There are many must-own stocks beyond the mega-caps that aren’t household names but have solid potential going forward. These stocks are using megatrends and tailwinds and have solid upside catalysts that could quickly propel them higher. Thus, I think it is worth having some exposure to these stocks, or you may miss out if these catalysts spark more excitement down the line.

What’s more, these stocks are not just about future potential – they are delivering strong financial results today. Even if the stars don’t fully align for them, I think these must-own stocks have enough cushion to still deliver gains.

Here are the seven must-own stocks:

CRISPR Therapeutics (CRSP)

CRISPR Therapeutics (NASDAQ:CRSP) is a company working to transform the treatment of serious health conditions through gene-editing research. With the recent approval of CASGEVY for sickle cell disease and beta-thalassemia in multiple countries and over 25 authorized treatment centers now active globally, I believe CRISPR is poised for significant growth. This tech can solve many diseases, and if the stars align, shareholders of CRSP could be in for enormous gains in the coming years.

The company’s pipeline includes treatments for cancer, autoimmune disorders, diabetes, and heart disease, with multiple data updates expected in the next year to year and a half. Notably, CRISPR’s proprietary nanoparticle delivery platform has enabled the addition of promising early research programs targeting uncontrolled high blood pressure and acute liver porphyria.

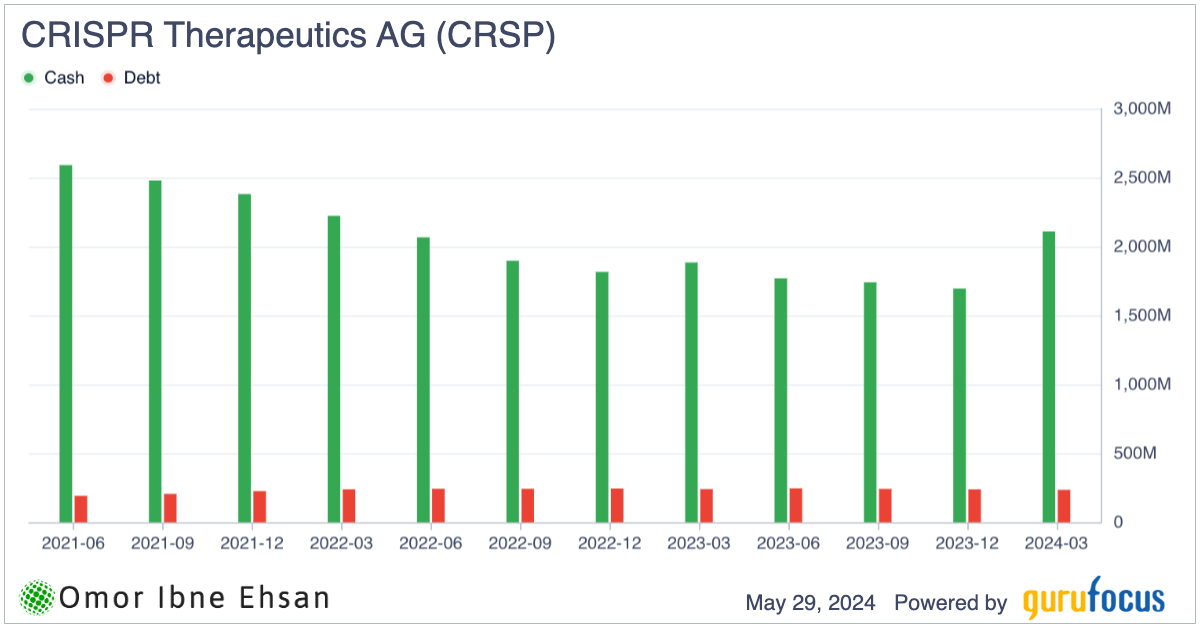

As of the end of March, the company maintains a strong balance sheet with approximately $2.1 billion available in cash, cash equivalents, and marketable securities.

Click to Enlarge

If analysts are right, this is more than enough to fund losses until it potentially turns profitable in 2027.

