Advanced Micro Devices (NASDAQ:AMD) will report earnings after the close on Tuesday July 27. AMD stock hasn’t been the worst performer out there, but it has been suspiciously quiet for about a year now.

While frustrating, that type of consolidation is incredibly healthy in my view. It gives the stock time to rest and a chance for it to build up some power to push higher. Of course, it’s even more frustrating when the overall markets continue to grind out all-time high after all-time high. Unfortunately, that also creates risk. Because an eventual correction in the broader market could unfairly hit AMD stock.

Regardless, this company is set to report earnings soon. I’m long and staying long and nothing this quarter will change that.

Why I’m Staying Long AMD Stock

The simple answer is usually the best answer and that is, I’m staying long AMD because it continues to generate impressive growth.

Analysts expect substantial growth in both earnings and revenue. The year ago revenue and earnings per share were $1.93 billion and 18 cents respectively, and the average estimates for the upcoming report are $3.62 billion and 54 cents respectively. For the naysayers: no, that’s not just a post-Covid rebound.

AMD did robust business throughout 2020, continually blowing away consensus expectations. For 2020, estimates called for about $7 billion in revenue and 60 cents in EPS. AMD delivered over $2 per share in earnings on $9.76 billion in revenue.

Estimates for 2021 have exploded higher over the last 12 months. This is something I have been writing about for a while now, continually pointing out how conservative the analysts have been. The same goes for Nvidia (NASDAQ:NVDA) too.

For what it’s worth, I am long NVDA stock as well. Like AMD, that thesis is simple too — it continues to generate above-average growth. Nvidia is building the backbone to various technologies and while it’s playing a larger role in that regard than AMD, both are helping to build our technological future, which is why I like both of them for the long term.

The focus doesn’t come down to any one quarter or earnings report. With a long-term view, investors understand there will be bumps in the road. Eventually those “conservative” analyst forecasts will likely become “aggressive” forecasts and these companies will disappoint. Perhaps that quarter is even among us in a few days. But the long-term demand for AMD’s products isn’t over and that’s why I remain bullish on this company.

Digging Deeper

AMD’s turnaround has been spectacular. Once left for dead and trading for sub-$2 in February 2016, it’s hard to imagine the run AMD has been on. Unlike many other companies with explosive revenue growth, AMD’s management has had the discipline to turn those dollars into bottom-line improvements.

AMD has become profitable, cash flow positive and lowered its debt load. More assets and fewer liabilities are a great combination for Wall Street.

Now the

company is likely set to acquire Xilinx (NASDAQ:XLNX) for $35 billion. For that much money, one could argue that AMD could have acquired something a bit more exciting with more growth.

Honestly, I agree with that. But Nvidia could have acquired something more exciting than Arm, too. With these acquisitions, it’s not always about “exciting.” Instead, it’s about adding depth to the financial roster.

Look at Nvidia’s acquisition of Mellanox, a quiet company that had steady growth, earnings and cash flow with a low valuation. Nvidia scooped it up, tucked it into its current operations and instantly expanded its profitability.

AMD’s hoping to do the same thing with Xilinx — although Xilinx’s valuation is a bit higher and AMD is using stock to finance the deal. Admittedly, that can create some headaches when it comes to AMD’s stock price, but it should be better off in the long haul with Xilinx rather than without it.

