Income investors should pay special attention to high-yield dividend stocks, especially if these stocks are safe and are trading at a valuation with little downside risk.

I think it is a good idea to sit on these discounted dividend stocks and let them compound rather than putting your money into some of the more overvalued names today. The turbulence has created opportunities to scoop up shares of quality companies at attractive prices and keep reinvesting.

Once interest rates come down and treasury rates fall, these dividend stocks are going to become very attractive. In the interim, you can prop up your dividend portfolio and make them compound much faster. If your average yield ends up even one or two percentage points higher, it can mean a lot in the long run – a potential game-changer for your retirement nest egg.

With that in mind, here are seven dividend stocks to look into:

USA Compression Partners (USAC)

USA Compression Partners (NYSE:USAC) is one of the largest natural gas compression companies in the U.S. Despite recent low gas prices and mild winters, the business has been growing and churning out profits nicely. Revenue grew over 16.3% YOY, hitting a new high of $229.3 million and beating analysts’ estimates. Adjusted EBITDA and distributable cash flow also set new records.

Management issued $1 billion in new 7.13% senior notes maturing in 2029; they were able to redeem some higher-interest debt and pay down their revolving credit line. This smart financial maneuvering earned USAC an upgraded credit rating from Moody’s. The stock currently yields 8.8%.

Admittedly, the distributable cash flow coverage ratio did dip slightly from last quarter to 1.41x. However, this makes sense when you consider that some preferred shareholders have converted to common stock.

Click to Enlarge

The dividends are stable, but I don’t expect much dividend growth here.

EPR Properties (EPR)

EPR Properties (NYSE:EPR) is a Kansas-based REIT that “that invests in amusement parks, movie theaters, ski resorts, and other entertainment properties.” REIT companies may not be your fancy, and I understand that since many people continue to be fearful about a Great Recession repeat. However, I do not think we are going to have a big real estate crash due to housing demand remaining strong and the labor market remaining solid.

In Q1, they reported EPS of 75 cents, which surpassed expectations by 13 cents, on total revenue of $167.23 million, which also exceeded forecasts.

What I find most encouraging is the strength of EPR’s coverage ratio from the past 12 months, which was 2.2 times. Even more impressive, the coverage ratio for their non-theater assets was 2.6 times. And their theater portfolio still had solid coverage of 1.7 times despite challenges at the box office. This gives me a lot of confidence that their cash flows will remain reliable.

They are having success expanding into new experience-focused categories beyond just theaters. Now, 93% of their $6.4 billion portfolio is experiential, and 99% is leased, so EPR has built an incredibly stable foundation.

While they’re wisely being selective now about new investments, it’s clear to me that EPR is positioning itself for long-term success.

Click to Enlarge

Dividend investors should feel very good about EPR’s future prospects as dividends payouts make a recovery. The dividend yield right now is 8.4%.

Main Street Capital (MAIN)

Main Street Capital (NYSE:MAIN) is one of the more under-the-radar dividend stocks that I think is worth holding. The yield is not as good as the two stocks I’ve discussed above, but 5.93% is still nothing to scoff at.

Results for the first quarter reinforce why this high-yield company remains one of my top “hold forever” dividend stocks. MAIN delivered an impressive annualized return on equity of 17.2% for the period while growing its net asset value to a new record high. A distributable net investment income of $1.05 per share provided substantial coverage of over 54% for the monthly dividends.

MAIN saw growth in both its lower middle market and private loan segments and saw “attractive opporeestunities” to continue this momentum.

Click to Enlarge

With MAIN boosting the quarterly dividend payouts consistently, I believe MAIN’s monthly dividends are positioned to keep increasing and growing for the long term.

Topaz Energy (TPZEF)

Topaz Energy (OTCMKTS:TPZEF) is another indirect energy play that invests in energy companies. It has been very consistent and has seen solid dividend growth over time. In Q4 2023, they achieved a royalty production of 19,600 barrels of oil equivalent, exceeding their own optimistic guidance for the year. They had a 10% annual production increase thanks to extensive drilling activities on their land by operating partners. They also have replaced over 100% of reserves at no cost to their own business.

In addition, Topaz’s infrastructure assets had operating margins of 95% while requiring minimal ongoing maintenance expenses. The company’s seventh dividend raise during that time to 32 cents per share reflects a substantial 60% growth since early 2020. Plus, with over $105 million in excess cash last year and a careful strategy for reinvesting profits, I believe Topaz is in an excellent position to continue providing reliable dividends well into the future.

