When most investors think of blue-chip stocks in today’s market, big tech giants immediately come to mind. These household names have been on an incredible run, with many minting new all-time highs. However, it is important to look deeper within the blue-chip space to uncover companies with outsized potential right now.

While everyone is focused on chasing the hot stocks of the moment, I believe some incredible opportunities are hiding in plain sight. There are several forgotten blue-chip stocks trading at massive discounts right now that could be poised for huge comebacks in the coming years.

Many of these household names have already bottomed out or are on the cusp of major inflections higher. And history shows that buying great but underappreciated companies before the market catches on is often a recipe for doubling your money (or doing even better). With that, let’s dive into these names.

Aflac (AFL)

Aflac (NYSE:AFL) is a rock-solid blue-chip company that doesn’t get the attention it deserves. The stock has delivered outstanding returns for shareholders over the years.

The company reported strong Q1 2024 results, with adjusted earnings per share growing 7.1% to $1.66. The company’s U.S. segment was particularly impressive, with a 3.3% increase in net earned premiums and an 80 basis point improvement in persistency to 78.7%.

Several mega trends bode well for Aflac’s future. Rising health care costs drive demand for Aflac’s supplemental insurance. Moreover, companies are increasingly focusing on employee wellness and robust benefits to attract and retain talent.

I expect Aflac to continue its track record of steady growth and profitability. The stock has significant upside potential if the company executes as well as it has historically. Its dividend yield currently sits at 2.14%.

Dollar General (DG)

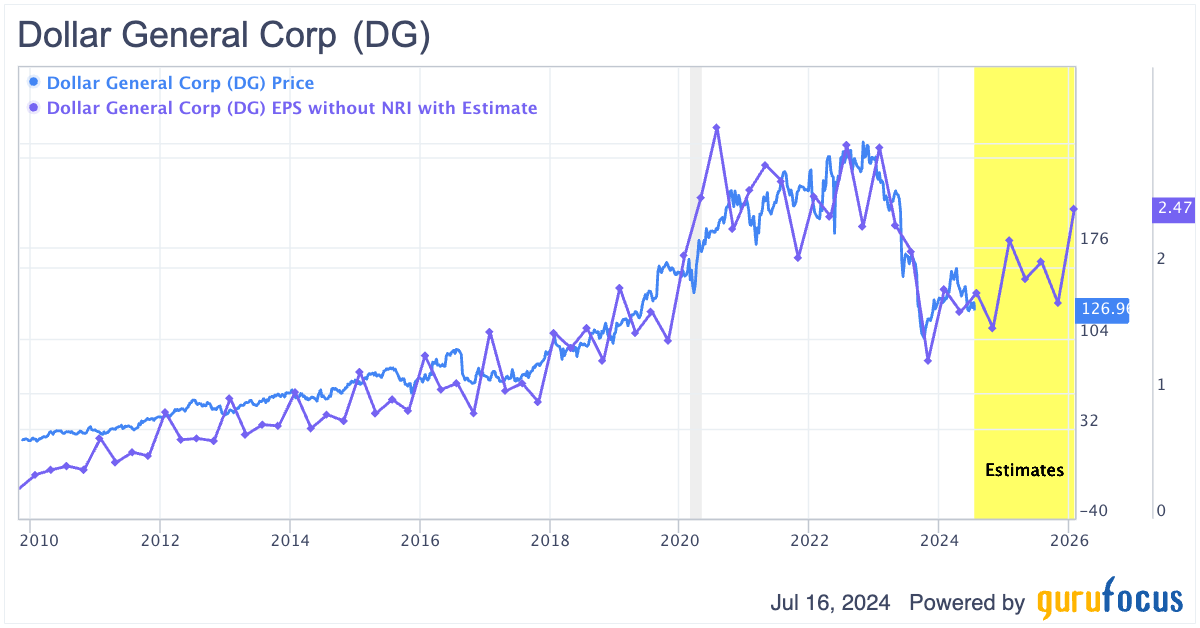

Dollar General (NYSE:DG) is America’s largest discount retailer. The stock has taken a hit recently, declining significantly from its peak as the retail sector faces challenges. However, I believe DG stock is poised for a rebound.

Dollar General remains a highly profitable company, despite temporary setbacks. In Q1 2024, the company’s net sales increased 6.1% to $9.9 billion. This was driven by strong growth in consumer traffic. Now, operating profit did decrease by 26.3% to $546 million. However, analysts expect profits to start climbing back to normalized levels soon.

Click to Enlarge

The company reiterated its full-year guidance, anticipating net sales growth in the range of 6%-6.7%, same-store sales growth of 2%-2.7%, and earnings per share of $6.80-$7.55.

Dollar General is now expanding its fresh produce offerings to 5,000 stores. That’s a convenient strategy, considering its competitor Dollar Tree (NASDAQ:DLTR) has closed 15% of its locations. Now, Dollar General plans to capitalize on this opportunity by opening 800 new stores in 2024.

In my opinion, you can rarely go wrong buying a profitable, blue-chip household name at a discount. The stock’s 1.86% dividend yield is the icing on the cake.

Whirlpool (WHR)

Whirlpool Corporation (NYSE:WHR) is a well-known home appliance maker that may be overlooked due to its business model alone. This once-overlooked blue-chip stock has begun to rally after a 65% drop from its peak. No one can say if this short-term rally will hold. But I believe significant long-term upside potential remains for this gem.

Whirlpool has an $8.4 billion debt load, and high interest rates have caused a lot of pain for investors as many focus on balance sheets of top companies.

However, the company has about $1.6 billion in cash. This cash should keep the lights on as the storm passes. Moreover, expected rate cuts in the next few months could help accelerate Whirlpool’s sharp turnaround.

Whirlpool recently cut costs by $800 million in 2023 and plans to cut another $300-400 million of costs in 2024. Notably, WHR stock also gained more than 1% market share in North America in the fourth quarter of 2023. I’m pretty optimistic on this overlooked blue-chip stock for these reasons and more!

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.