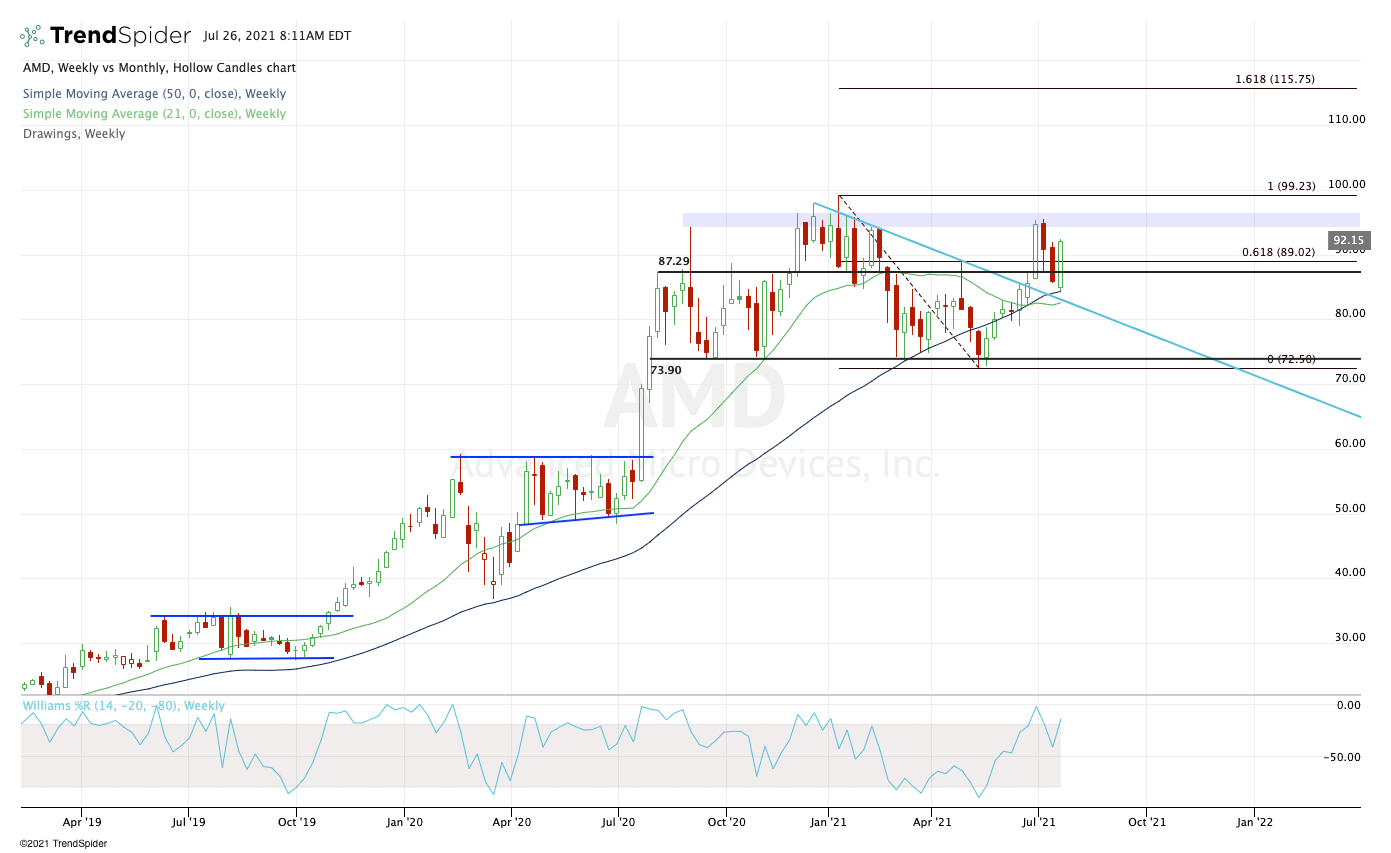

Trading Advanced Micro Devices

Click to Enlarge

In early July 2020, AMD stock exploded higher. That’s as the company was dominating against Intel (NASDAQ:INTC) and as the latter faced a large delay in one of its chips. However, AMD has been relatively range-bound since.

Stuck between $74 and $87, the stock has had trouble getting out of this range. When it has, $95 has served as resistance.

Last week, AMD gave bulls a bullish engulfing candle by opening below the prior week’s range and closing above it. That’s positive, although earnings will be the main driver of the stock’s price action in the short term.

On a bullish post-earnings reaction, I’d love to see a push up through $95. Above $95 puts the all-time high of $99.23 in play, along with $100. Above $100 opens the door to 161.8% extension around $115.

On a bearish post-earnings reaction, I want to see AMD stock hold the $87 to $89 area. Below that puts the 50-week and 21-week moving averages back in play. Below that and $80 or lower could be on the table.

On the date of publication, Bret Kenwell held a long position in AMD and NVDA. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell.