When it comes to credit card stocks, there are five main choices: Visa Inc (NYSE:V), Mastercard Inc (NYSE:MA), Discover Financial Services (NYSE:DFS), Capital One Financial Corp. (NYSE:COF) and, finally, American Express Company (NYSE:AXP). So, should we go with AXP stock over all these others?

The first note is that DFS and COF aren’t solely credit card businesses, they have other segments too. While this helps them diversify to some degree, it’s also a drag on margins and makes them more susceptible to losses when the economy stumbles. While they are not bad companies, they don’t have the type of bread-and-butter credit card fee businesses that V and MA thrive on.

Not only do I find the business models and management teams of V and MA superior to AXP and others, but I find them more attractive in a myriad of other ways too. All three companies benefit from the growth of credit and debit over cash and check. But, more specifically, the growth overseas for V and MA is more impressive.

Another consideration? Partnerships. For years, Amex was the credit card brand for Costco Wholesale Corporation

(NASDAQ:COST), one of the only retailers that’s holding its own against Amazon.com, Inc. (NASDAQ:AMZN). Well last year, Amex lost its partnership with that company after failing to negotiate a deal that worked for both parties. Who won it? Visa.

Speaking of Amazon, Visa has also partnered on its Prime Rewards card.

Valuing AXP Stock Price

AXP stock isn’t all that bad. Just last month, shares were sporting 12-month gains of 30%. While that figure has slipped to just 17% gains, the returns are still pretty good. Further, its dividend yields about 1.5%. Expectations for 21% earnings growth and 9.5% sales growth in 2018 is also solid, even if those growth rates slow to 11% and 6.3% in 2019, respectively.

Also on the plus side is AXP stock’s low valuation! American Express stock trades at just 12.7 times 2018 earnings estimates. That’s pretty darn cheap for a double-digit earnings-grower, even if the new tax laws are giving it a big kicker this year. For me, though, I would personally rather pay a premium for a higher quality company. Visa and Mastercard fit the bill here. These stocks trade at a lofty 26 and 28 times 2018 earnings estimates, respectively.

However, analysts expect MA to grow earnings 31% in 2018 and another 17.5% in 2019. They’re calling for sales to grow a robust 16% in 2018 and 12.5% in 2019.

For V, analysts expect 26.7% earnings growth this year and 18% in 2019. On the revenue front, forecasts call for 10% growth this year and 11% in 2019.

These companies have sported double-digit earnings and revenue growth for years and, because of their overseas growth, that will likely continue. Further, just look at their margins. V sports profit margins of almost 40%, while MA rings in at more than 31%. AXP? Less than 9%. There’s a reason V and MA trade at a premium and AXP trades at a discount. In this case, I’m more than happy to pay the premium.

Trading American Express Stock

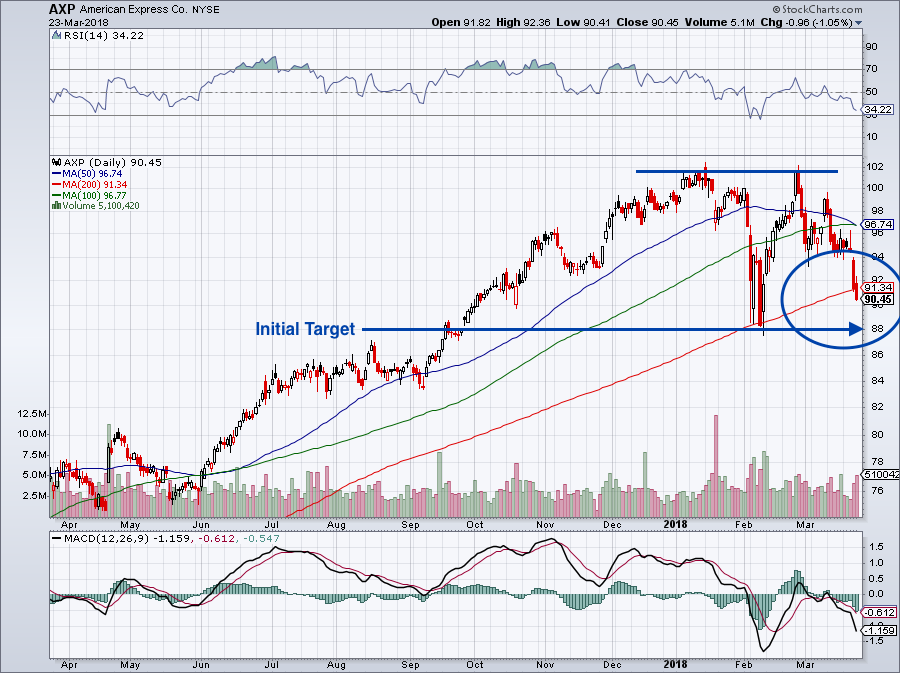

I know I’m painting a bad picture on AXP stock here, but that’s not the intent. It’s a fine company and a decent stock. I just don’t find it attractive like I do for other names in the space. That goes for the chart of AXP stock too.

Click to Enlarge

As you can see, the AXP stock price recently closed below its 200-day moving average. Resistance near $102 is pretty clear and, so far, $88 has been support. But a decline into the mid-$80s wouldn’t be surprising, as AXP stock price spent much of last summer consolidating in this area. Also, the 50-day is crossing below the 100-day moving average, showing that momentum is not working in AXP’s favor.

Now look at V and MA:

Both stock have all three major moving averages steadily trending higher. Both are pulling back into support. While they are under pressure, these charts are much more constructive than that of AXP. For this reason (and fundamentally), I’d rather go with V and MA over AXP stock.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a position in V.