Boy oh boy, has CVS Health (NYSE:CVS) been under pressure. CVS stock has spent 2019 in the dumpster so far, down about 14.3% on the year now. That badly lags the 48-stock iShares U.S. Healthcare Providers ETF (NYSEARCA:IHF), which has climbed 9.9% year to date. CVS Health stock is the fund’s third-largest holding.

About the only thing worse than CVS stock has been Walgreens Boots Alliance (NYSE:WBA), which is down an abysmal 19%. Surely with so many other stocks and the broader market outpacing CVS Health stock, there’s no reason to own it. Right?

Well, that may not actually be the case.

CVS stock has some merits worth discussing, even if some investors don’t conclude that it’s a buy. Let’s take a deeper look at both the fundamentals and the technical setup on the chart.

Valuing CVS Stock

CVS stock is fueled by incredible sales, thanks in part to its acquisition of Aetna. Analysts expect revenue of $252.6 billion for 2019, a near-30% jump from the prior year.

The sheer size of that sales figure is noteworthy. In 2020, forecasts call for sales growth of ~2% to $257 billion. For comparison, Amazon

(NASDAQ:AMZN) is forecast to record about $275 billion in sales this year. Estimates call for CVS to come in just behind Apple (NASDAQ:AAPL) at $256.8 billion in revenue this year.

As for the bottom line, analysts expect earnings of $6.83 per share this year. While that’s down 3.5% from the prior year, consider the valuation. At current prices, CVS stock trades at just 8 times earnings.

That’s incredibly cheap for what is actually a high-quality retailer. Not that 2020 estimates for 4.5% earnings growth are robust by any means, but 8x earnings for decent growth shouldn’t be ignored. Further, the stock pays out a dividend yield just north of 3.5%.

Investors could question the balance sheet, which admittedly bloated quite a bit after it paid $69 billion to acquire Aetna. Long-term debt has ballooned to $86.3 billion in the latest quarter, up from $60.7 billion just six months ago and $22.1 billion at year-end 2017.

For some investors, that will nix an investment right away. That said, CVS’s balance sheet isn’t exactly pushing it to the brink. Total assets of $219.7 billion easily top total liabilities of $159.7 billion. However, total current assets of $47.8 billion are outweighed by total current liabilities of $50.6 billion, and admittedly, I’d like to see the former outweigh the latter.

Trading CVS Health Stock

To be sure, the balance sheet could be more attractive. But after all, when a stock trades at sub-10x earnings, there’s often a reason. With a decent dividend and solid growth though, some may look past those restraints and find CVS stock attractive.

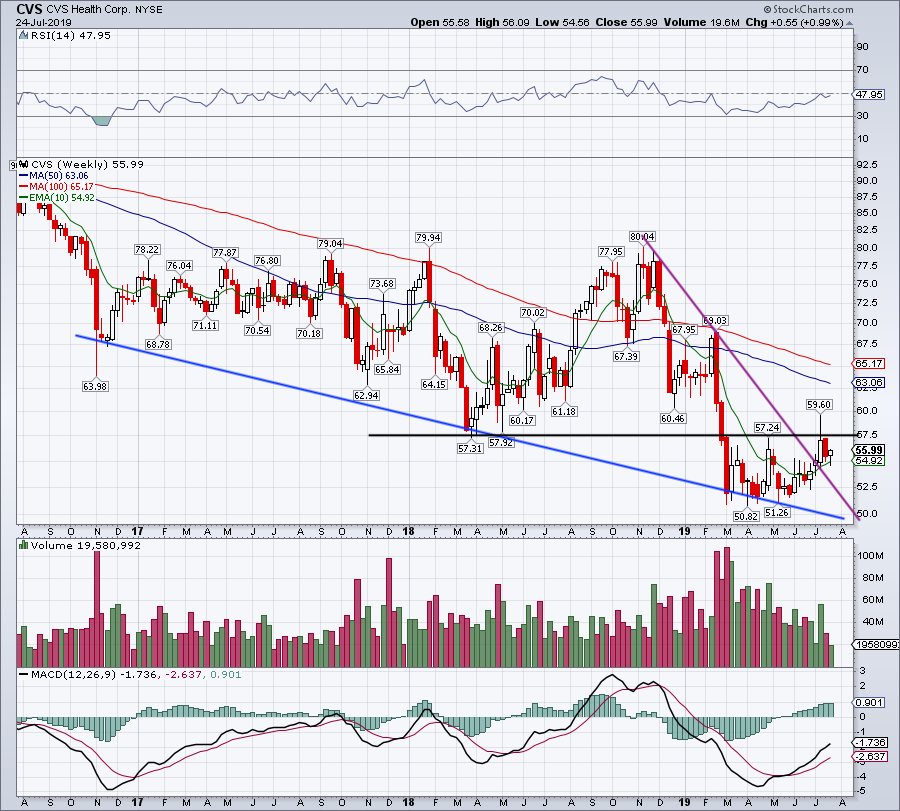

Click to Enlarge

If CVS Health stock can get its current ratio north of 1.0 and generate positive free-cash flow growth, it may quickly find its stock in demand. What else helps get a stock in demand? Bullish momentum, and CVS stock is working on it now.

Less than a year ago, CVS stock hit $80. A few months later, investors were praying $50 would hold as support. It did and now shares are trying to push through $57.50 resistance.

This level has proven itself to be significant over the past 18 months or so. Reclaiming it would be a positive development for bulls and open the door to a run higher. Above $57.50 and a run to the 50-week moving average is possible.

So far, the stock is doing a really good job of holding the 10-week moving average. If it can continue to do so, it will eventually be forced into a make-or-break situation: either the 10-week fails as support or CVS stock breaks out over resistance.

The stock still has a lot of work to do, but the recent action has been positive so far. For now, see that it holds the 10-week level.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AMZN and AAPL.