Gap (NYSE:GPS) has been making a lot of changes over the past few months. It ended February with by announcing it will spin off its Old Navy brand and in March iGap scooped up Gymboree’s high-end kids line Janie and Jack. Further, despite GPS stock making a big jump after reporting earnings, those gains have evaporated as notable support is now back on the table.

There’s a feeling that the Gap stock price will continue lower into long-time support. But there’s also a feeling that because it’s so far off the recent highs — down more than 13% from its six-month peak in March — that Gap stock will soon bounce. What should investors do?

First, it should be acknowledged that a 3.76% dividend yield is not one to ignore. However, it shouldn’t be the sole consideration for investors weighing a position in GPS stock. Instead, we have to also consider the valuation, as well as other peers worthy of buying.

Valuing Gap Stock

Gap stock has some excellent assets and it’s far from the worst apparel play investors can choose. Its Athleta brand has serious potential, particularly given the momentum in similar apparel brands like Lululemon Athletica (NASDAQ:LULU) and Nike (NYSE:NKE).

That said, some of Gap’s brands are far from thriving and overall growth is somewhat stagnant. Comp-store sales growth was flat in fiscal 2018 and revenue growth going forward is expected to be sluggish, too. Analysts estimate that revenue will grow 1.1% this year and next.

When it comes to earnings, consensus expectations call for a 4.6% contraction this year and 3.2% growth in 2020. Worth noting is the company’s restructuring and spinoff of Old Navy. This will impact the top and bottom lines, but it should result in a stronger company with better margins.

Also worth pointing out is that even though analysts expect an earnings contraction this year, the consensus expectation still calls for earnings of $2.47 per share. In other words, GPS stock trades at just over 10 times earnings, factoring in some of that slowing growth.

Because of its brands and some of the good things Gap is doing, I consider it a somewhat attractive name, but not a must-own stock. At the same time, names like Target (NYSE:

TGT) are attractive with its 3.2% dividend and long history of payout increases, or Kohl’s (NYSE:KSS) with its 3.7% payout. However, I don’t mind buying GPS on a pullback into support.

So, let’s see where that support is.

Trading GPS Stock

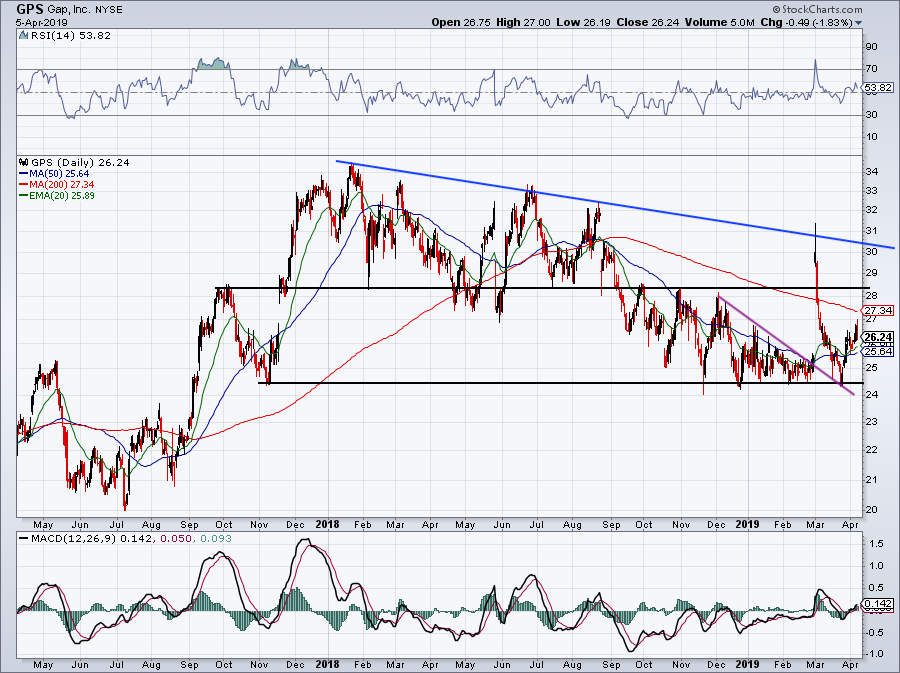

Click to Enlarge

The post-earnings surge in Gap stock to $31 has been swatted down, with shares now down below $26 after Tuesday’s 2.05% drop. Downtrend resistance (blue line) is still very much resistance and $28 wasn’t enough to support the name either. However, long-term range support near $24.50 was an excellent buying opportunity.

Not only was this long-term support, but it was also the backside of prior short-term downtrend resistance (purple line). Because GPS stock crumbled so tragically last month after a post-earnings surge, the name did not land on my radar. That’s too bad, because I’m kicking myself for missing GPS stock down there.

If the 50-day and 20-day moving averages hold as support, Gap stock can put in a higher low and start working on a move higher. If those averages fail, investors can wait for a buying opportunity down near $24.50, where GPS stock price will be sitting near long-term support and pay a near-4% yield.

Above the 200-day moving average and bulls can target $28 on the upside, with potential follow-through to downtrend resistance (blue line).

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.