The steep selling in U.S. markets has felt relentless in the first half, and even the best Asian stocks got caught in the tide.

Despite already falling into a bear market territory, the U.S. indices still trade above fair value. When considering interest rates have further risen as the Federal Reserve battles rampant inflation, investors should diversify geographically. And the best Asian stocks, already at a deep discount, also have strong growth prospects ahead.

Worldwide, all but one of the central banks are raising interest rates. China’s central bank is the exception. This suggests that the country is willing to continue an accommodating monetary policy. It wants to stimulate economic growth while the world tightens credit conditions.

Click to Enlarge

Technology stocks have the best prospects in Asia. In China, Alibaba (NYSE:BABA) is among the most widely followed e-commerce firms. JD.com (NASDAQ:JD) is a solidly run online retail firm, too. In the stock trading segment, Hong Kong-based Futu Holdings (NASDAQ:FUTU) is a potentially growing firm. In Singapore, the online retailer and gaming firm Sea (NYSE:SE) is popular.

In South Korea, Coupang’s (NYSE:CPNG) e-commerce business is expanding into food delivery, while microblogging platform Weibo (NASDAQ:WB) and video sharing company Bilibili (NASDAQ:BILI) is focused on a young and growing audience.

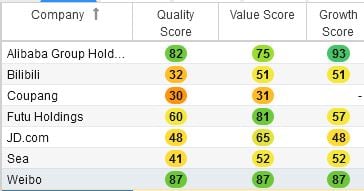

In the table above, Weibo and Alibaba score the best. According to Stock Rover, a quantitative scoring site, Alibaba has the best growth prospects. Conversely, Sea, Bilibili, and Coupang have scores that could improve.

But their prospects to make those improvements are what get them on this list of the best Asian stocks.

| BABA | Alibaba | $102.40 |

| BILI | Bilibili | $22.88 |

| CPNG | Coupang | $15.80 |

| FUTU | Futu Holdings | $45.66 |

| JD | JD.com | $60.26 |

| SE | Sea | $69.15 |

| WB | $19.31 |

Alibaba Group Holding (BABA)

After a lengthy span when regulators were unwilling to approve new mobile games as the government heightened its scrutiny against gaming firms, China has finally approved 60 domestic games. This is a turning point. Investors reacted by buying shares of Alibaba, which has a gaming segment.

In the fourth quarter, Alibaba posted a 9% growth in revenue, to $32.19 billion. Its business benefited from a 29% year-over-year growth in the local consumer services unit. The company added 28.3 million annual active customers, to 1.31 billion users. The company reversed its losses and posted income from operations of $11 billion.

During the Covid lockdown in March and April, consumer demands changed. People stocked up on necessities by buying in bulk. Alibaba offered on-demand and on-time delivery, even for bulk purchases, to customers during that period. As demand for bulk products increases, investors should expect revenue per customer to grow.

In the second half of the year, Alibaba needs a sustainable and robust supply chain. If it gets its logistics in place, its merchants may meet the growing consumption rebound.

Bilibili (BILI)

Bilibili is a video service provider for a young audience in China. The company posted first-quarter losses of 66 cents a share. Revenue rose by 30% Y/Y to $797.3 million.

Investors should consider BILI stock because it’s growing its monthly active users. For example, MAU topped 293.6 million, up by 31% Y/Y.

After China lifted its Covid-related lockdown, Shanghai staff who worked at home returned to work. This will help the company renew its momentum in growing its e-commerce and advertising.

During the lockdown, its advertising business suffered. Advertisers put their spending plans on hold. With the disruption over, Shanghai customers should slowly renew their willingness to spend. They will also increase their reliance on delivery services.

BILI stock may underperform as the lockdown dragged into the current quarter. But after that, the company will monetize its growing MAU and DAU. For example, paying customers reached a record high of 95 minutes spent on the platform.

Coupang (CPNG)

Coupang (NYSE:CPNG) is not yet profitable. To get there, it needs to expand its market, grows revenue, and increase operating margins.

In the last quarter, Coupang posted revenue growth of 32% YOY. Chief Executive Officer Bon Kim is confident that the company will grow its e-commerce revenue faster than the market. For example, its active customers grew to over 18 million, up 13% Y/Y. CEO Kim attributed the growth to an unmatched customer experience driving deeper engagement.

