc. (NASDAQ:AMD) lost 8% on a downgrade at Morgan Stanley citing a slowdown in the CPU business.

Heading into November and the start of the holiday shopping season, J C Penney Company Inc (NYSE:JCP) lost 8% and Macy’s Inc (NYSE:M) lost 4.3% after both were downgraded at Citigroup on rising risks.

This despite what should be good news for retailers from the economic front: Personal consumption expenditures rose 1% month-over-month in September, beating estimates and ahead of the 0.1% rate seen in August.

That’s the best performance since 2009. The savings rate fell to the lowest level since December 2007, at 3.1%.

Conclusion

Click to EnlargeMonday’s pullback was to be expected after Friday’s picture-perfect rally.

SentimenTrader notes that “knockout earnings” and “enthusiastic” stock price reactions have often been a contrary indicator for the major indexes.

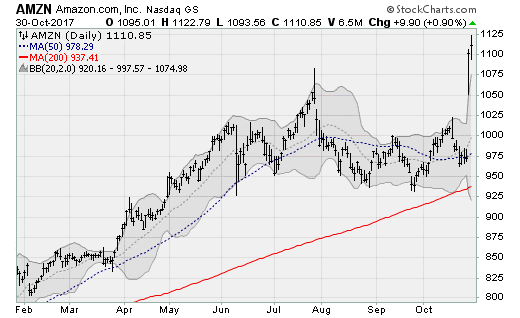

A study of market history — using Amazon.com, Inc. (NASDAQ:

AMZN) and Alphabet Inc (NASDAQ:GOOG) as the triggers — shows that chasing the enthusiasm (and buying the Nasdaq the day after earnings) has been a losing idea.

Those stocks dropped on average 0.4% one week later (vs. a 0.2% gain for any random week).

Breadth is also strikingly narrow. The S&P 500 hit a new high on Friday powered by the third-fewest stocks in 27 years. The tech-heavy Nasdaq 100 was an even more extreme example, posting its largest price gain on the fewest rising stocks since January 2000. Before that, there was an occurrence in January 1999.

Click to Enlarge Still, checking in on the 17-month moving average indicator, any weakness that results will likely be a buying opportunity.

Check out Serge Berger’s Trade of the Day for Oct. 31.

Today’s Trading Landscape

To see a list of the companies reporting earnings today, click here.

For a list of this week’s economic reports due out, click here.

Tell us what you think about this article! Drop us an email at editor@investorplace.com, chat with us on Twitter at @InvestorPlace or comment on the post on Facebook. Read more about our comments policy here.

Anthony Mirhaydari is the founder of the Edge (ETFs) and Edge Pro (Options) investment advisory newsletters. Free two- and four-week trial offers have been extended to InvestorPlace readers.