The vast number of U.S.-listed stocks that pay dividends do so on a quarterly basis. Beyond the borders of the nation, many dividend-paying stocks stretch out their distributions to bi-annual or even annual payments. Their argument is that the company does its business and after their fiscal year is wrapped up — only then should the cash crumbs be spread out to the pesky shareholders.

But that’s not how the folks residing in the C-Suites see it when it comes to their own remunerations. They prefer to pay themselves every so-many weeks with bonuses and other perks throughout the year.

But there is a collection of companies that don’t see shareholders as a burden — but rather as the rightful owners of the company. And as such, they are paid monthly dividends — often with rising levels of distributions for attractive dividend yields. Moreover, the dividends paid are ample, more than enough to cover the meager level of inflation in the U.S. economy. And that’s a low bar.

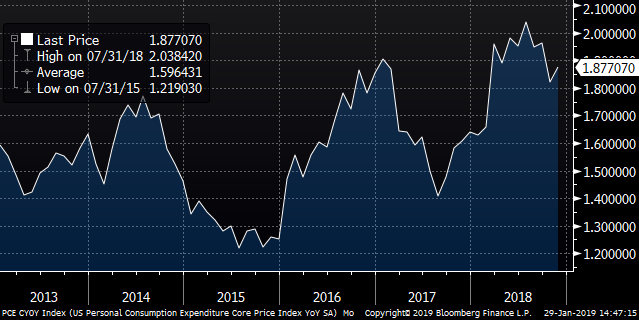

Because with the core Personal Consumption Expenditure (PCE) Index running at 1.88% — which measures the overall consumer spending cost changes in the U.S. economy and not just a constructed market basket like the Consumer Price Index (CPI) – inflation is firmly at bay for now and the foreseeable future.

Click to Enlarge

And it’s also worth noting that this is the measure that the Federal Reserve Bank uses for inflation measurements, which it would like to see it above 2% in a healthy economy.

There are varying industries that have companies paying monthly dividends. But they tend to be in businesses that are “cash cows,” providing dependable profits from which distributions can be paid. I’ve assembled a nice collection of companies that you can select to bump up your own portfolio’s cash payouts with regular to rising monthly dividends.

Main Street Comes to Wall Street

![]()

Main Street Capital Corporation (NYSE:MAIN) is set up as a Business Development Company (BDC), which is codified under U.S. tax law under the Small Business Investment Incentive Act of 1980. This act passed by Congress and signed by then-President Jimmy Carter came as the U.S. economy was in a pickle. Inflation was a problem and banks were reticent to lend to small to middle-market companies. They were concerned about the inflation risk of fixed lending facilities as well as the underlying credit risks in the business sector.

The result is that the Act extended the Investment Companies Act of 1940 that enabled non-bank companies to be formed that would be largely exempt from corporate income taxes if they made loans and equity participation investments in small- to middle-market companies. Therefore, they would be passthrough securities with investors getting paid the majority of profits that could also come with passthrough tax deductions to shield their individual current income tax liabilities.

Main Street makes loans with some additional equity participation to companies in the $10 to $100 million dollar revenue range. This is exactly what the U.S. market needs as many of the traditional middle-market commercial bank lenders have largely been sidelined thanks to onerous regulatory and capital rules stemming from legislative and administrative responses to the post 2007-2008 financial mess. And while there’s been a great deal of regulatory and legislative reforms during 2018, many of the skilled lender talent has left traditional banks and, in turn, they’ve been found in Main Street and other non-bank lenders.

Main Street gets to make loans with less regulatory and compliance costs. The result is that its efficiency ratio (a prime measure of the cost to earn each dollar of revenue is a fraction of middle-market lending banks. This means that its costs are lower and profitability is much higher.

Revenues are rising with gains running at an annual basis of 13.49% on average over the past three years.

The revenues and profitability fuel a rising dividend distribution, which has been climbing by an average annual rate of 4.06 over the past five years. And with a monthly payout yielding 6.41% Main Street is a great start to getting monthly dividend payouts.

