Wayfair (NYSE:W) has been on fire this year. Shares are up 123% so far in 2020 and are up more than eight-fold from the March lows. This rally has been bananas, but can it keep going? Wayfair stock is ideally situated in the e-commerce space at a time where online sales are booming.

When the novel coronavirus began sweeping across the world, it decimated many companies and hurt most business. For a few companies though, the coronavirus actually drove demand.

Think of companies like Netflix (NASDAQ:NFLX), Shopify (NASDAQ:SHOP), Amazon (NASDAQ:AMZN) and — you guessed it — Wayfair.

As consumers were sitting at home, they weren’t sitting still. They were busy ordering new items online and looking at digital forms of entertainment. Wayfair may not offer much for the latter, but when it comes to online sales, it has a role to play. With coronavirus cases on the rise again, can Wayfair stock continue higher?

Catalysts for Wayfair Stock

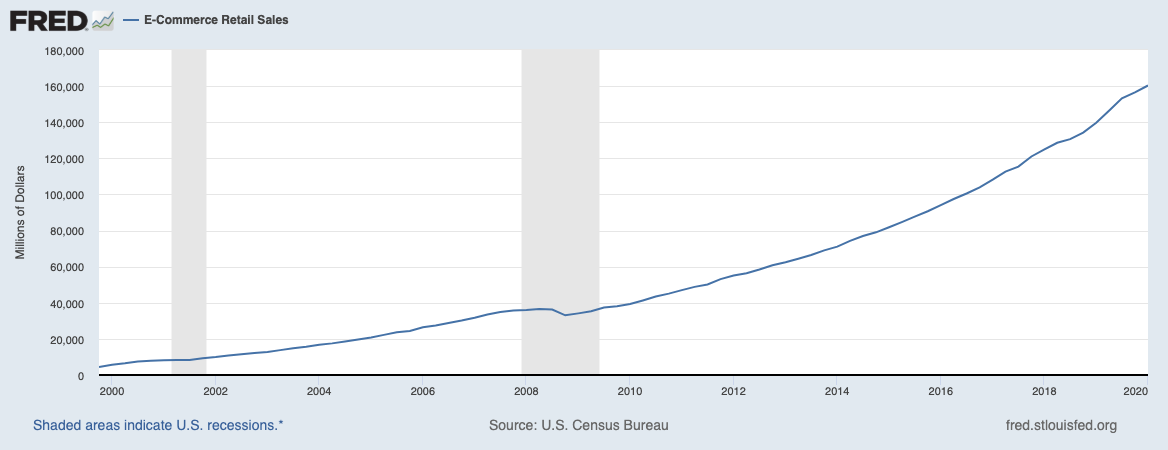

As we mentioned above, increasing coronavirus cases only increases the odds that consumers will turn to online sales. But this trend is nothing new. Consumers have been turning to e-commerce for years now. There’s a reason why companies have been putting more focus into online operations, and that’s because that’s where the growth is.

That’s not just Amazon, either. Target (NYSE:TGT

), Walmart (NYSE:WMT), Costco (NASDAQ:COST) and others have been plowing resources into their online operations. The following chart highlights why:

Click to Enlarge

As you can see, the e-commerce trend has been in play for quite some times. In the case of Wayfair, the catalysts go even further. With resilient housing sales in the U.S., consumers aren’t letting fear of a lasting recession stop them from moving forward.

This is unlike what we saw during the last recession about a decade ago, where the housing market was decimated. Although a big part of that problem was the real estate market itself, which played into the issues of the Great Recession.

We’re not facing the same risks here — a recession triggered by a global pandemic, not a real estate bubble — and it shows in housing sales. That should continue to benefit Wayfair, which sells all types of furniture.

It Has Growth

The boom in sales isn’t just theoretical, it’s tangible. Analysts expect sales growth of 36.5% this year. Even though analysts’ estimates call for a loss of $3.92 per share in fiscal 2020, that’s up big from prior estimates. Just 90 days ago, analysts were forecasting for a loss of $9.02 per share.

In 2021, consensus expectations call for growth to cool down, but still be positive. Specifically, analysts are looking for revenue and earnings growth of 16% and 23%, respectively.

At a time where many companies are struggling to generate positive sales and earnings growth, Wayfair is doing both.

The Risks

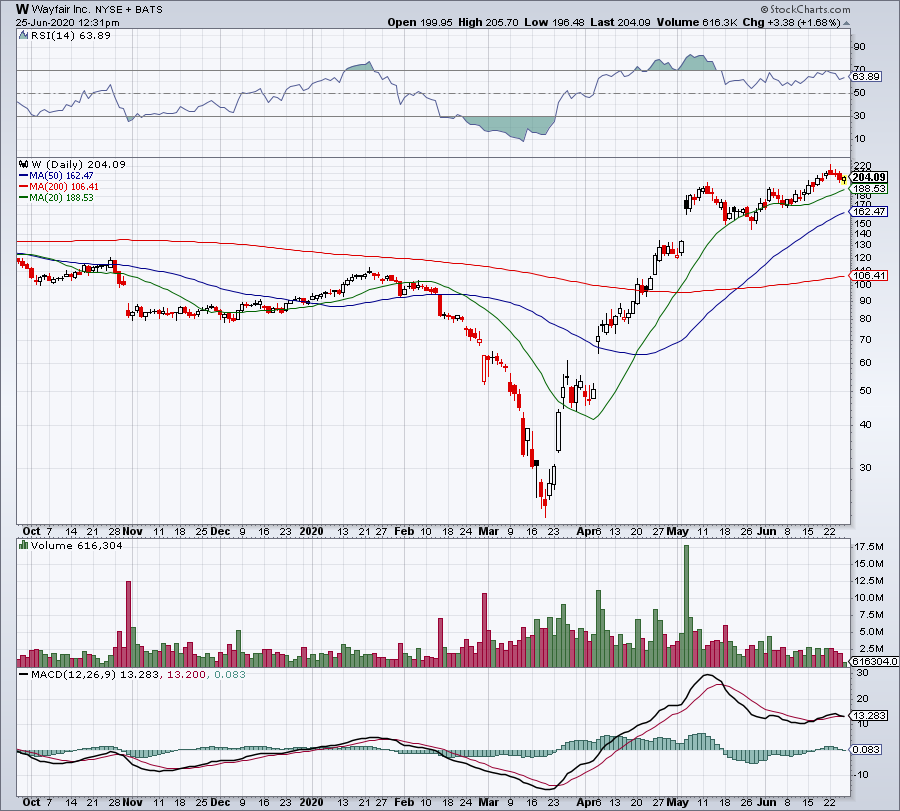

Click to Enlarge

That said, this stock doesn’t come without risks. This isn’t Amazon — which has a booming e-commerce arm, an advertising unit, and a cloud computing business.

We’ve underscored Wayfair’s negative net income, but realize there are other concerns, too. Free cash flow is negative and continues to worsen on an annual basis. Current liabilities also top current assets — $1.49 billion vs. $1.27 billion — creating concern about short-term liquidity.

Finally, the stock is up more than 700% from the lows. While that’s a great run for the bulls and shows that longs are in firm control of the stock, it does create concern about a substantial pullback. That’s even with coronavirus remaining front and center and even as growth prospects remain strong.

At the end of the day though, the trend is our friend. That goes for both the top and bottom line, as well as the stock price. Stick with the trend until it bends.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.