Rigetti Computing (RGTI)

Rigetti Computing (NASDAQ:RGTI) is working hard to develop new quantum computers and make quantum computing power available to everyone. Quantum computing could be the next big leap forward after artificial intelligence, with the potential to solve problems that are impossible now and create tremendous new opportunities. I’m interested to see how far Rigetti has come, with their 9-qubit Ankaa system recently achieving a very impressive 99.3% accuracy rate for operations involving two quantum bits in the first three months of this year. They expect their upcoming 84-qubit Ankaa 3 system will keep an accuracy of over 99% by the end of 2024, followed by a 336-qubit Lyra system.

Rigetti is also growing the part of its business that delivers quantum computer processors (QPUs) to customers on-site. Recently, they provided a Novera QPU to Horizon Quantum Computing in Singapore. This follows earlier work with major U.S. research labs like Fermilab and the Air Force Research Lab. In April, Rigetti launched a new partnership program to support the development of on-premises quantum computing around the world. While still in the early days, Rigetti’s technological progress and expanding customer relationships have made it a company with promising long-term potential for investors willing to accept some risk and uncertainty. With $3.1 million in quarterly revenue, up 39% from a year ago, Rigetti seems to be making steady strides and is certainly worth watching as this tech unfolds.

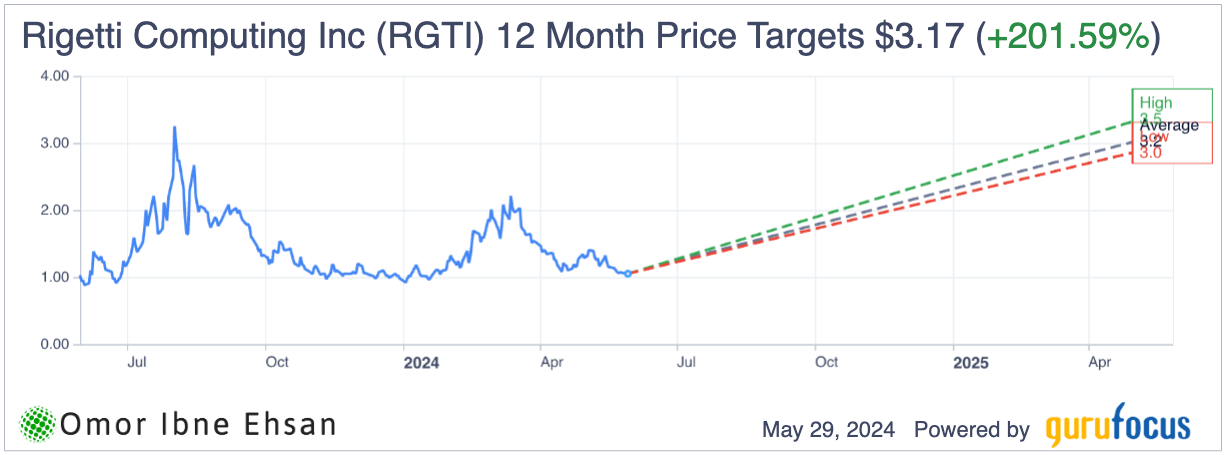

However, it is important to remember that cash could run out in a few years if it keeps losing money, but I think quantum computing breakthroughs could secure enough excitement by then to offset any cash crunch. Analysts also seem very bullish.

Click to Enlarge

Onto Innovation (ONTO)