A Triple Net Winner

![]()

EPR Properties (NYSE:EPR) is a real estate investment trust (REIT) that focuses on a very risk-controlled and efficient way to profit from real estate assets known as longer-term, triple net leases. Triple net leases are leases that are made to corporate tenants that are not only responsible for lease payments but also for taxes, insurance and general maintenance — hence the term “triple”.

This means that EPR acquires properties that have little additional costs over their leased lifespans. This means less management cost as well as less risk of uncertainty over the lease term for costs to keep up the properties as well as risks of higher taxes or changes in insurance costs.

The benefits of this means that EPR can run more efficiently in its operations with lower provisions for cost challenges for its portfolio of properties. This means more certainty in cash flows from its portfolio of properties, which in turn supports more stable revenues for monthly dividend payouts.

EPR focuses on educational properties, entertainment facilities and resort properties and facilities. So that kids are educated and they, in turn, can be entertained with family members either locally or on holidays.

The educational properties involve those that are contracted by early educational centers as well as charter schools and private schools. These provide stable reliable tenants that commit to long-term leases that are likely to be renewed to attract and keep their student populations.

The entertainment facilities are largely leased to movie megaplex theaters from national and international chains with ample branding. These are in major markets with ample demand supporting longer-term commitments for the properties.

The resorts and facilities include a variety of activities that range from major ski resorts including Camelback Mountain as well as golf courses and resorts including from operator, TopGolf. And EPR also owns a collection of water parks in prime locations. All of these benefit from the consumer trend of experience spending, which supports longer-term commitments from the operators of the properties and facilities.

All in all, the properties of EPR have been increasing revenues significantly with average annual gains running at 14.37% for the past three years alone. The triple net leases from the properties with longer-term leases continue to support significant dividend distributions. The distributions continue to rise by an average annual basis of 6.28%. And with a current yield of 6.21%, EPR is a great monthly dividend payer.

The Right Retail

![]()

Mention retailers and many investors will think that they are doomed by the likes of

Amazon (NASDAQ:AMZN) and other online behemoths. But not all retail can be replaced by a website and a few clicks. In fact, one of the more pervasive of retail space in nearly every significant city and town in America actually benefits from the surge of online shopping. That would be FedEx (NYSE:FDX), which operates thousands of stores that provide the ability to send back many of those returns from online spending sprees of American households.

Then there’s another retail space that gets attention each year at the start of the year and continues through the months until year-end. Gyms are always in demand. Either for those that need or want to lose extra pounds or those that want to keep them off while staying in better health — gyms are a reliable part of the American retail space. And one of the leaders in this retail market space is LA Fitness.

Then we have the company that is one of the major go-to retailers when it comes to picking up or having prescription drugs delivered. Walgreens Boots Alliance (NASDAQ:WBA) is one of the leaders in local pharmacies that is also a prime place to visit to pick up last minute items for health, beauty, food and household goods that just can’t always be fulfilled by the online space even Amazon’s Amazon Now.

And one of the other prime retail spaces that’s also a defense against online vendors is the super-discounted dollar stores. These stores are found in urban, suburban and rural areas where they provide bargain buys that are made by all kinds of consumers on a regular basis. They tend to have sticky and reliable customers making for good retail space. And two of the leaders include Dollar General (NYSE:DG) and Family Dollar (NYSE:DLTR).

What do the five companies all have in common? They are all long-term triple-net lease customers of Realty Income Corporation (NYSE:O).

Realty Income is set up as a real estate investment trust (REIT) which has its top tenants represented by the above companies amongst its thousands of properties across the American marketplace.

Revenues are rising across the portfolio with gains running on an average annual basis of 9.21% over the past three years alone.

This supports a nice monthly dividend distribution that continues to be raised by Realty Income by an average annual rate of 3.92% over the past five years alone. With a current dividend yield of 4.07%, O stock makes for a great inflation-trouncing monthly dividend-payer and rounds out my collection for your portfolio.

All My Best,

Neil George

Editor, Profitable Investing