It’s earnings season, and you know what that means: Banks go first. We’ve heard from a slew of banks already, including JPMorgan Chase & Co. (NYSE:JPM), Goldman Sachs Group Inc (NYSE:GS) and Citigroup Inc (NYSE:C). JPM stock rallied, GS stock fell, and C stock is jogging in place. Which direction will it go?

Citigroup stock hasn’t been my favorite bank holding. For the past year, I have been a steadfast bull on Bank of America Corp (NYSE:BAC). That stock continues to churn out new high after new high. While I continue to like BAC, it’s hard to best against C stock at this point.

Why Like C Stock?

Revenue grew just 1.5% last quarter, but both sales and earnings beat expectations. For 2017, Citigroup now has earnings of $5.33 per share. Analysts expect that figure to swell roughly 20% to $6.37 this year and another 16% to $7.38 in 2019. Analysts are forecasting revenue growth of roughly 3.5% for both years.

So we’re probably paying a pretty decent price for this growth, right? After all, 20% earnings growth rarely comes at a discount. That is, unless we’re talking about bank stocks. That’s one reason why I have liked BAC stock for so long. Its low valuation and increasing capital return has made it a no-brainer stock holding.

C stock is similar. Shares trade at a paltry 10 times forward earnings. How is that even possible given this growth? Further, Citigroup pays out a 1.65% dividend yield, while its underlying business continues to improve.

With a new lower tax rate, the bank’s bottom line should continue to swell. As the U.S. and global economies continue to strengthen, Citigroup’s core businesses will only gain strength. That’s something that can’t be repeated enough. I have said it over and over here on InvestorPlace

that investors continue to underestimate the economy and consumer confidence.

While some things can change in a hurry, the positive developments that are underway should continue in a positive direction. We’re working with an aircraft carrier, not a jet ski. Now that we have sustained momentum, it’s big momentum, and it will be hard to halt. This economic run has a lot farther to go before slowing down.

Trading Citigroup Stock

Before we get into the specifics of the C stock price, I think there’s a very important fact to consider. This company took a massive, $22–billion charge last quarter. You might be wondering, how is it possible for Citigroup to take such a large loss? More intriguing, how has the stock price not been punished for such losses? From the company’s press release:

“This charge is comprised of $19 billion related to the re-measurement of Citi’s deferred tax assets (DTA) arising from a lower U.S. corporate tax rate and shift to a territorial tax regime, and $3 billion related to the deemed repatriation of unremitted earnings of foreign subsidiaries.”

Essentially, the tax bill acted as a massive one-time negative catalyst to Citigroup, but should be a repetitive positive catalyst moving forward. Although unfortunate, it’s very bullish that the stock barely even flinched. Citigroup CFO let investors know in December that this charge was the likely outcome. Still, shares have done remarkably well over the past six weeks.

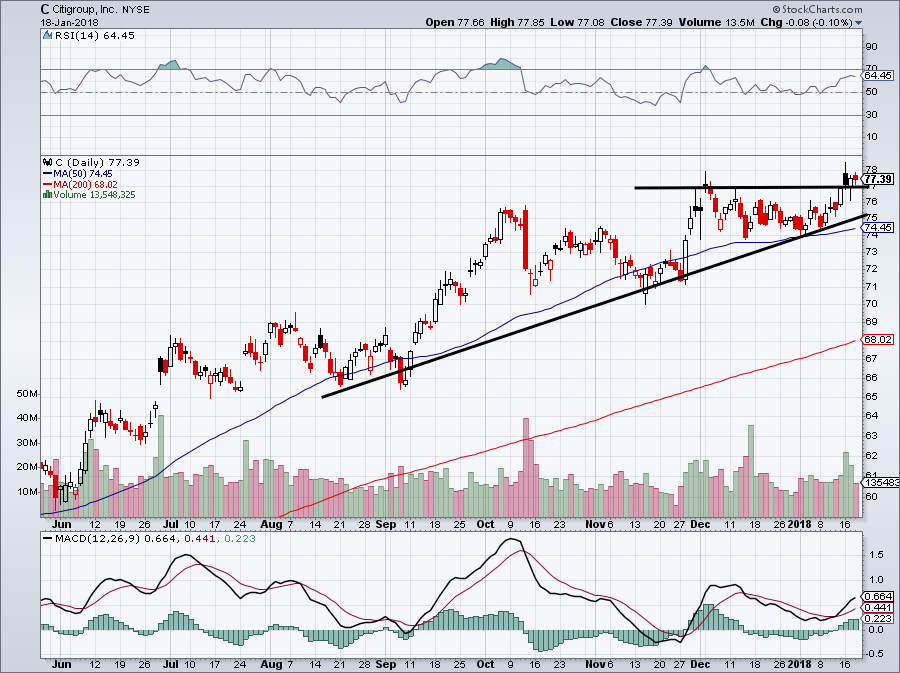

Click to Enlarge

To me, that’s bullish. When the stock can shake off a bad event like this, it tells me C stock has upside. It’s not exactly a rapid ascent, but the path of least resistance is definitely higher.

Citigroup stock is cheaper than all of its peers on an earnings and book value basis. With 20% earnings growth on the table for 2018 and the stock’s ability to hold up in the face of a $22-billion charge, I wouldn’t bet against C stock here.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.