Strong second-quarter results from Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL), posted on July 25, are nothing short of breathtaking. Google stock should soon be back to its winning ways.

The company beat consensus estimates on earnings and revenue by a wide margin. Even though the stock topped $1,250 on July 26, Alphabet stock fell as selling pressure on the tech index weighed it lower.

With 19% year-on-year revenue growth at its size, the search engine giant will keep rewarding its investors.

Strong Q2 Results

Alphabet reported revenue growing 19% Y/Y to $38.9 billion. Improvements to its core information products clearly paid off. Developments in its products, such as Search, Maps, and Google Assistant all contributed to the higher revenue. The Google properties revenue growth is most notable as it increased from $23.3 billion to $27.3 billion.

For the quarter, Google’s advertising revenue was $32.6 billion, easily off-setting the approximately $1 billion loss from its “other bets” division.

Traffic acquisition costs, or TAC, to Google Network Members and distribution partners, was steady at 13% of Google properties revenue. On an absolute basis, costs rose slightly to $7.2 billion. Despite Alphabet stock getting caught up in the 3.6% weekly decline on the Nasdaq (NASDAQ:QQQ), management signaled confidence in its future.

On Jul. 24, the Board of Directors authorized a share buyback of up to an additional $25 billion. The stock already bounced back from the June lows of $1,050, closing recently at $1,176. With that in mind, the company might wait for a dip below the 50 and 200-day simple moving average of $1,125 before buying back shares.

Strong Balance Sheet and Alphabet Stock

Alphabet did not report any noticeable weaknesses on its balance sheet in Q2. It recorded a slight increase in accrued expenses and other liabilities but nothing that would concern investors. Income from operations more than offset any of those cost increases. And with an EPS of $23.91, the stock trades at an annualized P/E of just 12.3 times.

To diversify its business away from the advertising on its products, expect Alphabet to continue aggressively growing its home assistance product line. Consumers are becoming more willing to run Internet searches using their voice. Plus, by getting many home assistance tasks done on Google Home hardware, the company gains more insight into the consumer’s search needs.

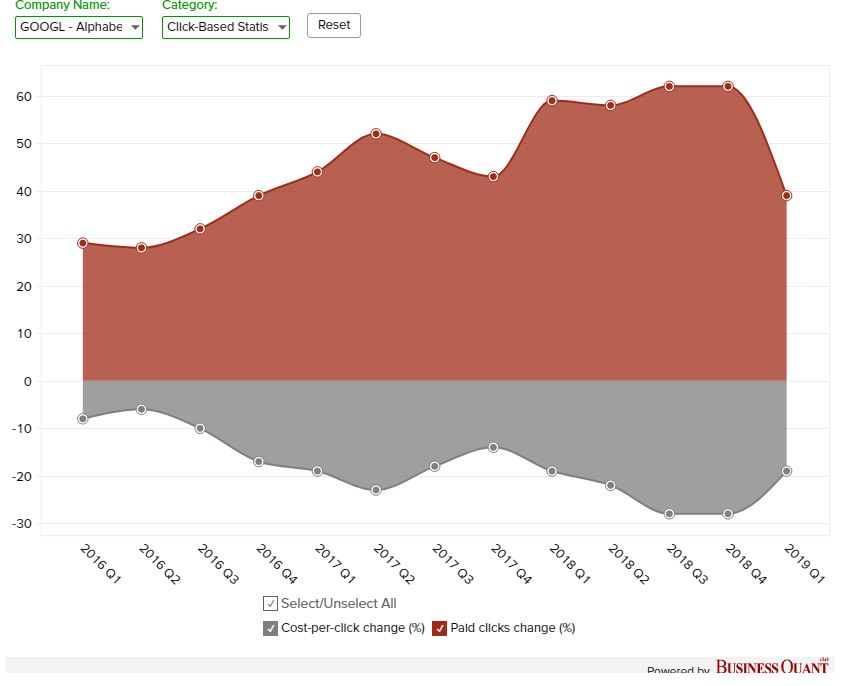

Below: revenue from clicks fell in Q1, only to recover in Q2.

Source: BusinessQuant

On the smartphone front, Google is set to release Pixel 4. When Pixel 3 had a notch, it hardly differentiated itself from Apple (NASDAQ:AAPL) iPhones. So this time, Pixel 4 gesture controls will most certainly differentiate itself from current and future iPhones.

Indirectly, Pixel 4 devices become a reference design for Android manufacturers. The better Androids become, the more likely users stay on the platform, using Google search, among many things, as their preferred search engine.

Two new features coming to Pixel 4 may entice consumers to upgrade to the latest Pixel. Pixel 4 will have motion sensing, using radar and being the same technology as that used to detect planes and objects.

But the “Soli,” as it is called, will sense small motions around the phone. It will recognize gestures and detect when the user is nearby. Face unlock, which Samsung already offers in its Galaxy phones, will come to the upcoming Pixel. But it will work differently. Once it senses the user nearby, it will unlock if the face sensor and algorithms recognize the owner. In effect, the phone will unlock as the phone is picked up, all in one motion.

Valuation and Your Takeaway

35 analysts who cover Alphabet stock on Wall Street have an average $1,390 target price. This valuation is consistent in a 10-year DCF Revenue Exit model whereby the terminal revenue multiple is 4.2 times. With a discount rate of between 10%-11%, the fair value is close to Wall Street’s estimate.

Profit-taking on Alphabet stock started on July 26 but that selling pressure is weakening. The tremendous earnings growth, driven by advertising revenue, justifies a higher share price. New hardware developments in smartphone and home assistants also strengthen Google’s branding with customers. Continue accumulating GOOG stock as the stock climbs higher.

Disclosure: As of this writing, the author did not hold a position in any of the aforementioned securities.