For being a “dinosaur stock,” as some say, Cisco Systems (NASDAQ:CSCO) sure has been hot. Cisco stock is up 24% over the past year and has doubled over the past three years. Yes, doubled. As in, it’s done better than Facebook (NASDAQ:FB), Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) and Intel (NASDAQ:INTC) over that time span.

Short of the stock performance, it feels that, in some ways, Cisco does not get the credit that it deserves. Take its WiFi 6 networking stack. This doesn’t get a whole lot of attention — unlike 5G — but it’s something that could be just as transformative if (and more likely when

) it plays out. A passage from the linked article above:

“Wi-Fi 6 can offer 400 percent greater capacity and operate well in dense areas such as lecture halls and stadiums. The 5G and Wi-Fi 6 tandem is likely to handle outside wireless connectivity and inside, respectively.”

This is just one catalyst for a company that has many. What are they?

Valuing Cisco Stock

Cisco stock pays out an attractive 2.5% dividend yield, something that’s hard to find in the tech sector. Usually to find that type of payout, investors have to sacrifice growth. That’s somewhat true with Cisco too, at least to a certain degree. The company sports mid-single-digit revenue growth and that’s okay, but its double-digit earnings growth is far more attractive.

Analysts forecast revenue to grow 4.8% this year to $51.7 billion and 3.5% next year. On the earnings front, estimates call for 18% growth to $3.07 per share. Admittedly, those estimates drop down to growth of “just” 10% in 2020 to $3.38 per share.

A lot can change in 12 months, which is why estimates that are 24 months out oftentimes are not worth basing an investment case around. Cisco is already more than halfway through its fiscal 2019 year though, with third-quarter results due up on May 15. Better-than-expected results may get analysts to nudge those 2020 estimates higher, so let’s see how the company does this quarter.

One last note on the company’s capital return policy. Cisco stock got a boost when it reported a top- and bottom-line beat back in February. However, the company also added $15 billion to its buyback plan. The share repurchase authorization now sits at $24 billion, or roughly 10% of Cisco’s current market cap.

On a valuation basis, shares trade at 17.75 times this year’s earnings estimates. That’s not bad for a 2.5% dividend yield, double-digit earnings growth and a company that’s sure to benefit from 5G, WiFi 6 and a continuing secular trend of connected devices.

Trading CSCO Stock

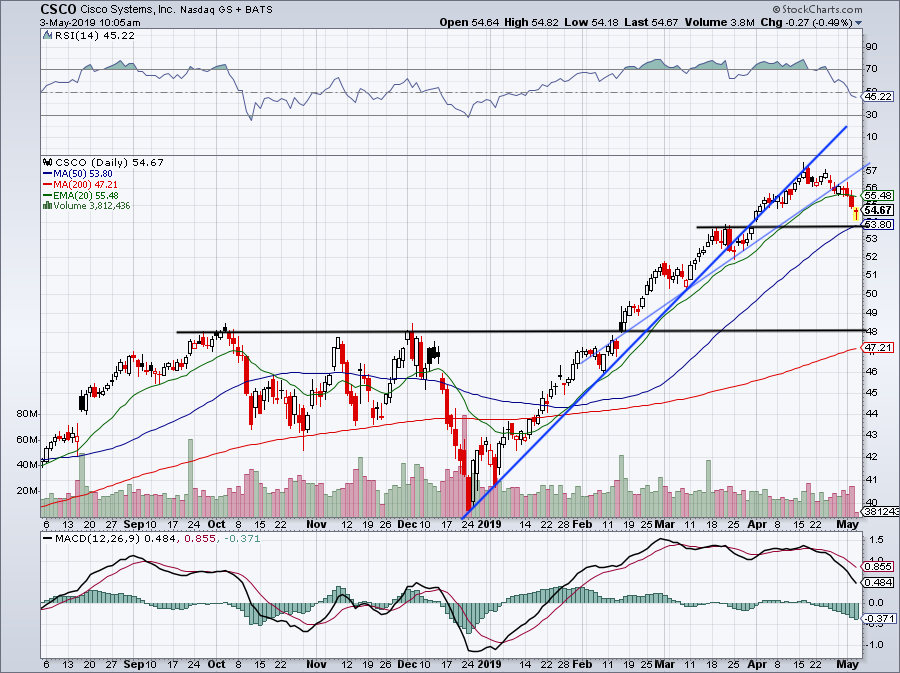

Click to Enlarge

With all that said, how do we trade Cisco stock and where’s the best spot to buy it?

There are actually two attractive spots for Cisco stock, depending on how conservative or aggressive investors want to be. Conservative bulls can consider a long position on today’s phantom test of the 50-day moving average. Shares sank in early Friday trading after Arista Networks (NASDAQ:ANET) disappointed investors with its earnings report.

Not to jump down that rabbit hole, but a quick note on ANET: The company beat on earnings and revenue estimates, but sank as Q2 guidance came up well short of analysts’ expectation. That miss is mainly due to the action of a large unnamed cloud customer.

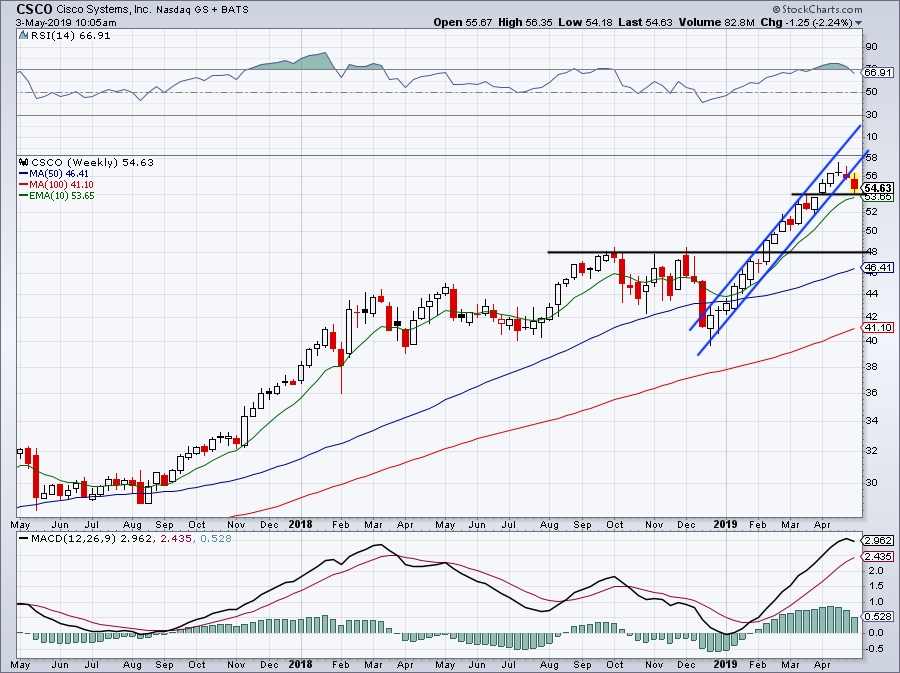

Click to Enlarge

So why should CSCO stock fall because ANET is getting less commitment from one of its larger customers? Already down about 6% from its highs and pulling into potential support, Cisco stock is a long for more aggressive traders. Below the 50-day moving average and the gap fill and short-term traders may consider stopping out.

A drop down to $48 is where I would really love to scoop up Cisco stock. It’s just above the 200-day moving average — although, admittedly, by the time it gets down there, the 200-day will likely be higher. Further, this was a big breakout area back in February after this level had been resistance all through Q4.

I don’t know if we’ll see Cisco stock back down there, but it’s a buy if we do.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell was long CSCO and GOOGL.