Editor’s note: “Why Wall Street’s AI Bet May Be Dead Wrong” was previously published in July 2025. It has since been updated to include the most relevant information available.

Everyone’s watching the wrong AI boom.

While Wall Street and Silicon Valley obsess over ChatGPT-5 – or how many exaflops xAI is hoarding – they’re missing the real earthquake.

It’s already rumbling beneath the surface. And it’s about to crack the foundations of the AI world and reorder the entire semiconductor supply chain.

That quake? The silent, seismic shift from Large Language Models (LLMs) to Small Language Models (SLMs).

And it’s not theoretical. It’s happening now.

AI is leaving the cloud. Crawling off the server racks. And stepping into the physical world.

Welcome to the Age of Physical AI

If the past five years of AI were about massive brains in the cloud that could pass the bar exam and write poetry, the next five will be about billions of tiny, embedded brains powering real-world machines.

Cleaning your house. Running your car. Cooking your dinner. Whispering insights through your glasses.

This is AI going physical. And when that happens, everything changes.

Because physical AI can’t rely on 500-watt datacenter GPUs.

It can’t wait 300 milliseconds for a round trip to a hyperscaler.

It needs to be:

- Always on

- Instantaneous

- Battery-powered

- Offline-capable

- Private

- Cheap

And that means it can’t run GPT-5.

It needs SLMs: compact, fine-tuned, hyper-efficient models built for mobile-class hardware.

SLMs aren’t backup singers to LLMs.

In the world of edge AI, they’re the headliners.

The new AI revolution won’t be televised.

It’ll be embedded. Everywhere.

The SLM Invasion Has Already Begun

You may not have noticed it yet – because the companies deploying small language models are not bragging about billions of parameters or trillion-token training sets.

They are shipping products.

Apple’s (AAPL) upgraded Siri? Runs on an on-device SLM.

Meta’s (META) Orion smart glasses? Powered by locally deployed SLMs.

Tesla’s (TSLA) Optimus robot? Almost certainly driven by an ensemble of SLMs trained on narrow tasks like folding laundry and opening doors.

This is not a niche trend.

It is the beginning of the great decentralization of artificial intelligence – from monolithic, cloud-based compute models to lightweight, distributed intelligence at the edge.

If large language models were the mainframe era of AI, SLMs are the smartphone revolution. And just like in 2007, most incumbents do not see the freight train coming.

To be clear: LLMs are remarkable – but they are not scalable.

You cannot put a 70-billion-parameter model in a toaster. You cannot run GPT-5 on a drone.

SLMs, by contrast, are purpose-built for the edge. They:

- Operate at sub-100 millisecond latency on mobile-class chips

- Fit into just a few gigabytes of RAM

- Deliver reliable performance for 90% of AI agent tasks (instruction following, tool use, commonsense reasoning)

- Can be fine-tuned at low cost for narrow applications

They are not omniscient.

They are the blue-collar AI that gets the job done.

And in a world that needs AI agents in cars, robots, glasses, appliances, manufacturing lines, kiosks, and wearables – reliability and cost will beat generality and elegance every single time.

The Investment Implications: GPU Utopia Cracks

Now here is where it gets interesting.

For the past two years, the core AI investment thesis has been simple:

“Buy Nvidia (NVDA) and anything tied to GPUs – because large language models are eating the world.”

That thesis held up. Until now.

If small language models begin to dominate AI deployment, the model starts to break down.

Why?

Because SLMs do not require data centers. They do not need $30,000 accelerators. They do not consume 50 megawatts of cooling. They do not even rely on OpenAI’s API.

All they need is efficient edge compute, a battery, and a purpose.

And that changes everything.

The center of gravity in AI shifts – from cloud-based GPUs and training infrastructure to edge silicon, local inference, and deployment tooling.

This does not mean Nvidia loses.

It means the next trillion dollars in value could accrue somewhere else.

