I don’t use the term “screaming buy” very often. In fact, very rarely do I use such terminology, because it can come across as disingenuous. But when it comes to Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) stock, that’s exactly the scenario we may have.

This company remains a powerhouse when it comes to online domination — perhaps too much so for its own good. Alphabet stock is facing antitrust probes from the U.S. government, as are many of its FAANG brethren. Facebook (NASDAQ:FB), Amazon (NASDAQ:AMZN) and Apple (NASDAQ:AAPL) are all likely on the list. Alphabet has also caught the eye of President Donald Trump.

While that could spell trouble down the road, remember that Alphabet dominates online search (Google) and online video (YouTube), while its collection of assets is hard to match.

Business Is Good for GOOGL Stock

Here’s the thing about Alphabet stock: the company just reported a

great earnings result. Earnings of $14.21 per share erupted past estimates by $2.75 per share. Revenue of $39.94 billion grew more than 19% year-over-year and topped estimates by more than $730 million.

Yeah, it was a good quarter.

Operating margin of 24% came in well ahead of analysts’ expectations for 22.6% and management approved a $25 billion buyback. Its “Other” category revenue easily topped estimates, with sales of $6.18 billion versus a $5.63 billion estimate. The beat was led by a strong showing from its cloud business. Management hopes to triple its cloud sales force in the coming years, showing no signs of slowing down.

Remember, the cloud is what’s helping drive Amazon higher. Additionally, it elevated Microsoft (NASDAQ:MSFT) to a trillion-dollar valuation. YouTube is the Alphabet’s second-fastest revenue grower, accelerating the top line.

Better-than-expected sales growth combined with lower-than-expected spending and consensus-beating margins helped drive the substantial earnings beat. Investors finally saw something to like in GOOGL stock, with shares rallying 10% in response to the report.

Since the selloff took hold though, shares have given up almost all of those gains.

The Balance Sheet Is Robust

What’s one thing that investors consistently overlook in my view? Alphabet’s balance sheet. This thing is a mammoth, as the company recently took the cash crown from Apple.

Alphabet boasts cash and short-term equivalents of $121 billion, up 18.4% year-over-year. Perhaps even more impressive, that’s up 6.7% from the prior quarter just three months ago. Cash makes up approximately 15% of the total market capitalization for Alphabet stock.

Total current assets are up 18.75% year-over-year. Moreover, total assets are up 21.5% and weigh in at an astounding $257.1 billion. That easily out-muscles total liabilities of just $64.9 billion. GOOGL stock may get hammered in a recession thanks to it being in tech, but almost no company seems as safe as Alphabet.

Trading Alphabet Stock

I am a long-time shareholder of Alphabet stock, but I do trade around some of my position. I was lucky enough to bail on GOOGL stock right before its first-quarter earnings in April. Shares were up more than 30% in four months and I felt it was too much, too fast. Unfortunately for me, I did not get a fill in Alphabet down at $1,020 in June.

Anyone who has followed my work on InvestorPlace knows I love nibbling on Alphabet when the GOOGL stock price drops into the $1,000 to $1,020 range. But stingy investors have been given another gift: A post-earnings pullback.

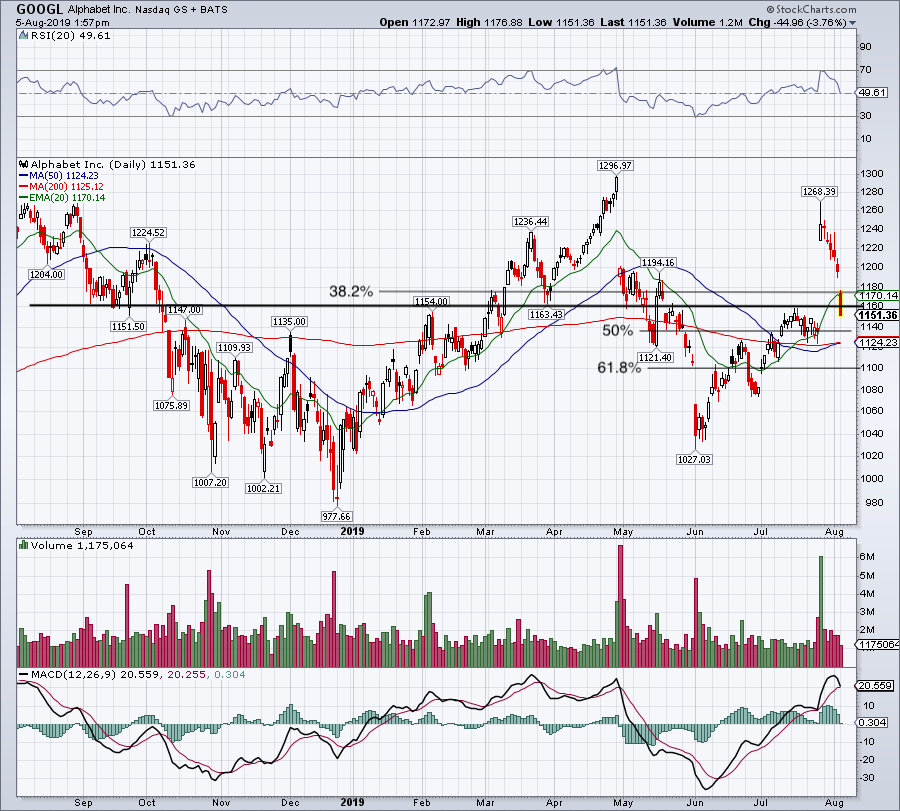

Click to Enlarge

Despite a strong rally, six straight declines since have eliminated almost all of the recent gains. On Monday, the GOOGL stock price knifed through the 20-day moving average and 38.2% retracement like they weren’t even there. That’s the same day Loop Capital analysts bumped their price target by $100 up to $1,350 on the name.

Active investors can buy Alphabet stock should it solidly reclaim the $1,170 mark and look for a move higher from there. But this is a tough environment right now and investors should keep that in mind.

Should we get a deeper pullback, GOOGL will be attractive to long-term holders. Between the 50-day and 200-day moving average confluence at $1,124 and the 50% retracement near $1,140 may be a good place to start accumulating. Below and the 61.8% retracement comes into play near $1,100.

While painful in the short-term, we’d be lucky to get another opportunity below $1,040.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AAPL, AMZN and GOOGL.