Do you trust analysts? It would be understandable if you don’t. Too few of them were sounding the alarm bells in 2008, and too many of them still seem to be following the crowd — rather than leading it.

Nevertheless, the professionals who keep close tabs on Real Estate Investment Trust (REIT) Public Storage (NYSE:PSA) seem to see something on the horizon they’re not optimistic about. Ergo, even with ample opportunity and good reason to cast a more bullish light on PSA stock, they’re not budging. Indeed, a handful of them are voicing increasing levels of doubt.

Anything’s possible, but this is case where it might be wise to heed the advice of the folks getting paid to do the research and make the call.

Subtle Red Flags

It’s difficult, if not downright dangerous, to evaluate any REIT like a typical equity, like Microsoft (NASDAQ:MSFT) or Bank of America (NYSE:BAC). Whereas names like BofA or Microsoft are measured by clear-cut metrics like per-share profits, quirky figures like FFO (funds from operations) are better indicators of a REIT’s health.

Even then though, PSA stock is a bit of an outlier among its REIT peers such as Alexandria Real Estate Equities (NYSE:ARE) and Realty Income (NYSE:O

). Most real estate trusts collect rent from corporate tenants. Or, in the case of residential facilities, the tenants may be consumers, but they tend stay put for at least a few months at a time. Public Storage is, as the name suggests, a chain of facilities that allows consumers to store their excess possessions they arguably should get rid of, but can’t.

Nevertheless, facilitating the retention of individuals’ junk has proven to be a fruitful business.

A booming economy has boosted the purchase of new goods, yet many consumers still can’t give up their old ones. At the same time, the ongoing mass retirement of the baby boomers has led many of them to downsize their homes, but not prompted them to get rid of a commensurate number of possessions.

It’s not a bulletproof, uncompetitive industry though. Through 2020, 3,500 new self-storage facilities are expected to be built within the United States.

Though subtle, these competitive pressures may already be taking a toll on Public Storage’s results. Although the company’s second-quarter rental revenue was up to the tune of 1.7%, its core funds-from-operations only grew 2.4% on a year-over-year basis. Gross margins fell from 73.3% in the second quarter of 2017 to only 73.0% this time around. Operating income — which is still a measure that’s comparable to a more conventional company’s — fell 3.7%. The six-month figures were similarly lackluster.

The numbers could have been worse. But all things considered about the economic environment, they should have been better.

Analysts Concerned

The brewing trend is at least part of the reason Goldman Sachs analyst Andrew Rosivach downgraded PSA stock earlier this week, from “Neutral” to “Sell.” Rosivach is concerned that slowing same-store growth against a backdrop of increasing competition in this particular sliver of the REIT market could keep occupancy rates under pressure. The Goldman analyst also lowered his price target on PSA stock from $210 to $198.

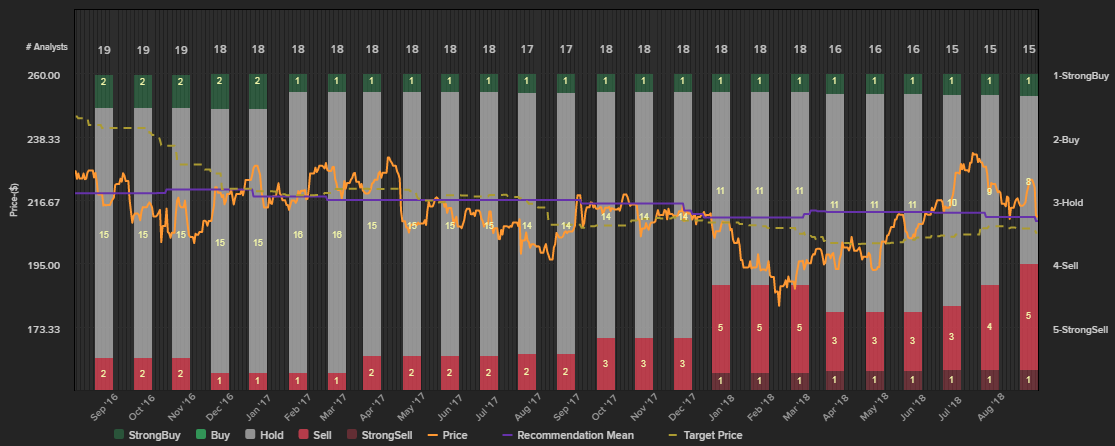

Rosivach isn’t alone in his concern. The analyst community as a whole — a community that is generally bullishly biased — presently rates Public Storage as less than a mere “Hold.” The consensus price target is $205.5, which is a bit lower than the stock’s present price near $211.20.

The pros just haven’t updated their outlooks yet? There’s no denying they aren’t always quick about refreshing their official calls. That’s not been the case with Public Storage though. These stock-handicappers have been updating their stances of late. It’s just that most of these updates have leaned in a more bearish direction — despite the stock’s ascension from earlier in the year.

Click to Enlarge

And make no mistake — when any equity meets or exceeds the consensus target or a particular analyst’s target, they know about it. If merited, they’ll respond with an adjustment. None have opted to up their view of PSA stock.

There’s a reason. It’s likely to be the same basic reason Andrew Rosivach just voiced.

Bottom Line for PSA Stock

Don’t misread the message. If your only purpose of holding onto this REIT is for its reliable dividend, that’s not likely to change anytime soon. And, if you’ve held a position in PSA stock for a while and would incur a hefty tax burden in selling it, there’s not necessarily a need to swap this name out for another.

If you’re a newcomer still mulling an entry into Public Storage, however, this is a case where you may want to think long and hard about why so many professionals just can’t get behind the stock. They’re clearly seeing something they don’t like on the horizon, despite the ticker’s respectable resilience.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.