Micron’s (NASDAQ:MU) situation continues to deteriorate. With its margins waning and its revenue and profitability falling, MU stock price has fallen meaningfully from its highs. Just two months ago in April, Micron stock was trying to break out and exceed $45. What happened?

While the trade war was seemingly heading towards a friendly resolution a few months ago, a tweet from President Trump sent those assumptions down the drain. The tweet sank the stock market, as the PowerShares QQQ ETF (NASDAQ:QQQ) calmly shed 11.5% in the month of May.

However, it’s had a much more devastating impact on semiconductors, chip makers and memory producers. For instance, Nvidia (NASDAQ:NVDA) tumbled more than 23% in May, MU stock dropped almost 26% from peak to trough and Lam Research (NASDAQ:LRCX) dropped roughly 18%.

Comments that Broadcom (NASDAQ:AVGO) made in conjunction with its second-quarter results didn’t help. On Thursday evening, the chip maker said it expects first-half headwinds to persist in the second half of the year, after previously expecting them to lift. That caused Broadcom to issue full-year revenue guidance that was well below analysts’ average estimate ($22.5 billion vs. $24.31 billion), inflicting even more pain on the group.

What About the Valuation of Micron Stock?

Too many people look at MU stock and assume it’s a buy because of its low valuation. Many understand how price-earnings (P/E) ratios work, but some don’t. They see Micron stock trading at four or five times its earnings and say, “That’s a buy to me!”

What they don’t consider is the very basic equation of the P/E ratio. Quite simply, the ratio is price divided by earnings. When a company’s stock falls and its earnings stay flat, its valuation or P/E ratio falls, making it more attractive. However, when companies’ earnings fall, their stocks become more expensive.

When both price and

earnings fall — which is what’s been happening to Micron — the company’s P/E can remain almost constant. Last July, MU stock was trading at almost $60. Analysts’ average estimate called for earnings of almost $12 per share during the fiscal year, giving MU stock a forward P/E ratio of about five. Fast forward to June 2019 and the forward consensus earnings estimate has cratered almost 50%, down to $6.35 per share. So, too, has the stock price, which is also down almost 50%.

That’s not surprising. The decline in estimates, in conjunction with the decline of MU stock, has kept the P/E ratio relatively constant. Thus, MU stock isn’t that much cheaper now than it was in the past.

Micron’s Underlying Business

NAND memory is a component of Micron’s business, making up roughly 30% of its total revenue last quarter. However, another form of memory, DRAM, is the largest piece of MU’s pie, making up 64% of its total revenue.

Micron’s President and CEO, Sanjay Mehrotra, said this about NAND and DRAM:

“NAND markets remain oversupplied from the acceleration in bit growth driven by the industry transition to 64-layer 3D NAND. Although fiscal Q2 pricing came in below our expectations, we are optimistic that demand elasticity and seasonal trends will support improving demand growth in the second half of the calendar year.

Since our last earnings call, DRAM pricing weakened more than expected. Our demand outlook for calendar 2019 has moderated, led by somewhat greater levels of customer inventory, weakening server demand at several enterprise OEM customers and worse-than-expected CPU shortages.”

Other executives have made unfavorable observations about memory:

Anthony Neri, president and CEO of Hewlett Packard Enterprise (NASDAQ:HPE): “So the overall commodity environment continue to be favorable and there is an oversupply now compared to last year’s as you recall there was shortages and costs going up. The DRAM prices are down.”

Dion Weisler, CEO of HP Inc (NASDAQ:HPQ): “I think broadly speaking, we have seen some easing around the overall supply chain costs in the basket of commodities and logistics.”

Kelly Kramer, CFO of Cisco Systems (NASDAQ:CSCO), also said the company was benefiting from reduced DRAM prices.

Trading MU Stock

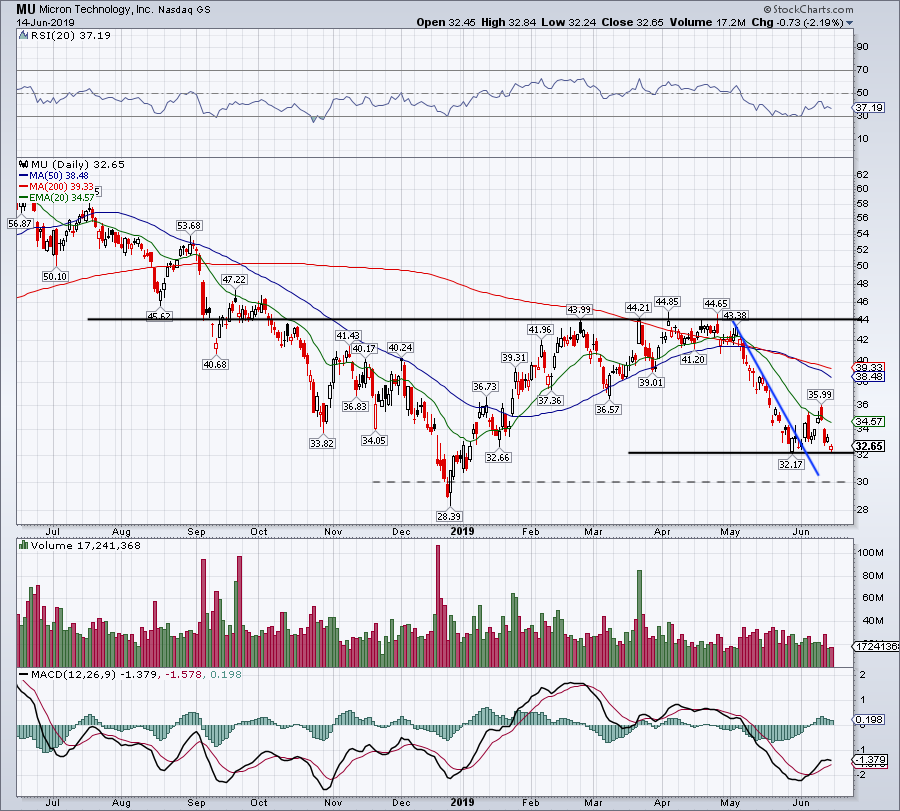

Click to Enlarge

Micron’s price action was very discouraging last week , with MU stock topping out near $36. It’s now down about 8% from those levels.

If MU stock falls below Friday’s lows, it could be in some trouble. Those lows buoyed Micron stock in late May and early June. If they can’t do so now, then MU stock could tumble to $30. If the selling pressure doesn’t relent, it could continue even lower.

Now that semis and tech have caught a bid, see if Micron can hurdle $34 and its 20-day moving average. Otherwise, Micron stock looks risky on the long side in the short-term, particularly with a percolating trade war.

With all that said, Micron is a boom-bust company. When its business is tough — like now — the ride is rough for investors. When its business is good — and it eventually will be — MU stock will be a huge winner. Even if MU slides further from here, it will likely be a good hold over the long term. DRAM and NAND aren’t going anywhere, and neither is MU stock.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long NVDA.