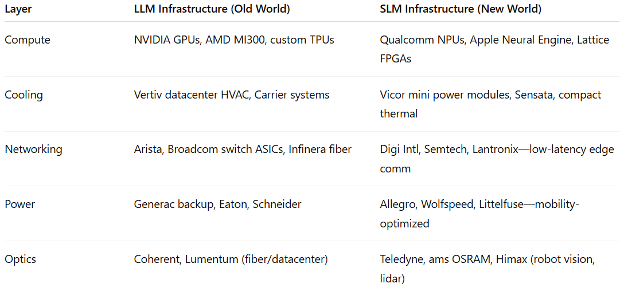

The New Infrastructure Stack for Physical AI

Let’s get specific. The LLM world runs on one kind of infrastructure. The SLM world needs a completely different stack.

Critically, SLMs are inexpensive to replicate and do not require constant API calls to function.

That is a direct threat to the rent-seeking software-as-a-service (SaaS) AI model—but a powerful tailwind for device original equipment manufacturers (OEMs) and edge compute firms.

And based on the chart above, you can start to see how this tectonic shift may play out across public markets.

Qualcomm (QCOM) looks like a major winner. Its Snapdragon AI platform already runs many SLMs. It is the ARM of the edge AI world.

Lattice Semiconductor (LSCC) could also benefit. The company produces tiny FPGAs—ideal for AI logic in low-power robots and embedded sensors.

Ambarella (AMBA) is another potential standout, with its AI vision SoCs used in robotics, surveillance, and autonomous vehicles.

Among the Magnificent Seven, Apple appears especially well positioned. Its Neural Engine may be the most widely deployed small AI chip on the planet.

Vicor (VICR) also deserves mention. It produces power modules optimized for tight thermal and power envelopes—key to edge AI systems.

On the other side of the ledger, several beloved AI winners could find themselves on the wrong side of this transition.

Super Micro (SMCI) may be vulnerable if inference shifts away from data centers and server demand softens.

Arista Networks (ANET) could face pressure as data center networking becomes less critical.

Vertiv (VRT) might see growth flatten if hyperscale HVAC demand slows.

Generac (GNRC) may be exposed to declining demand for backup power if the SLM trend reduces reliance on centralized compute.

This is how paradigm shifts happen.

Not overnight – but faster than most incumbents expect. And with billions in capital rotation along the way.

Build a Portfolio for the SLM Age

If you believe AI is moving from “text prediction in the cloud” to physical intelligence in the world, then your portfolio needs to reflect that.

Instead of chasing the same three AI megacaps everyone owns, focus on:

- Edge chipmakers

- Embedded inference specialists

- Optics and sensing providers

- Power management innovators

- Robotics component suppliers

The mega-cap GPU trade isn’t dead. But it’s not the only game in town anymore.

The Final Word

The reason this story isn’t everywhere yet is simple: it does not sound flashy.

“Small models” do not make headlines. But they are what will drive profits—because they are what will scale artificial intelligence to a trillion devices and embed it into the everyday fabric of human life.

SLMs aren’t just a more efficient alternative to giant cloud-based AI. They’re the key to taking artificial intelligence off the server racks and into the real world.

These models can run on local hardware and require less power, less latency, and less bandwidth – making them ideal for use in embedded systems and autonomous machines.

In short: SLMs unlock the era of “physical AI.” That includes everything from smart factories to warehouse bots to humanoid machines like Tesla’s Optimus.

And behind the scenes, an entire ecosystem of suppliers is rising to meet the hardware demands of this shift: companies making the sensors, edge chips, power modules, actuators, and embedded inference engines that bring AI to life.

To best position your portfolio for the next leap in this megatrend, don’t just look at the robots. Look at the components powering them.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.

P.S. You can stay up to speed with Luke’s latest market analysis by reading our Daily Notes! Check out the latest issue on your Innovation Investor or Early Stage Investor subscriber site. Questions or comments about this issue? Drop us a line at langofeedback@investorplace.com.