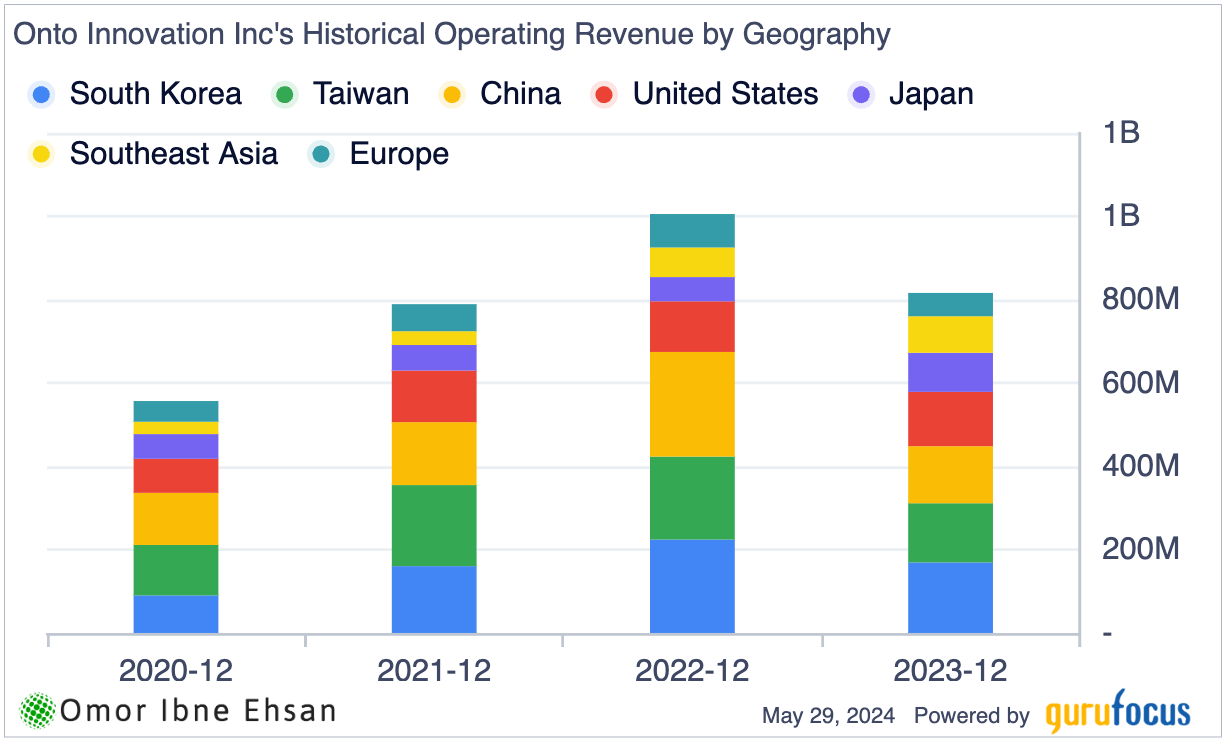

Onto Innovation (NYSE:ONTO) is a company that provides process control for creating computer chips. They work with the semiconductor industry, which makes the tiny circuits used in all kinds of electronic devices. Onto is poised to benefit from the huge demand for high-performance memory and circuitry packaging needed for artificial intelligence devices. This drove a solid 64% YOY increase in revenue from specialty chip packaging last quarter. The company is also one of the most diversified geographically.

Click to Enlarge

Onto’s Dragonfly inspection system seems to be a key strength, with revenue jumping 30% over the previous period to support packaging for AI chips. They are also innovating ways to identify new flaws in extremely thin chip wafers used for multi-chip module packaging. With 69% of earnings now coming from the fast-growing specialty device and advanced packaging markets, Onto appears well-equipped to benefit from the rising needs of AI adoption.

While the company may not yet be on every investor’s radar, I think Onto Innovation deserves a closer look, given its strong momentum and role in some of the most promising trends in chipmaking today. The future looks bright for this process control leader.

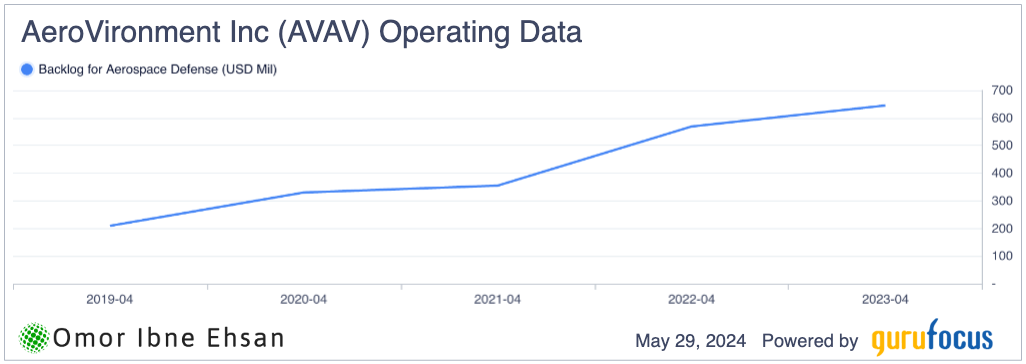

AeroVironment (AVAV)

