I have been a big Nvidia (NASDAQ:NVDA) bull for a long time now. All you have to do is look at a chart of NVDA stock over the past five years to see why. The company continues to dominate competitors and there is seemingly nothing to slow it down.

When NVDA stock dipped during the Covid-19 selloff and everyone was seemingly losing their collective minds, I called Nvidia “a steal” below $50 (on a split-adjusted basis). For what it’s worth, I don’t say that to gloat.

Trust me, that’s not my thing. I have been humbled far too many times that arrogance is now a superstition of mine. In any regard, I really bring that call up because, when things feel panicky, that’s when investors need to dial in and focus. Don’t get lost in the chaos. As a mentor of mine once said, when the market speeds up, slow down.

Currently down 35% from its all-time high, I think it’s safe to say things have officially sped up for NVDA stock.

When to Buy the Dip in NVDA Stock

Nvidia is a former relative strength monster, but when shares were up more than 160% on the year at the highs, it was clear that it would have to cool off at some point. That point is now. Shares are down four weeks in a row and in eight of the last nine weeks.

On Jan. 21, NVDA stock filled the gap from Oct. 26. With a bit more downside, though, we’ll start to hit some more meaningful levels. Specifically, that’s the weekly VWAP measure, then the 200-day and 50-week moving averages.

If NVDA stock hits the 200-day, it will be down about 37% from the highs. If it hits the 50-week near its present value, shares will be down roughly 40% from the high.

Click to Enlarge

If you love Nvidia and want some exposure, there are worse times to buy then after a 35% dip down toward the 200-day. However, if we get to the $195 to $200 area, I think that’s an area investors really need to consider adding some exposure.

Not only is the 50-week a notable breakout area on the chart (blue line), but it’s also near the fourth-quarter low.

While the markets could tumble into a bear market and NVDA stock lose 50% or more of its value, investors can bet on the long-term here. In the long run, this name will come back. It’s a matter of when, not if.

Going below $195 and failing to get back above that does open Nvidia up to more potential downside. But we can revisit NVDA stock if that becomes the situation.

Why to Buy the Dip in Nvidia

Okay, so we know where to buy the dip, but why do we want to do that? Frankly, because Nvidia is one of the best companies I have ever seen. I like Advanced Micro Devices (NASDAQ:AMD) and respect Intel (NASDAQ:INTC) — although I’m not attracted to the latter — but Nvidia dominates both.

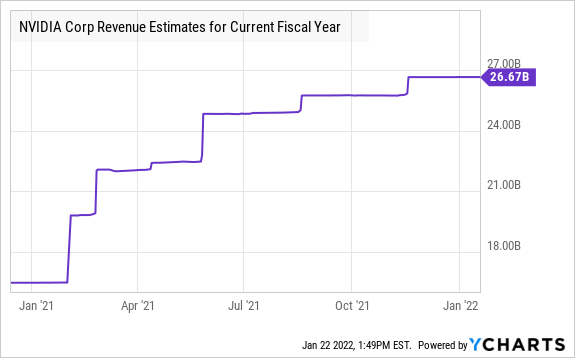

AMD has robust growth and, like Nvidia, has continued to stun analysts, leaving them far too conservative and caught flat-footed. But Nvidia’s margin profile versus AMD shows which company really has the pricing power. Analysts (finally) expect approximately 60% revenue growth this year for Nvidia, with estimates calling for $26.7 billion in sales.

Click to Enlarge

Allow me to show you something. The chart to the side shows how much consensus revenue estimates have come up over the last 12 months. Will they be short again this year?

Estimates for calendar 2022 (fiscal 2023) call for 19% growth. While that seems like a big deceleration from the prior year, it’s still pretty darn impressive. Further, estimates for fiscal-year 2024 and 2025 also call for 16% and 19% revenue growth, respectively.

It might be a little too aggressive, but can we make a bull case and say 20% annual revenue growth for the next three years?

Given Nvidia’s end-markets — autonomous driving (AD), artificial intelligence (AI) and machine learning, graphics, supercomputing, cloud-computing, datacenters, metaverse and more — that’s not so far-fetched in my view. And if that’s the case, it answers the why part of why investors should be long NVDA stock.

One Risk to Create More Chaos

All that said, the one risk that really jumps out to me here is Nvidia’s planned acquisition of Arm. The $40 billion deal is nothing to sneeze at. While it will cost a pretty penny for Nvidia, it will significantly bolster its list of customers and give it an impressive portfolio.

There’s incredible value there. However, if the deal falls through, I don’t know what will happen to NVDA stock.

If the market remains in a sell-the-news mood, a failed deal might smack the share price lower. Will it be down 40% at that point? Or even 50%, maybe? For all we know, NVDA will rally back to $300-plus and pop on the news. Who really knows?

I only mention this because headlines amid chaos can create sell-the-news reactions. I don’t think this is any different.

On the date of publication, Bret Kenwell held a long position in NVDA. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell.