Bank of America Corp (NYSE:BAC) has been on fire over the past year, but you wouldn’t know it by the last few days. BAC stock price is down about 5% this week. Time to take profits and hit the road? Not so fast. Let’s take a look at three reasons to stay long BAC Stock.

Interest Rates Moving Higher

Whether they’re moving up rapidly or not, interest rates are at least moving higher. For years we were stuck at zero or near-zero rates, because the economy lacked oomph. Well, now we’ve got some oomph and this time it really feels sustainable.

All of that has led to higher interest rates over the last 15 months. However, we’re still a ways away from “normal rates.” So they should continue to climb over the next few years. The Federal Reserve has been telegraphing that a December rate hike is on the table. That has since become the expectation. While the Fed would like to hike two to three more times in 2018, Wall Street isn’t overwhelmingly confident that will happen.

We will see, but the trend is up. Why do rates matter for Bank of America? With one of the largest collections of customer deposits in the country, higher rates allows BAC to earn more money on those deposits. It’s essentially risk-free income. BAC isn’t the only winner, as JPMorgan Chase & Co. (NYSE:JPM), Citigroup Inc (NYSE:C), Wells Fargo & Co (NYSE:WFC), and other banks benefit too.

Valuation Remains Low

That brings us to our second point. While BAC stock price is up tremendously over the last 12 months, up 40%, it’s still reasonably priced. Trading with a price-to-earnings (P/E) ratio of 13.9 and a forward P/E ratio of 12.4, this is still a really cheap stock.

Sales are forecast to grow 5.7% this year and just 3.7% in 2018. However, earnings are expected to grow about 20% in each of those years. Using its trailing P/E ratio and 2018 estimates, it’s not crazy to think BAC stock could trade at $33 to $35 by fiscal year-end 2018. That’s about 25% to 30% upside from current levels and even more if we get a pullback.

It’s Got Dividend Plus

In August, BAC upped its quarterly dividend to 12 cents per share, a 60% boost from its prior payout. That follows a 50% increase from the following year. Management is no slouch on the buyback, either. Alongside a dividend hike, the company approved a 140% year-over-year increase in the buyback program from $5 billion to $12 billion. This follows a collective $13 billion in buybacks from 2013-2015.

Massive? No, not when you consider that BAC stock now sports a $265 billion market cap. But it’s not totally insignificant. No one will ever be like Apple Inc. (NASDAQ:AAPL), but that doesn’t mean buybacks aren’t worthwhile.

The point is, management continues to return capital to shareholders in the form of buybacks and dividends. This should make any long-term investor happy. Particularly when the company is buying back cheap stock. Shares now yield about 2.9%, while 10-year Treasuries yield 2.36%. So given that kind of yield and BAC stock’s capital appreciation, it looks pretty attractive in my view.

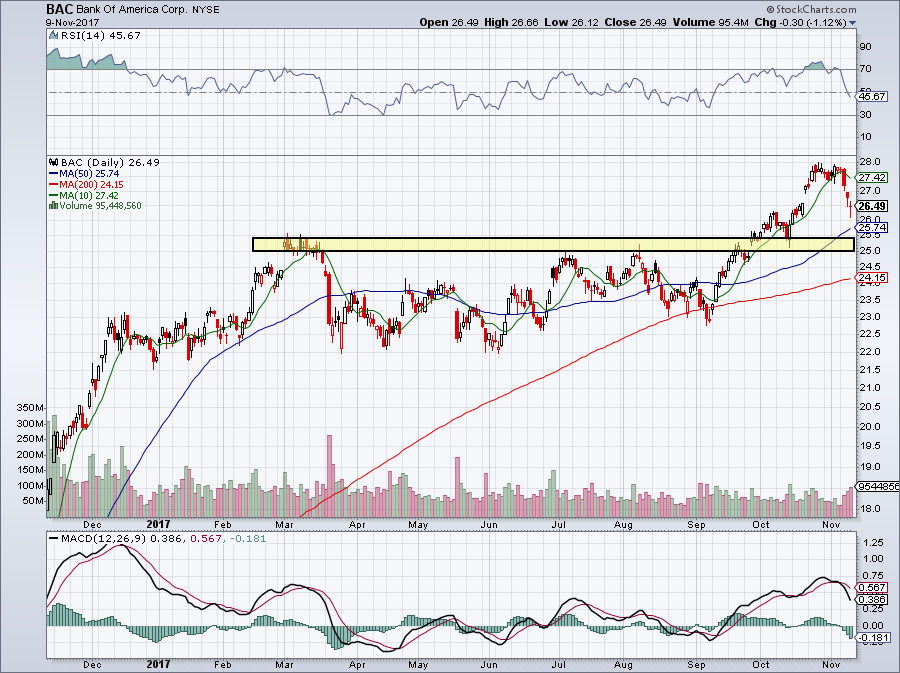

Trading BAC Stock Price

Click to Enlarge

There is strong support between $25 and $25.50. We know this because BAC stock price has been consolidating between $22 and $25 for almost a year. Once it broke above, in late September, the top of this range became support. The only question is, will BAC stock pullback to $25.50? That’s down about $1 per share from current levels.

Investors with a higher risk tolerance can buy a partial position now and add to it on a retest of the yellow rectangle (on the chart). A stop-loss can be used on a close below $25. Risk-averse investors can wait for a pullback to this level and make their initial purchase in the $25 to $25.50 range. However, it means risking BAC stock not pulling back that far and missing a run back to its prior highs near $28 and possibly higher. One could also consider sell cash-secured puts on BAC stock.

The bottom line is simple: BAC stock is one to be long. It has robust earnings growth, a low valuation and decent yield. The economy should boost its results and allow for higher rates, too.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.