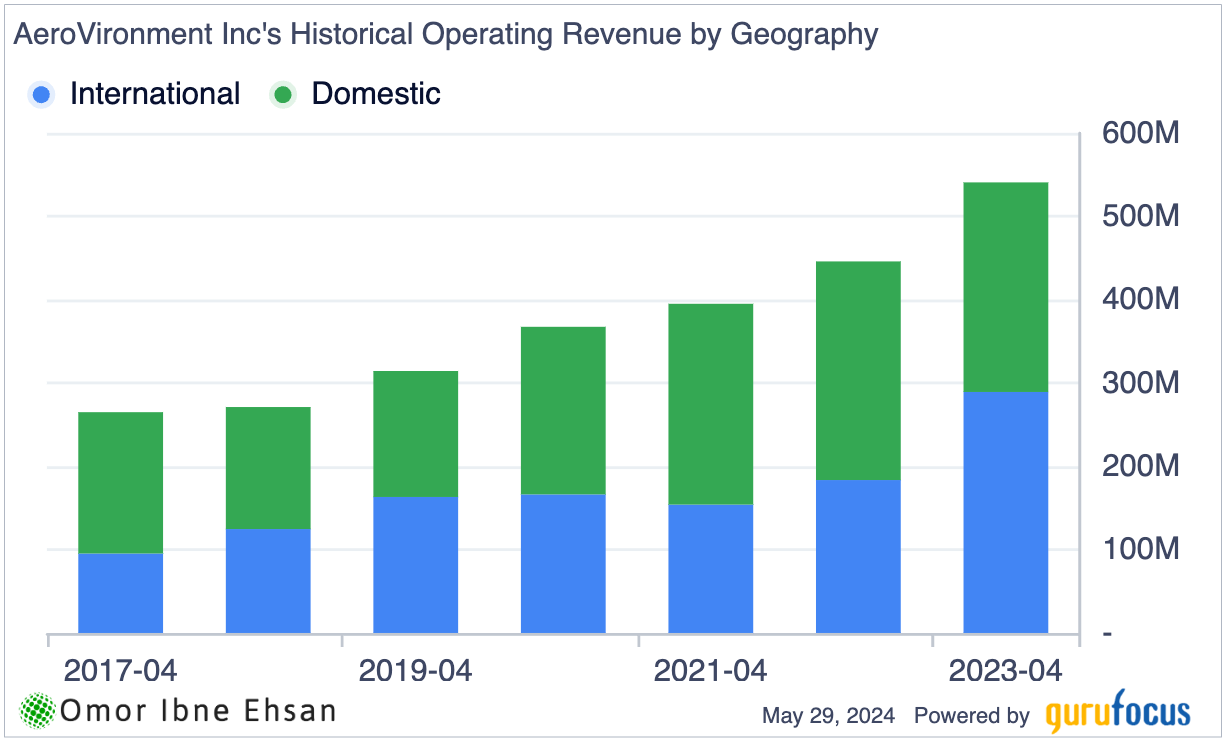

AeroVironment (NASDAQ:AVAV) has built a name for itself by designing and manufacturing unmanned aircraft for both military and commercial applications. The company seems poised to benefit tremendously from the huge uptick in demand from governments all over the world who are increasing their drone budgets. In Q3 of FY2024, AeroVironment’s revenue jumped almost 40% YOY to $187 million, largely driven by its Loitering Munition segment, which saw 140% growth in sales. Indeed, it is among the must-own stocks if you want to invest in defense.

Management is currently in deep discussions with the U.S. government regarding a large multi-year sole supplier contract for their Switchblade drone and is also engaging with over 20 interested countries hoping to purchase this platform. In fact, most of its sales are international.

Click to Enlarge

I believe AeroVironment’s cutting-edge drone technology makes them the first choice for the UAV revolution that is radically reshaping modern conflicts.

With backlog increasing 12% and investments in improving current solutions, AeroVironment appears well-prepared to meet the surging need.