Click to Enlarge

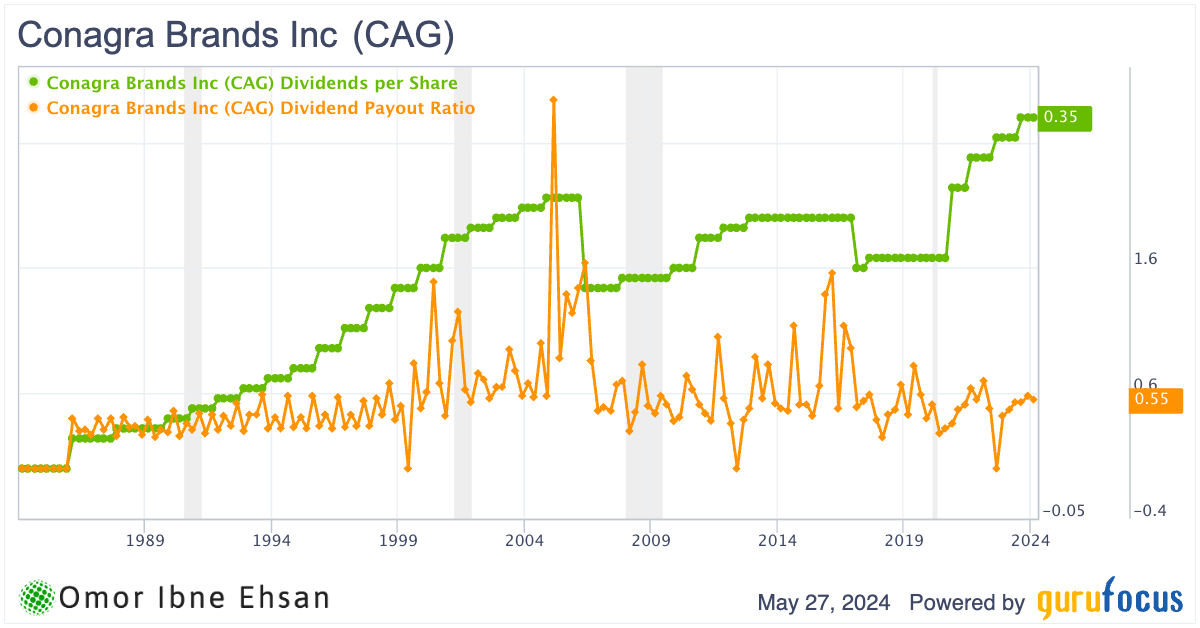

Conagra Brands (CAG)

Conagra’s (NYSE:CAG) stock did decline by 11.7% in the past year, but I see steady improvements. The stock is up 2.5% year-to-date. While overall volumes were still lower in the third quarter compared to last year, the seven percentage point sequential rise in frozen food volumes from the first quarter is encouraging.

It seems the company’s investments in frozen foods are starting to pay off, even if refrigerated products are creating some temporary noise due to pass-through deflation being reported. The strong pricing power seen in the Grocery and Snacks segments also bodes well, with product lines like tomatoes and canned meats bouncing back nicely.

I expect Conagra’s diversified portfolio will provide valuable stability during this uncertain macroeconomic climate. While it’s difficult to pinpoint exactly when volumes will start increasing again, the building of positive momentum is undeniable.

Click to Enlarge

The stock also comes with a dividend yield of 4.62% as of writing.

Enterprise Products Partners (EPD)

Enterprise Products Partners (NYSE:EPD) continues to be one of the most stable and consistent dividend stocks to buy right now. It is another energy play, but the stock is very insulated from volatility in natural gas and oil prices.

The midstream giant just reported another extremely solid quarter, with operating margins growing 7% over last year to reach $2.5 billion. The successful startup of new natural gas processing facilities in the Permian Basin region and the strong demand for energy exports fueled this growth.

EPD has tremendous cash generation ability, with cash available for distributions hitting $1.9 billion and providing 1.7 times coverage for the 5% distribution raise. Management is wisely retaining $786 million to reinvest back into the business, which should help drive future expansion.

Click to Enlarge

With a 7.3% yield, 27 straight years of raising distributions, and a business model as rock-solid and dependable as they come, EPD remains one of the safest high-yield stocks.

Verizon Communications (VZ)

It’s been a challenging few years for Verizon (NYSE:VZ) shareholders, but I’m cautiously optimistic things may start turning around for the telecom giant. While losing over 158,000 phone subscribers last quarter was disappointing, it does represent a significant improvement over previous years. Consumer wireless revenue also inched up 3.3%.

Most importantly, Verizon generated $2.7 billion in free cash flow during the period while growing adjusted EBITDA to $12.1 billion. That cash flow will be crucial for continuing to reward investors through dividend payments. The company’s myPlan offerings, including Netflix (NASDAQ:NFLX) and other perks, are helping drive continuing revenue streams from customers.

Cost-cutting efforts also appear to be gaining steam. If that trend holds, I wouldn’t be surprised to see free cash flow increase throughout the year. While the stock price has fallen considerably in recent times, I think we may be approaching a bottom. Getting Verizon’s high-yielding dividend at these lower share prices seems like a wise long-term strategy for income investors.

Click to Enlarge

The dividend yield is at 6.69% as of writing.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.