Shares of AT&T Inc. (NYSE:T) are under pressure, down more than 13% over the past month and 21% this year. With T stock now trading at its lowest levels since 2015, is it time to get in or wave the white flag?

A more positive spin? Its dividend yield — 5.86% — is at its highest level since 2012. While some may see that as a negative, it’s hard to hate a big, dependable payout.

The Case Against T Stock

A few arguments can be made against T stock, the first being its lack of capital appreciation. Over the last five years, shares are down 4.3%; over the last 10, T stock has lost more than 17%. Obviously that’s not attractive. However, when including the dividend, the returns jump to a positive 29% and 45%, respectively. No, it’s not Apple Inc. (NASDAQ:AAPL), but T isn’t BlackBerry Ltd (NYSE:BB), either.

What’s also not attractive? The fact that, thanks to Verizon Communications Inc. (NYSE:VZ), T-Mobile US Inc (NASDAQ:TMUS) and Sprint Corp (NYSE:S), the wireless competition is fierce. Constantly increasing demand for more data is forcing wireless carriers to constantly upgrade their equipment to service this high demand. Will the customer ever tone down their demands? Not likely.

Making matters worse, AT&T’s $48.5 billion acquisition of DirecTV was a big one. It was meant to diversify the business and give it additional revenue streams. However, thanks to the cord-cutting trend led by Netflix, Inc. (NASDAQ:

NFLX), AT&T is incurring quite the cost to bring in new subs, while at the same time seeing quite a few heading for the exits. This is hurting margins.

So its next move? Acquire Time Warner Inc (NASDAQ:TWX) in an ~$85 billion deal. This will put obvious stress on T’s balance sheet. When considering its sizable dividend, previous acquisitions and notable CapEx, there’s reason for some concern.

Let’s Not Forget the Positives

Lest we forget that AT&T has a very strong business. Operating cash flow (OCF) and free-cash flow (FCF) remain quite impressive. Time Warner also generates positives cash flow and net income. Once its financials are added to AT&T, I think that will be good for the dividend. With a trailing FCF total of $16.5 billion, T’s annual dividend payout of roughly $12 billion is easily covered. TWX sports a trailing FCF of approximately $4.6 billion and has generated net income of $3.3 billion to $3.9 billion in each of the past four years.

In essence, AT&T has the free-cash flow to cover its dividend and make additional debt payments in the future. Because of the size of the deal, things will grow more complicated at first. Although the total cost could fall thanks to the Justice Department possibly forcing asset sales. The valuation for TWX is high for this deal, but for T investors, the focus is the dividend.

Additionally getting HBO, Warner Bros and Time Warner’s other entertainment assets are making AT&T into more of an ecosystem than in the past. Combine it with a network (AT&T) and distribution platform (DirecTV) and AT&T could be well positioned for the future.

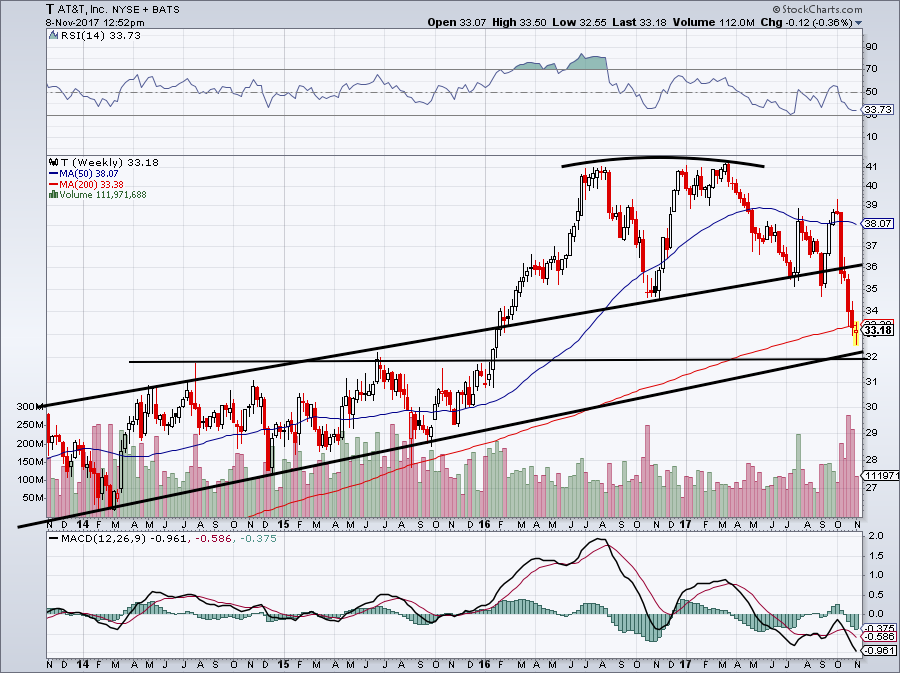

Trading T Stock Price

Click to Enlarge

Here’s the thing with AT&T: It’s not a growth stock. It’s up to investors to decide if its big yield and low stock appreciation are something they want and/or need. Looking for income? AT&T is a dependable name that yields close to triple that of a 10-year Treasury bond and has the chance for appreciation over time, particularly from these levels.

That said, if an investor is looking for growth or even a combination of growth and yield, they should look elsewhere. AT&T is similar to a bond — not structurally — but in how behaves. With that, let’s look at the stock.

Obviously $41 has been some pretty stiff resistance on AT&T. And support near $36 failed to come into play. The hope now is that ~$32 will act as support for T stock. Obviously no one can guarantee that will be case. Based on multiple levels in the past though, I would expect $30 to $32 to provide pretty solid support.

Investors going into a long T position should know that and use it as their risk/reward basis. If T stock fits your needs, considering a long-term position near current levels doesn’t seem crazy, particularly with a 6% yield.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, he did not hold a position in any of the aforementioned securities.