Click to Enlarge

The stock remains a smart pick for investors wanting exposure to the booming drone industry trend, as analysts expect AeroVironment to deliver 31% revenue growth in fiscal 2024 based on rising global defense budgets earmarked for drones.

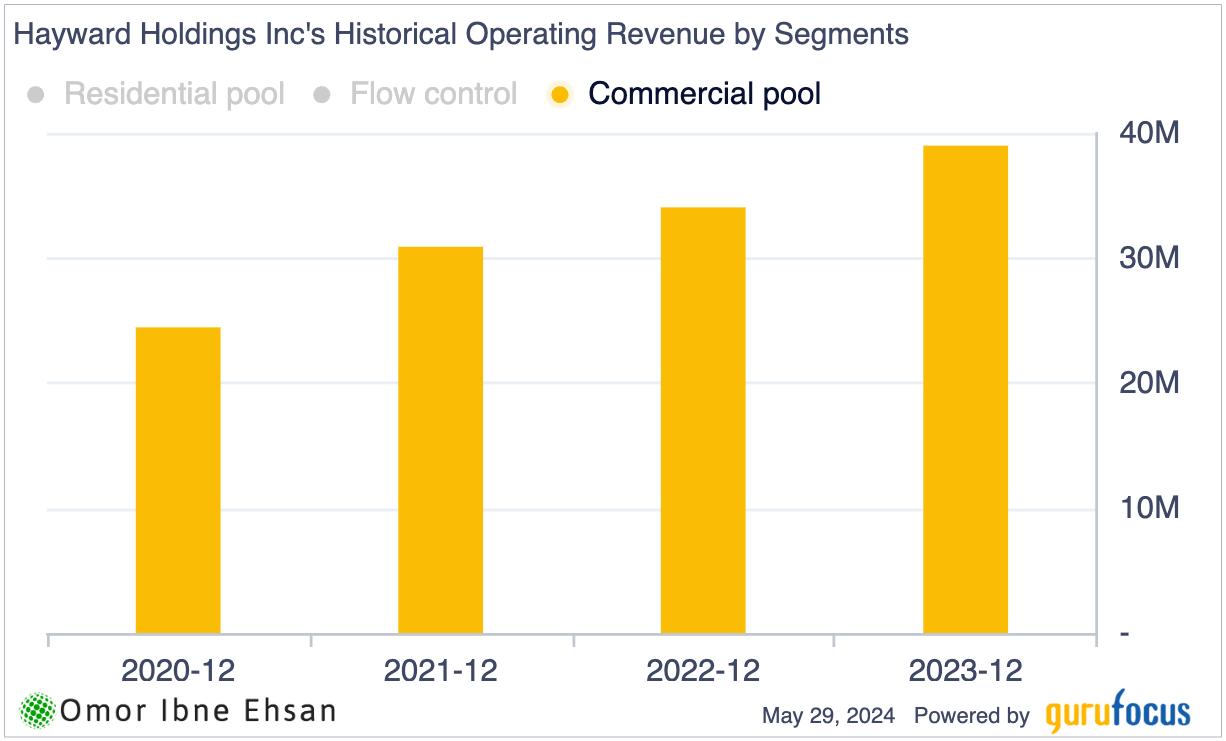

Hayward Holdings (HAYW)

Hayward Holding (NYSE:HAYW) makes swimming pool equipment and accessories. While not widely discussed on Wall Street, the company has a leading position in the growing commercial pool market. The commercial segment has continued to grow, whereas other segments have faced difficulties.

Click to Enlarge

According to Global Market Insights “Swimming Pools and Spas Market size was valued at over USD 2 billion in 2023 and is anticipated to grow at a CAGR of over 7.5% between 2024 & 2032.“

The company’s sales of commercial pool systems in North America surged double-digits in the first quarter, continuing a years-long trend fueled by more travel and hotel construction since the pandemic.

Despite broader economic challenges, Hayward delivered impressive first quarter results with revenue up 1%, gross profit margins expanding 260 basis points to a record 49.2%, and strong cash flow. Management is skillfully navigating near-term demand uncertainty by consolidating their European facilities while introducing new innovative products to gain more market share.

