Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) is an easy stock to overlook despite its nearly $2 trillion market capitalization. Yet, GOOGL stock has attributes to satisfy most investors’ needs, whether you’re an old-school, value-oriented investor or focused on high growth.

Think about it. GOOGL stock has the growth and performance to anchor a growth-stock portfolio, which can easily see big swings in both directions. It also has the balance sheet strength and a reasonable enough valuation for more conservative investors.

Let’s take a look at five reasons investors should consider taking a position in GOOGL stock now.

GOOGL Stock vs. the Other FAANGs

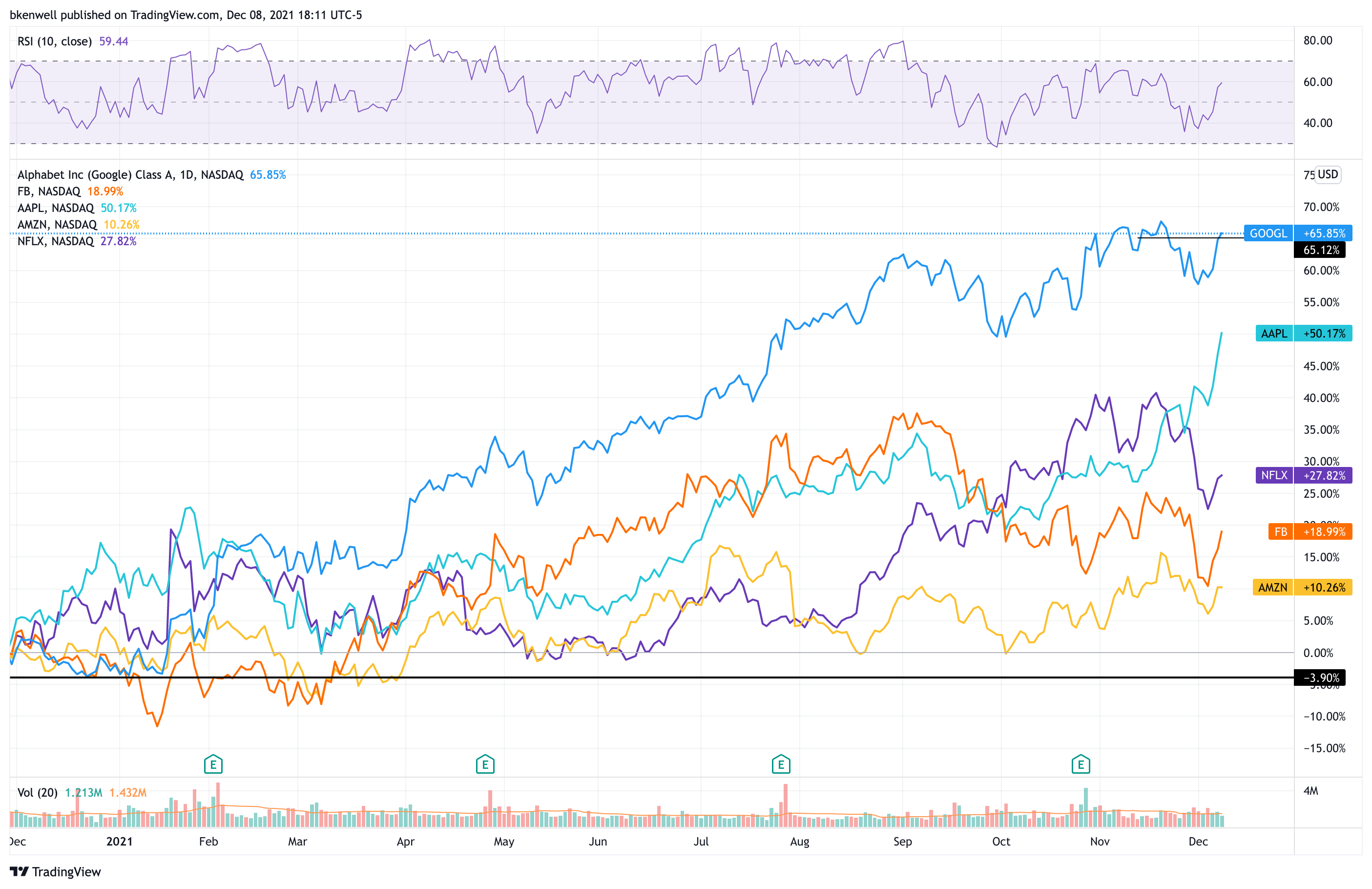

Despite the sluggish movement in Alphabet’s shares over the past month and the robust rally we’re seeing in Apple (NASDAQ:AAPL), GOOGL stock has been the best-performing FAANG of 2021.

Click to Enlarge

GOOGL stock is up 68.9% year to date and 64.4% over the past 12 months. Apple, the next best-performing FANNG stock over these periods, is up 34.2% and 45.4%, respectively.

As you can see, there is quite a bit of distance between the No. 1 and No. 2 performers. And while many investors tend to gravitate toward the more exciting FAANG holdings, there’s no denying GOOGL stock has been the clear leader of the pack.

Balance Sheet and Assets

At the end of the third quarter, the company boasted total assets of $347.4 billion. That includes total current assets of $184.1 billion and total cash and equivalents of $142 billion. All of these are at record highs, while total debt sits at less than $28.1 billion.

Alphabet’s balance sheet has become insanely powerful, even as Microsoft (NASDAQ:MSFT), Apple and Meta Platforms (NASDAQ:FB) are the ones that seem to get all the attention.

Beyond cash, Alphabet’s assets include the two most popular websites in the world: Google.com and YouTube.com. Think of them as the Boardwalk and Park Place of the Internet. These sites are almost unimaginably valuable and the biggest growth engines and profit drivers for the company.

Google has plenty of other assets as well, including its self-driving car project Waymo, the Nest line of smart home products, Waze satellite navigation software and Fitbit fitness products.

Growth

Mature tech names can often turn into value traps as growth slows. That’s far from the case with Alphabet, though. Despite its mammoth size, it still churns out solid growth numbers.

Analysts expect revenue to increase nearly 40% this year to $25.1 billion, followed by 16.8% growth in 2022. Earnings are expected to jump 85% to $108.52 per share this year. While earnings growth is also estimated to slow next year, analysts expect it to average 21% a year over the next five years.

Margins and Valuation

Speaking of earnings, on a trailing basis, Alphabet is generating 56.5% gross margins. That’s incredible given its revenue figure. It also boasts a record net profit margin of 29.5% on a trailing basis.

GOOGL stock is trading at 26 times next year’s earnings estimates. That may have some value investors printing this article off just to tear it up into tiny pieces. But consider that stocks like Procter & Gamble (NYSE:PG) and Clorox (NYSE:CLX) trade with similar valuations despite having inferior financials and much lower growth projections.

GOOGL Stock Chart

Click to Enlarge

When we look at the weekly chart, GOOGL stock has been on a slow, methodical drive higher off its March 2020 lows. True, the past few weeks have shown some consolidation. But, for the most part, anyone who has shorted this stock hasn’t done well.

The problem with taking profits in Alphabet creates the simple question of, “When do I get back in?”

A look at the chart above highlights this problem. It has been far more rewarding to buy the dips than to sell the tops. For now, that’s what I will keep doing, even if we get a healthy washout down to the $2,500 area.

With GOOGL stock trading just below $3,000 a share and 3% below its all-time high, it’s hard not to look toward the key extension levels next.

On the date of publication, Bret Kenwell did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell.