Earlier this week, Piper Jaffrey once again touted Amazon.com, Inc. (NASDAQ:AMZN) as a top pick, explaining it’s only scratched the surface of the amount of money it could extract from consumers. Analyst Michael Olson even went as far as to raise his price target on Amazon stock from $1,200 to $1,400. That’s 11% above the stock’s present price.

It’s an exciting, even familiar, refrain to shareholders of a company that can seemingly do no wrong. And truth be told, Amazon has largely earned its stature among investors with its top-line growth, even if bottom-line growth hasn’t matched it.

At some point, though, the analyst community is going to have to start accepting and discussing the reality that the bigger Amazon’s e-commerce business gets, the less profitable it is. Indeed, were it not for Amazon Web Services — the Amazon’s cloud-computing arm — the company would be alarmingly in the red. And even that may not be enough in the near future.

Piper Jaffrey’s Olson upped his target on Amazon stock mostly in response to the firm’s review of data regarding consumer spending during the all-important holiday-shopping spending period late last year. In short, as big as Amazon has become, it still only captured about 4% of the money spent on gift-giving late last year. Olson opines the company is “still in the early innings of its share-gain potential,” which could be taken from rivals like Wal-Mart Stores Inc (NYSE:WMT) or Target Corporation (NYSE:TGT).

It all sounds very compelling — and believable — on the surface. Amazon.com has become a juggernaut few competitors dare stand up to. And it’s still growing the top line at a double-digit pace.

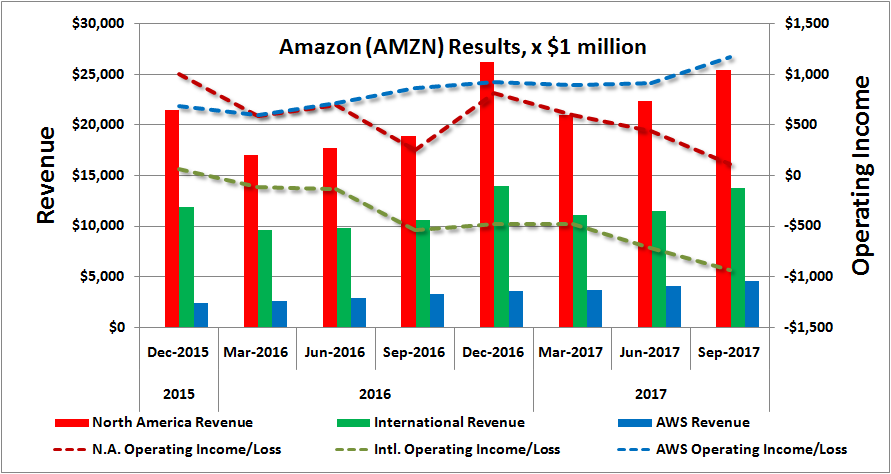

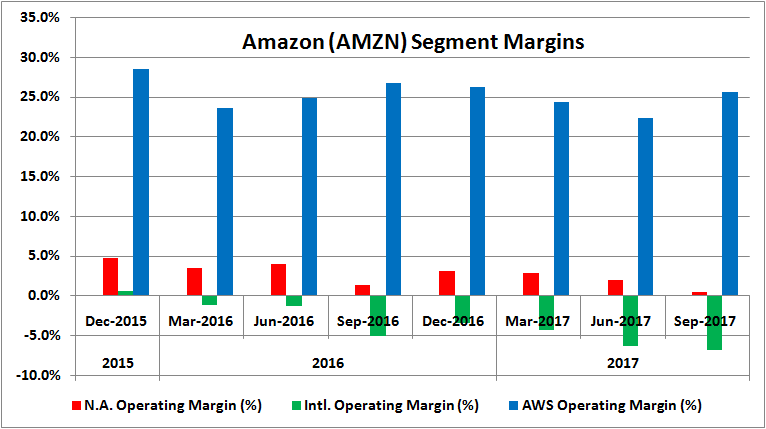

The funny thing is, the bigger Amazon’s e-commerce machine gets, the less profitable it becomes. More of the same top-line growth is likely to mean more of the same shrinking bottom line, putting all the pressure of cash flow on Amazon Web Services.

Dynamics of Amazon Stock

Click to Enlarge

Click to Enlarge

It’s not the end of the world in and of itself. Lots of companies manage different divisions of various profitability levels. If it works for owners of Amazon stock, then it works.

It’s a dynamic that should be questioned though, as it may not be able to work forever.

There are two overarching liabilities packed into Amazon’s profit mix. One of them is the one Tom Taulli explored last year, pointing out that competition from names

like Microsoft Corporation (NASDAQ:MSFT) and Alphabet Inc (NASDAQ:GOOGL, NASDAQ:GOOG) is heating up now that Amazon has proven cloud computing and cloud storage is a viable market. The more players who are in the race, the thinner margins become as a price war ensues.

The other vulnerability of such a lopsided mix of earnings? It’s not even clear how profitable AWS actually is.

Amazon’s Cash Flow Isn’t Really

It’s a bit complicated, but here’s the simple explanation: Amazon’s touted cash flow isn’t actually its cash flow. The company expenses short-lived hardware used by Amazon Web Services as a capital lease obligation. As such, the cost of that equipment isn’t deducted from cash flow, though given the short lifespan of a server, it arguably should be treated like a traditional, recurring expense. Amazon isn’t bucking GAAP rules, to be clear, but the approach does obscure the true, effective cost of keeping AWS up and running.

Either way, the heavy cost of running AWS in an increasingly commoditized environment is creating some major liabilities. A closer look at last quarter’s SEC filing shows $116 billion worth of debt and capitalized lease obligations. That’s up from just a little less than $40 billion in debt and capitalized lease obligations Amazon was sitting on a year earlier.

Those are bills that are going to have to be paid sometime by a company that could be limping along more than it seems on the surface.

Bottom Line for Amazon Stock

A pronouncement of death for Amazon stock? Hardly. If nothing else, CEO Jeff Bezos has proven he’s always got another trick up his sleeve to drive growth.

Still, these are the basis of questions that die-hard shareholders of AMZN should be asking. The company is making a massive, expensive bet on a cloud market that’s not guaranteed to be dominated by Amazon. If it’s not actually as profitable as it seems like it is, there’s no real backup plan or scenario that gets the company anywhere near its projected profit expectations.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.