Now that the inventory replenishment period is mostly over and early customer discounts have expired, I expect Hayward’s price increases will have a fuller impact on financials in the coming periods. This pricing power combined with Hayward’s strengthening profits and cash generation makes the stock look undervalued at current price levels in my view. As leisure spending keeps rebounding, Hayward seems well-positioned to deliver gains for investors. As such, I think it is one of the best must-own stocks for the pool market exposure.

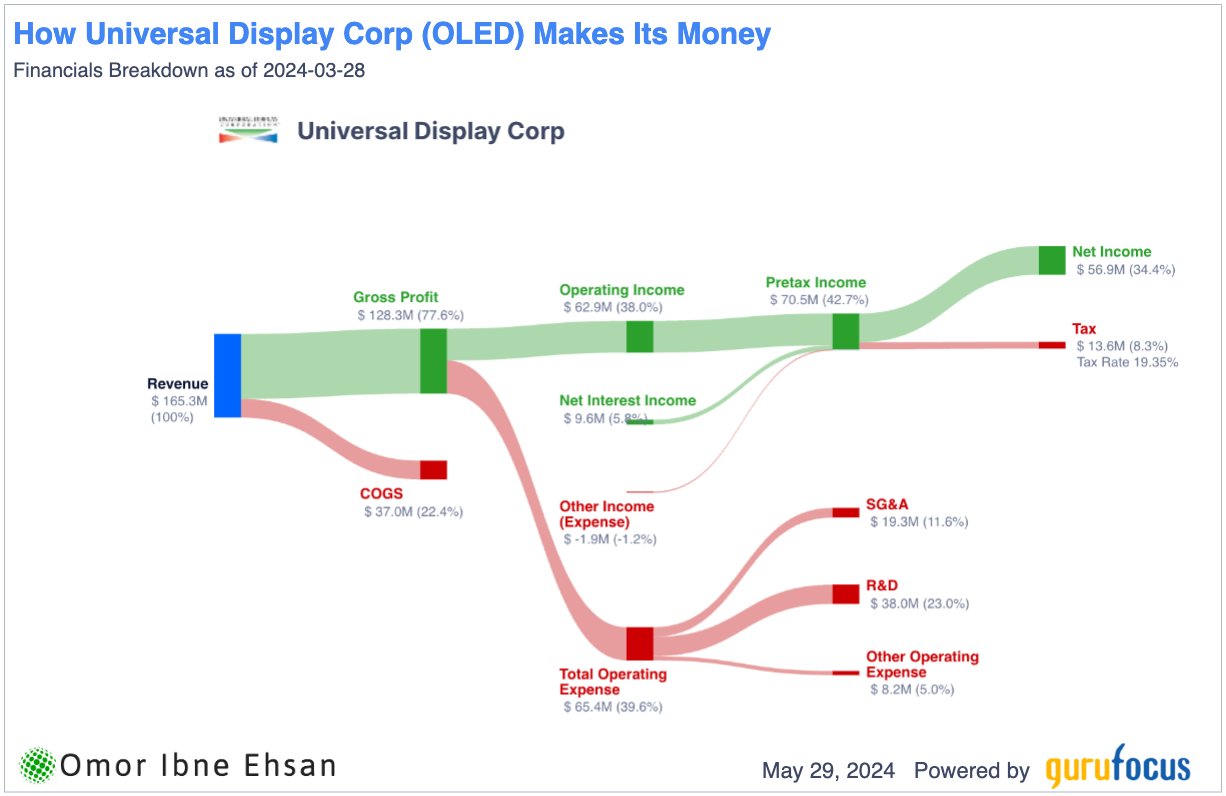

Universal Display Corporation (OLED)

Universal Display (NASDAQ:OLED) is a leading developer of OLED technologies for the display and lighting markets. Their numbers show that more and more industries are embracing OLED due to its superior performance and flexible design options. You may have recently heard about the new iPad M4 and its dual OLED technology. I think many more devices could start using it.

