If I said in January that Facebook Inc (NASDAQ:FB) stock would be trading near $150, many investors would be backing up the truck. After all, it’s the premiere platform for advertising — who wouldn’t want to buy Facebook stock?

It’s easy to ask for a pullback in certain stocks or the market as a whole. But when you see the S&P 500 down 10% in 10 days like we witnessed in February or are staring at FB stock down 20% from its highs, pulling the “buy trigger” becomes a whole lot harder.

In that regard, is it time to buy FB stock?

I’m going out on a limb to say yes, it’s time to start a position. Whether you’ve been long since its $38 IPO and were looking for a pullback to buy or have been contemplating a fresh position in the social media juggernaut, 20% declines in Facebook stock don’t come around too often.

The fear with these types of situations is: How low will the pullback in Facebook stock last?

Sizing Up Facebook Stock

Facebook’s user data issue is a bad one. It’s drawing boycotts and advertiser pushback, while causing users to question the morals of the company. It’s got CEO Mark Zuckerberg heading to Capitol Hill to testify and it raises concern about potential regulations in this space.

It also raises questions about Twitter Inc (NYSE:TWTR) and Snap Inc (NYSE:SNAP). Some have reported that both Twitter and Snap have engaged in similar data-selling practices that Facebook has. Are they next to get significantly hit?

Perhaps, but so far the social media leader has been hit the hardest. At best, FB stock would have been looking at 5% decline. At worst, it will get pummeled like Chipotle Mexican Grill, Inc. (NYSE:CMG). But that would require a decline of more than 66% or in Facebook’s case, a fall to $68. I can’t imagine a scenario where that plays out.

But what about a 30% fall to $136.50? Is a 40% decline to $117 in the cards?

Only because FB stock has fallen 20%, does a decline of 30% seem possible.

In the short-term, it’s hard to imagine much more pain. What we need to see is the business impact. Facebook still connects 2 billion people per month

. It still has impressive daily and monthly active user growth. And ultimately, it still has impressive ad, revenue and earnings growth. If these metrics take a hit, that’s how Facebook stock could see major declines this year.

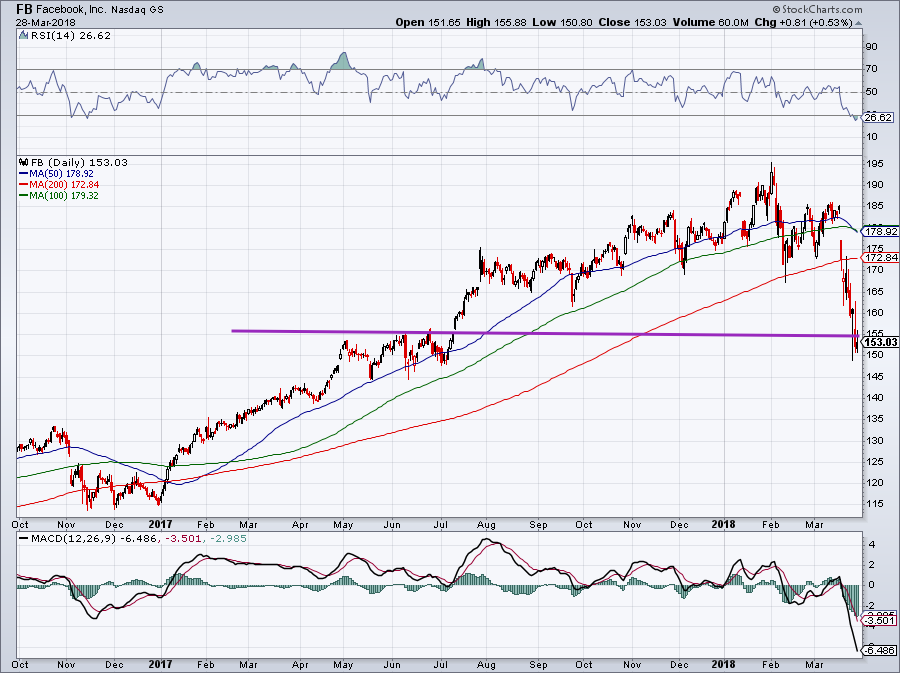

Trading FB Stock

There’s no way to put it nicely: the charts are not good. Now below the 50-day, 100-day and 200-day moving averages, the stock’s vital uptrend has been shattered. Seeing it below $155, what seems to be a notable support level, is also discouraging. While shares bounced Thursday, it’s no guarantee it will last beyond end-of-quarter trading.

Further, we’ve got the 50-day now below the 100-day, showing that intermediate trends are no longer bullish. If the 50-day moving average crosses below the 200-day, it will form what’s known as a “death cross,” a bearish technical setup. It shows that the longer term trend is no longer bullish.

Click to Enlarge

So why the heck would we want to buy this thing? Buying FB stock is ultimately a bet that it’s business will not suffer catastrophic consequences. It will suffer to some degree, but this doesn’t change the fact that the Facebook platforms are the best way for advertisers to reach customers.

I wouldn’t go all-in on Facebook stock yet. But nibbling a starter position now for a longer-term investment is a bet that FB is still relevant in 6 months, 12 months and 24 months.

Valuing Facebook

Estimates still call for earnings to grow 36% this year and 21% in 2019. Revenue estimates call for 35.8% and 27% growth this year and next. Shares trade at just 17.2 times 2019 earnings estimates. Even if we haircut this year’s earnings estimates of $7.35 per share by 20% (down to $5.88) and cut 2019 estimates by 10% down to $8.01 per share, FB stock still only trades at 19 times 2019 estimates.

On an earnings basis, it’s still cheaper than SNAP, TWTR and Alphabet Inc (NASDAQ:GOOGL, NASDAQ:GOOG). Heck, it’s even cheaper than The Coca-Cola Co (NYSE:KO) and has a valuation in line with Procter & Gamble Co (NYSE:PG).

For a company with this fat of margins — ~50% operating margins, ~40% profit margins — and this strong of growth, sub-20 times forward estimates is a good price for longer term investors.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did held a long position in GOOGL.