There’s no point in sugar coating at this juncture. Simply put, eclectic and quirky home furnishings and accessories retailer Pier 1 Imports (NYSE:PIR) could be the worst investment ever. Featuring an erratic price history over the last 20-plus years, patience may have finally run out for PIR stock.

If management was hoping to start the new year (and decade) on a high note, it turned out to be an abysmal failure. Just in this month alone, PIR stock dropped a staggering 46%. According to Stockrover.com’s profile, shares have received an overall score of zero. That’s due to myriad problems, including growth woes and severe concerns regarding fiscal stability.

Adding to the litany of distractions, Pier 1 announced earlier this month that they will close 450 stores. Roughly speaking, that amounts to half its total store count. On one hand, that might improve the company’s fiscal picture. However, the bottom line is that no successful business constrains their footprint.

Click to Enlarge

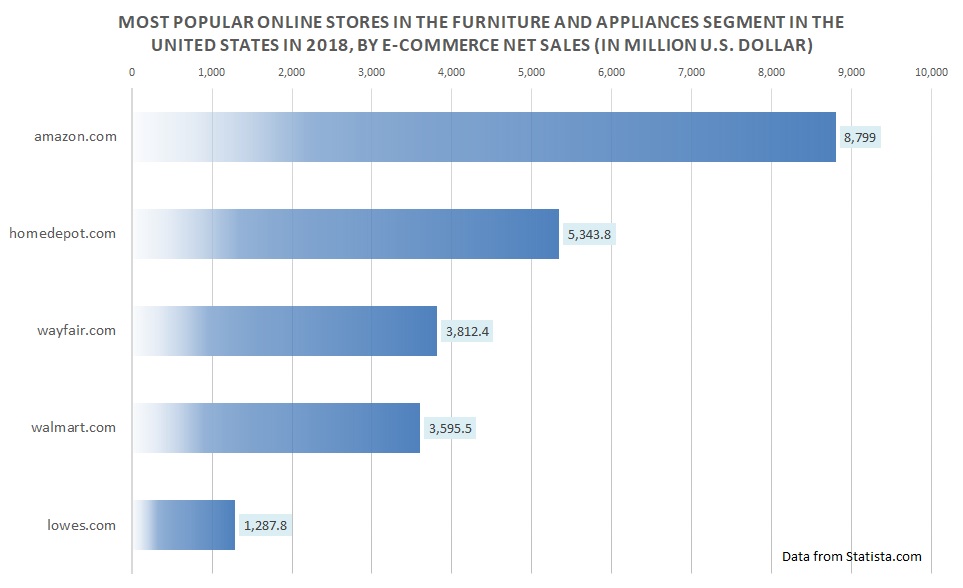

And while no one can predict the day-to-day swings of PIR stock, longer term, the writing is on the wall. Most worryingly, Pier 1 is no longer relevant compared to the competition. Even though Amazon (NASDAQ:AMZN) doesn’t necessarily focus on furniture and appliances, it delivered $8.8 billion in segment sales in 2018. And Home Depot’s (NYSE:HD) online division rang up over $5.3 billion.

Other major competitors in online furniture and appliance sales include

Wayfair (NYSE:W) and Walmart (NYSE:WMT) at $3.8 billion and $3.6 billion, respectively. On the other hand, Pier 1’s total 2018 revenue was a paltry $1.8 billion.

PIR stock appears a lost cause. But a more interesting take is what it implies for the U.S. economy.

Home Furnishings Sales Possible Harbinger for PIR Stock and the Nation

In my article about Pier 1 competitor Wayfair, I mentioned the risk of W stock jumping past its fundamentals. Specifically, median sales prices of homes sold in the U.S. have been declining since late 2017. Further, home furnishings sales, though rising since late 2017, have only just started to exceed their pre-Great Recession heights.

In other words, the home furnishings sector’s recovery is unconvincing. Moreover, if we are truly recovering from the Great Recession, we should see robust growth in this retail segment. After all, our home is where we spend the most time. Therefore, consumers are incentivized to spend their discretionary income for furniture and decor.

On the flipside, home furnishings is where most consumers will tighten their belt if they’re under financial pressure. Interestingly, The New York Times’ Julie Scelfo noted as such on Jan. 28, 2009. Scelfo wrote:

Home furnishings retailers are likely to remain vulnerable throughout the recession, said Joseph Feldman, an analyst at the Telsey Advisory Group in Manhattan who studies retail markets, because consumers no longer believe they should buy new things when what they have is adequate.

“If you’ve got less in your pocket and you’re worried about putting food on the table, you’re not going to be buying new throw pillows just because Pottery Barn has a new color,” Mr. Feldman said. “Given the state of the economy, consumers are doing more with what they have.”

Another way to look at it is that American consumers today still have a recession-era mentality. Money talks and it’s not being spent on home furnishings. Thus, the losses of PIR stock speak to more than just one company’s troubles.

Maybe a Dead-cat Bounce and That’s It

One of the startling takeaway’s about Scelfo’s NYT article is that if I didn’t disclose its publication date. And if I changed some of the company names around, you’d think she was reporting on current events. For example, Scelfo reported that:

Earlier this month, Williams-Sonoma, which owns the distressed Pottery Barn brand, announced that it would shed 1,400 jobs, and Waterford Wedgwood, the venerable crystal and china maker, filed for insolvency administration, the British version of bankruptcy protection. Lenox, the 120-year-old American china company, filed for the American version in November.

Basically, the home furnishings market has moved back in time to the Great Recession, yet the major indices are at record highs. That should at least give you pause.

Nevertheless, it’s not all bad news for PIR stock. Technically, shares are riding a support line a few cents above $3, representing last year’s closing low. So, it’s not out of the question that the equity could perform a dead-cat bounce.

What is out of the question – at least for rational investors – is holding on for a recovery. Sadly, this is a terminally ill stock. But the reason why it became that way is the biggest lesson you should glean from Pier 1.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.