I believe the growing OLED information technology market presents a huge growth opportunity for Universal Display. Research shows OLED personal computer shipments are projected to skyrocket from 7.1 million units in 2023 to an incredible 17.2 million units in 2024 and to a staggering 72.3 million in 2028. This rapid expansion is fueled by major players like Samsung Display and BOE, which have significantly increased their OLED IT manufacturing capabilities. Thus, I think OLED is definitely one of the must-own stocks if you want to have exposure to this tech.

What’s more, the rising popularity of OLED in smartphones, foldable devices, and televisions further strengthens Universal Display’s long-term potential for success. As a top OLED innovator, they are well-positioned to benefit from these large shifts happening in the display world. The margins on its sales are excellent, too.

Click to Enlarge

With Universal Display increasing their projected full-year revenue guidance to an impressive $635-$675 million range, I am getting more and more optimistic about the company’s future potential.

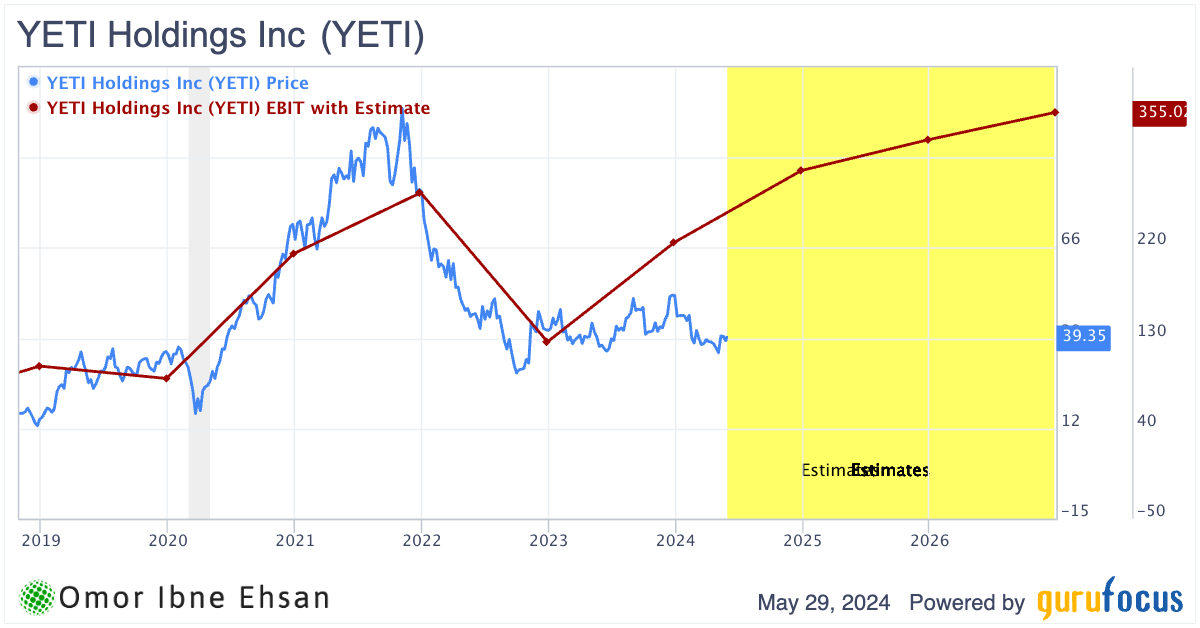

YETI Holdings (YETI)

YETI (NYSE:YETI) is a company that sells outdoor products. It posted solid Q1 results, with double-digit sales increases in all of its major categories like wholesale, direct-to-consumer, coolers and equipment, and drinkware. This positions them well to capitalize further during their key summer season.

I remain optimistic about the potential for expanding into new international markets – their overseas sales increased over 30% YOY and now comprise approximately 19% of total revenue. As interest in outdoor lifestyle products continues to grow globally, I believe this trend will serve as a tailwind for YETI’s business.

Encouragingly, YETI has successfully boosted profit margins substantially. Gross margins rose more than 450 basis points thanks to improved freight management. This translated to nearly a 440 basis point increase in adjusted operating margins as well.

YETI seems well-positioned for ongoing success in 2024.

Click to Enlarge

I maintain a bullish outlook as this company beat EPS estimates by 39% and has significant room for recovery in the coming years with earnings expansion.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.