Facebook (NASDAQ:FB) reported its first-quarter earnings results on Wednesday, April 29 after the close. With a 6.2% rally in the regular session, it was understandable for investors to be worried about a sell-off. However, FB stock ripped higher by almost 10% in after-hours trading.

That’s a clear sign that investors had priced in too much of a slowdown. The quarter wasn’t great based on expectations from three months ago. But based on current realities, the quarter was a success.

We have been steadfast on FB stock, calling it a buy on the dip. Part of the reason is its superior balance sheet, another part is the immense profitability of its business model. Let’s take a closer look.

Facebook Earnings

Earnings of $1.71 per share beat analyst expectations by a penny. Revenue of $17.74 billion jumped 17.6% year-over-year and topped estimates by more than $500 million.

Like I said, investors previously priced in too much negativity, even though FB stock has been rebounding hard off the lows.

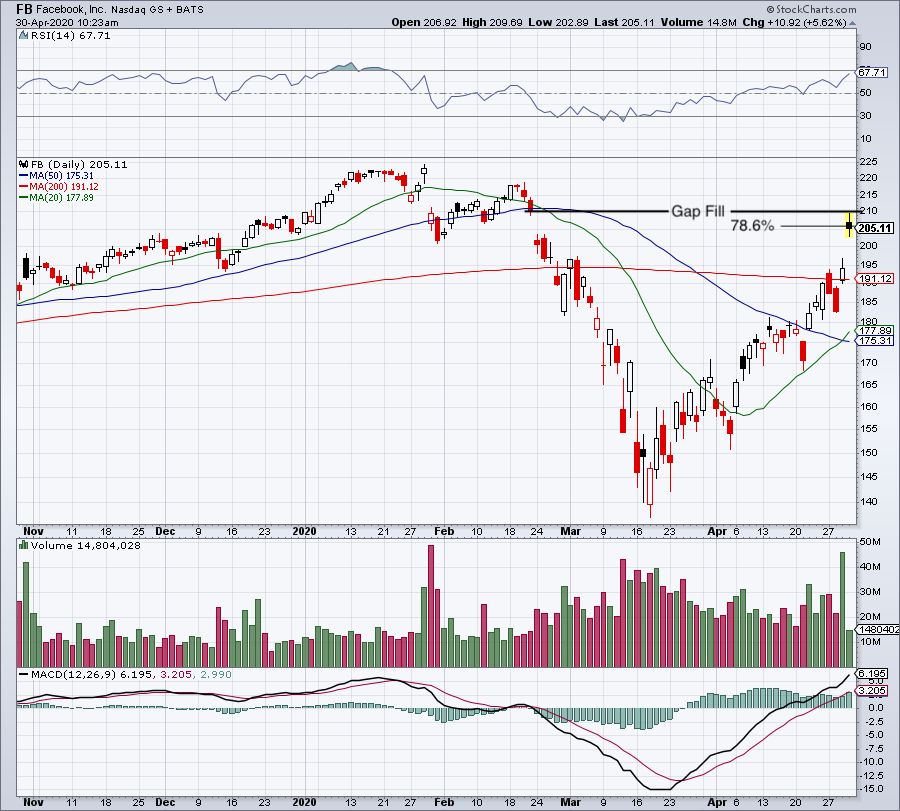

Click to Enlarge

Before the after-hours post-earnings rally, Facebook shares were up almost 42% from the lows. With the rally, shares have retraced about 80% of the losses they suffered during the novel coronavirus selloff back in March. It also sends FB back to its February gap down near $210 (see chart).

A further rally from here may be difficult, but at least we know what’s going on at the company. Daily active users (DAUs) grew 11% to 1.73 billion and beat estimates of 1.7 billion. Monthly active users (MAUs) made a similar move. They grew 10% to 2.6 billion and beat estimates of 2.55 billion.

We’re seeing strength across the board in social media user growth. That’s as we’ve now heard updates from Snap (NYSE:SNAP), Twitter (NYSE:TWTR) and

Pinterest (NYSE:PINS).

While user growth and engagement both trend higher, the concern has been digital advertising. After all, advertising is the driving force behind Facebook and many other online mediums. So how does that industry look?

Hope for the Best, Plan for the Worst

With Facebook and Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) both spiking on earnings, investors are starting to wonder if concerns over the digital advertising market are overblown.

Sure, ad spend is down as marketing budgets shrink. But if Google and Facebook are fine — at least, based on their earnings — then how bad can it really be? Alphabet CEO Sundar Pichai said:

“Performance was strong during the first two months of the quarter, but then in March we experienced a significant slowdown in ad revenues. The timing of the slowdown correlated to the locations and sectors impacted by the virus and related shutdown orders.”

From CFO Ruth Porat:

“Although we have seen some very early signs of recovery and commercial search behavior by users, it is not clear how durable or monetizable this behavior will be…As of today, we anticipate that the second quarter will be a difficult one for our advertising business.”

While Porat didn’t say it word for word, she effectively said that the company is still cautious going forward, but for now, there’s stabilization in the ad business. That gels with what Facebook CFO David Wehner said on the company’s conference call: “After an initial steep decrease in ad revenue in March, we have seen signs of stability reflected in the first three weeks of April.”

However, he also said (emphasis added):

“We are understandably cautious given that most economists are forecasting a global GDP contraction in Q2, which if history were a guide, would suggest the potential for an even more severe advertising industry contraction.”

The end result is a cautious management team who is prepared for darker times but is hoping for brighter days. So far, the numbers reflect the latter, although a worsening economic situation could bring the former into play.

Bottom Line on FB Stock

At the end of the day we have a company that still has solid growth, although the current quarter faces challenges. Unlike Q1, which had two strong months before a sharp decline began, Facebook enters Q2 amid low demand.

The hope is that we’re near a bottom in advertising and that by the end of Q2 on June 30th, Facebook, Google and others have seen a notable uptick in advertising demand. That will increase confidence among management and thus, confidence among investors.

After such a strong run, let’s see if we get a dip in FB stock over the next month or so. If so, it may be a buying opportunity for those that missed the first dip in Facebook.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.