Coupang improved its operating efficiency, particularly around process and technology. In the next few years, EBITDA margins will expand beyond the 7% to 10% range. In addition, it will grow Coupang WOW, a subscription service similar to that of Amazon (NASDAQ:AMZN) Prime.

Coupang will expand its Eats offering, a food delivery service. After improving on operating leverage, the next phase of Eats is expanding offerings. Still, it will not rely heavily on coupons and discounts to drive growth.

Futu Holdings (FUTU)

Futu Holdings operates a digitized brokerage and wealth management platform. The company looks attractive as it gains market share from weaker, smaller brokers.

The Federal Reserve’s rate hikes will increase Futu’s net interest income. Clients are sitting on idle cash that will earn Futu risk-free earnings.

Futu’s expansion in the U.S. could also disrupt the brokerage industry. Companies like Robinhood (NASDAQ:HOOD) have clients with lower assets managed. There’s an opportunity there for Futu.

In the last quarter, Futu said that it benefited from improving the quality and quantity of clients in Singapore. In the U.S., its client count grew. Since the average asset size fell, Futu will focus on raising client quality. The company will modify its client incentive program to attract clients with more assets. This should lead to more reliable quarterly profits.

Futu is educating its clients on how to trade on lower-risk assets. For example, it does not encourage clients to trade derivatives. Despite that, derivative trading accounted for 30% of Futu’s commission income.

Expect the company’s healthy research and development spending to increase the product quality and attract better clients

JD.com (JD)

JD.com is dealing with the Covid lockdown. It understood the impact of the more transmissible Omicron variant on its business. In the first outbreak two years ago, e-commerce and internet activity rose. This time, the lockdown and supply chain issues hurt JD’s warehouse and delivery stations.

JD adjusted for increased fulfillment times. Still, it resulted in a higher rate of order cancellations. In April, this rate increased, though it did improve in May. Levels are still high but as they normalize, JD stock should react favorably.

At 618, an annual retail event, JD proactively participated in a grand promotion. While growth was slower than before, it was still up 10% leading into the event. Investors should expect the company to post stronger quarterly results.

For the rest of the year, JD’s margins should expand. The company adjusted its investment levels. As the macro environment improves, JD will manage its cash flow and profitability. It will invest in areas that improve its operations.

Sea (SE)

Sea (NYSE:SE) runs Shopee and SeaMoney. In the first quarter, the company highlighted efficiency gains due to scale. If it can keep that up, it will capture market share, strengthen its position and benefit from operating leverage. For example, it achieved synergies for its two businesses in Southeast Asia and Taiwan.

In the gaming segment, Garena underperformed as growth slowed post-Covid. Sea offset the weakness by improving its user engagement in its popular game Free Fire. Monthly user trends are stabilizing. In the long-term, investors will need to monitor the user momentum without the benefit of the Covid-related lockdown.

Increasing user engagement is Sea’s priority. It is currently focused on increasing the longevity of Free Fire by adding more diversified content including more game modes. Users will also get user-generated content (UGC) tools.

In the first quarter, Sea posted an 80-cent-per-share loss. Revenue grew by 64.4% to $2.9 billion. SE stock is unattractive to cautious investors. Investors may consider a position from here before the company reaches profitability.

Weibo (WB)

Weibo is a Chinese microblogging website. If investors are willing to take the risk of Weibo delisting from the U.S. exchange, WB stock could be one of the best Asian stock to buy.

In the first quarter, Weibo posted non-GAAP earnings per share of 56 cents. Revenue grew by 5.6% YOY to $484.6 million. The company added 51 million users. It had 582 million monthly active users in March 2022, and 95% of its users are on mobile.

Weibo’s recovery depends on China loosening its lockdown. When that happens, Weibo’s uptrend will accelerate. In addition, the lockdown did not hurt the gaming industry. This suggests that when Weibo gets gaming approvals, its business will expand.

Half of Weibo’s business focuses on luxury products, automobiles, and fast-moving consumer goods (FMCG). During the lockdown, Beijing canceled the Beijing Auto Show. Weibo will adjust for future events by launching new models online and increasing its budget to promote the online event.

With Covid-19 better contained, Weibo stands to rebound well in future quarters.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.