U.S. equities rebounded on Tuesday, but ended well off of their best levels. The session was relatively low key as investors await a double whammy on Wednesday: A Federal Reserve policy announcement (set to tease a December rate hike) and the release of the tax reform proposal by Republicans in the House of Representatives.

President Trump is also expected to announce his nominee for Fed chairman.

In the end, the Dow Jones Industrial Average gained 0.1%, the S&P 500 wafted up 0.1%, the Nasdaq Composite added 0.4% and the Russell 2000 finished higher by 0.8%. Treasury bonds were unchanged, the dollar was stronger, gold lost 0.6%, and crude oil gained 0.4% to hit its best level since February.

Click to Enlarge Breadth was positive, with 1.7 advancers for every decliner. Volume was heavy despite the tepid price action, with NYSE activity at 124% of its 30-day average.

Consumer staples led the way with a 0.8% gain while industrials were the laggards, down 0.4%. Composite decking maker Trex Company Inc (NYSE:TREX) gained 25.7% on better-than-expected quarterly numbers on strong residential demand.

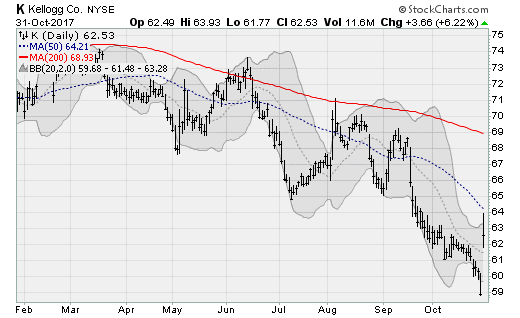

Kellogg Company (NYSE:K) gained 6.2% after a quarterly beat on better U.S. snacks sales. Mondelez International Inc (NASDAQ:MDLZ) gained 5.4% on stronger revenues.

Both represent relief for the recently battered consumer staples sector, hit by competitive pressure from Amazon.com, Inc. (NASDAQ:AMZN) and store brands.

On the downside, Under Armour Inc (NYSE:UAA) lost 23.7% after Q3 revenues missed estimates on apparel weakness. Forward guidance was cut 50% at the midpoint. Analysts were critical, citing a lack of U.S. growth and profitability concerns. AK Steel Corporation (NYSE:AKS) lost 21.5% on softer automotive demand.

And Qualcomm, Inc. (NASDAQ:QCOM) fell 6.7% after the Wall Street Journal reported the company withheld software critical to testing its chips in iPhone and iPad prototypes; Apple is reportedly considering dumping QCOM chips entirely as a royalty fight between the companies rages on.

On the economic front, consumer confidence in October surged to its highest level in nearly 17 years (since December 2000). Folks are upbeat about the short-term outlook and the health of the job market. This follows the release Monday of a big 1% increase month-over-month in consumer spending in September. All this sets the stage for a solid holiday shopping season.

Conclusion

All eyes are on the Republican tax plan to be unveiled tomorrow. Many issues remain unsettled, including the pace and level of corporate tax cuts (20% now or later?) and whether household deductions on things like mortgage interest and state and local taxes will survive.

Hopes have been elevated massively in recent months, raising the stakes for the plan meet expectations.

Click to Enlarge Looking back, October failed to live up to its spooky reputation this year with the major averages posting their best gains since February. The Dow added a massive 4.3%; while the Russell 2000 lagged with just a 0.8% gain.

This is connected to the ongoing narrowing in market breadth. Valuations grow ever more eye-watering as time goes one, with more than a year passing since the last major market pullback.

Check out Serge Berger’s Trade of the Day for Nov. 1.

Today’s Trading Landscape

To see a list of the companies reporting earnings today, click here.

For a list of this week’s economic reports due out, click here.

Tell us what you think about this article! Drop us an email at editor@investorplace.com, chat with us on Twitter at @InvestorPlace or comment on the post on Facebook. Read more about our comments policy here.

Anthony Mirhaydari is the founder of the Edge (ETFs) and Edge Pro (Options) investment advisory newsletters. Free two- and four-week trial offers have been extended to InvestorPlace readers.