Buy, buy, buy! That’s likely what investors were thinking for Overstock (NASDAQ:OSTK) after the company reported earnings last week. Despite what many considered a mixed report, the market shrugged it off, with Overstock stock not only rallying, but surging.

Shares went from roughly $37.50 to $48.50 overnight, making a massive gap higher. But shares closed well off the highs on Friday and cascaded another 15% on Monday, closing just below $36.

That is some crazy price action for what seemed like a good earnings reaction. Hopefully it didn’t suck too many bulls in, only to stick them with massive unrealized losses.

So now what?

Overstock Earnings

The company lost $2.20 per share in the quarter on revenue of $483 million. The $2.20 per share loss in the quarter was much wider than last year (a loss of 29 cents per share) and much worse than analysts had expected (they were looking for a loss of 86 cents per share).

While sales grew almost 12% year-over-year (YoY), that was only a partial focus. The larger focus came from a private equity investment from GSR Capital.

The company agreed to purchase up to 3.1 million shares of Overstock stock at a 5% discount to the stock’s Aug. 1 closing price of $35.50. That’s up to $104.55 million. Further and perhaps more interesting, the company agreed to purchase up to $270 million (or 18%) of Overstock’s security token, tZERO.

80% of tZERO is owned by an Overstock subsidiary, Medici Ventures. Between Overstock stock and tZERO, GSR Capital is agreeing to purchase up to $374.5 million worth of stock and securities. For a $1.1 billion market cap stock, that’s no small move.

What else came from the report? Gulp. Well, gross margin decreased 50 basis points to 19%. Sales and marketing expenses surged 118% to $94.4 million, while G&A/technology expenses climbed 26% to roughly $64 million. Both metrics easily outpaced revenue growth.

Valuing Overstock Stock

Aside from the private equity investment, what’s there to be excited about here? Ballooning expenses, massive losses, contracting margins are all a bad sign for business. Revenue growth was about the only positive and that was only 11.8%.

Clearly valuation isn’t among the reasons for those who are making the bull case. So I guess I just don’t understand why someone would want to own Overstock over a company like Amazon (NASDAQ:AMZN), Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL

), Netflix (NASDAQ:NFLX) or Apple (NASDAQ:AAPL).

Some of these companies have solid valuations, while others are more questionable. But against Overstock stock, they’re all superior, at least on a pullback.

Analysts expect Overstock to lose $4.17 per share this year and another $2.50 per share next year. Given how far off they were on the most recent quarter though and I don’t know how much faith I would put in those estimates right now.

Here’s what kills me though. If I can’t value a company on earnings, it has to be one some other metric. Usually it’s something like market share, revenue or cash flow.

But that’s not the case here. Revenue is only expected to grow 10% this year and 7.5% in 2019. Both operating and free cash flow are negative and I just really can’t see the positives here, fundamentally speaking.

The one thing Overstock has going for it is its balance sheet. Not that it’s pristine necessarily, but it’s not bloated and gives the company some flexibility.

Trading Overstock Stock

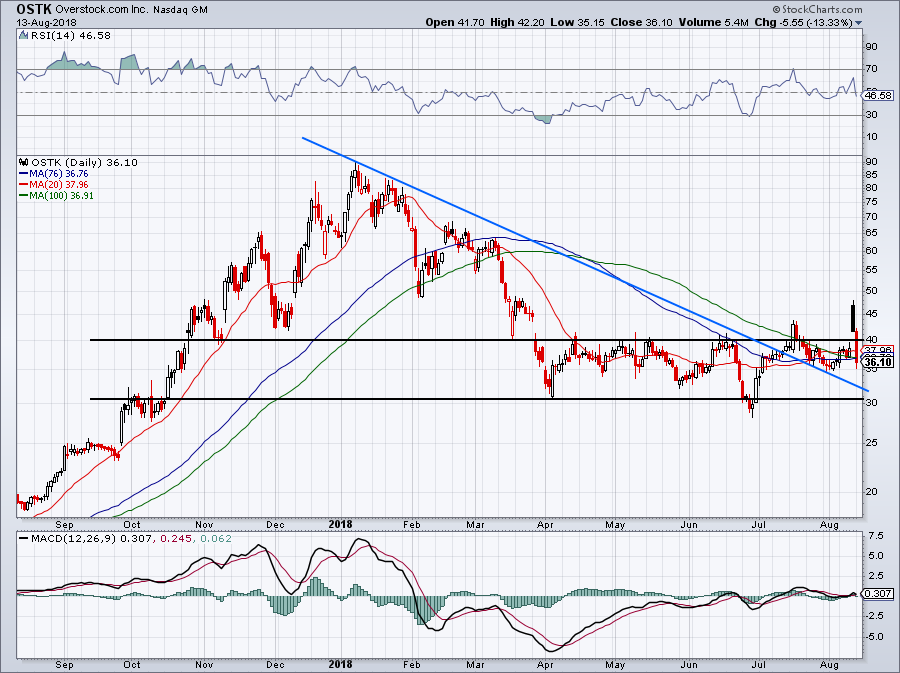

Click to Enlarge

So is this thing a no-touch at any price? Not necessarily.

After Friday and Monday’s monster decline, Overstock is now hovering just below the 50-day and 100-day moving averages. While this level could act as support, I’ve learned that Overstock is a tough one to handle.

That’s why I’m not a buyer unless it breaks out and closes over $40, or pulls back to about $30. Speaking on the latter, that’s range support and as long as the decline doesn’t happen in the next day or two, would put it near the backside of its prior downtrend (blue line).

This would represent a fall of about 20%, which certainly is not out of the cards.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AAPL.