Cisco Systems (NASDAQ:CSCO) is a free cash flow powerhouse. The market doesn’t appreciate this very much, and so Cisco stock is deeply undervalued. But I believe Cisco stock is worth a good deal more if you look at it from a different — and perhaps unrecognized — standpoint.

The market has not taken to the stock. For example, over the past year, the stock has fallen over 9%. So far this year, Cisco stock is down 1%.

Granted, the company’s sales and earnings have fallen as well. One reason why the stock has dropped could be its top-line performance.

For example, as of its April end quarter, Cisco posted sales of $12 billion. That figure was down 8% from $12.96 billion a year earlier. And net income was 8.9% lower at $2.77 billion, against $3.04 billion.

Click to Enlarge

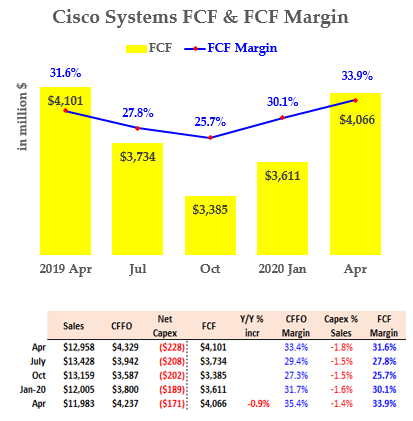

But here is what the market is missing. The company’s free cash flow has performed very well. Look at the chart on the right.

Cisco’s free cash flow was steady. FCF in the quarter ending April was $4.07 billion, but a year earlier it was $4.1 billion. That is flat year-over-year.

Moreover, and more importantly, the company’s FCF margin was actually higher. For example, the ratio of FCF to sales was 31.6% a year ago, and during its latest quarter, the FCF margin rose to 33%.

Cisco’s Amazing FCF Conversion Rate

FCF has actually risen and is higher than its nominal net income. For example, in its fiscal Q3 ending April, FCF was over $1 billion higher than its net income for the same quarter. Net income was $2.77 billion, but FCF was $4.07.

Analysts call this a conversion rate of 146%. That means that for every dollar of net income, $1.46 of FCF is generated. In this case, $2.77 billion of net income converts into $4.07 billion of FCF. This level of conversion is high on a relative basis.

For example, let’s look at some other super-profitable tech stocks and compare their conversion rates with Cisco. Microsoft (NASDAQ:MSFT) made $11.2 billion in its latest quarter in terms of net income. But its FCF was $13.9 billion. That gives it a conversion ratio of 124%. This is lower than Cisco’s 146% rate.

Apple (NASDAQ:AAPL) made $11.25 billion, but its FCF was $14.7 billion. That gives it a ratio of 131%, still lower than Cisco. Both of these companies are hardware/software tech companies just like Cisco.

Alphabet (NASDAQ:GOOG, NASDAQ:

GOOGL) converted its $6.96 billion in net income into $8.6 billion of FCF. That is a conversion ratio of 124%, still lower than Cisco’s. Oracle (NYSE:ORCL) made $3.18 billion in FCF in its latest quarter, but net income was $3.12 billion, for a conversion ratio of 102%.

You get the picture.

Cisco’s ability to make cash profits is very high. This makes Cisco stock very cheap as well.

It’s All About High FCF Yield

Cisco’s market capitalization is just over $200 billion. It generated $4.07 billion in FCF in its latest quarter. On an annualized run-rate basis, this represents $16.3 billion in FCF. So compared to its market cap, the FCF yield is 8.1%.

That is also a very high FCF yield. For example, Microsoft’s FCF yield is 3.5% and Apple’s is 3.1%. Alphabet’s FCF yield is 3.34%. Even Oracle is slightly lower — its FCF yield comes in at 7.5%.

The FCF average of this peer group is 4.36%. We can use this to help derive a value for Cisco stock.

For example, if we take Cisco’s annualized run-rate FCF of $16.3 billion and divide that by 4.36%, we get an implied market cap of $380.5 billion. That is 90% higher than its present $200 billion market cap.

In other words, CSCO stock is worth $90.11 per share, or 90% higher than its price today of $47.43.

What Should You Do With Cisco Stock?

Cisco is going to announce its Q4 earnings and free cash flow figures on Wednesday, Aug. 12. A simple thing to do is compare its quarterly FCF and see if the company is still on a run rate of producing $16.3 billion in FCF.

If so, this stock is very undervalued, as I have indicated above. I am not the only analyst who thinks so. Seeking Alpha reported that Morgan Stanley came out with a similar recommendation. Analyst Meta Marshall also likes the company’s flexible cash flow.

However, other analysts think this is a dull stock. According to Barron’s, JPMorgan Chase came out with a report at the same time downgrading the stock because of its negative revenue growth.

You know what I think about that. Free cash flow is used to pay dividends for shareholders, not revenue. In fact, Cisco still both repurchases its shares and pays a dividend. And why not? It has an 8.1% FCF yield. Its dividend yield is 3%. Each quarter Cisco’s share count falls, increasing the value of future dividends and earnings per share.

Look for an opportunity to average cost into Cisco stock after the earnings. If analysts seem disappointed, you will have a chance to buy it cheaper.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. He runs the Total Yield Value Guide which you can review here.